PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073514

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073514

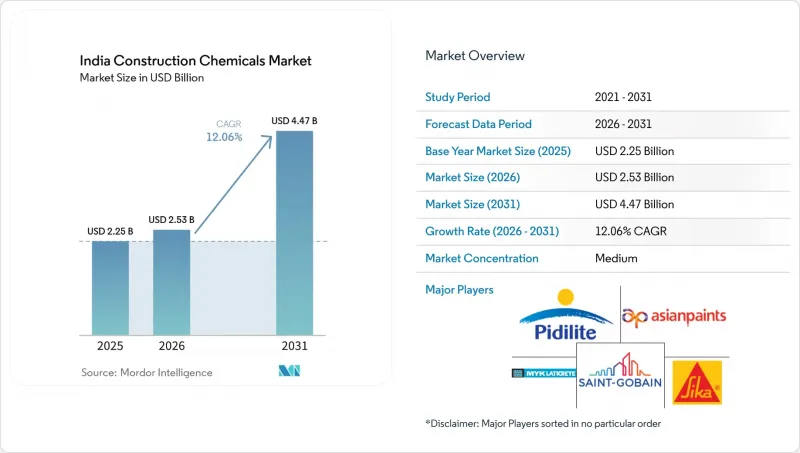

India Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india construction chemicals market size is expected to grow from USD 2.25 billion in 2025 to USD 2.53 billion in 2026 and is forecast to reach USD 4.47 billion by 2031 at 12.06% CAGR over 2026-2031.

This report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, and Waterproofing Solutions), and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

India Construction Chemicals Market Trends and Insights

Mega-infrastructure pipeline boosts specialty admixture demand

National Infrastructure Pipeline allocations channel steady large-volume orders toward high-range water reducers, corrosion inhibitors, and shrinkage-reducing admixtures needed for metro tunneling, coastal bridges, and seismic-zone viaducts. High-specification concrete for the Mumbai Metro Line 3 and Delhi-Meerut RRTS requires elevated early strength and low permeability, thereby heightening demand for premium polycarboxylate-ether chemistries. Highway packages under the Bharatmala Pariyojana are increasingly mandating performance-based mixes, which embed superplasticizer and air-entrainment dosages in tender documents. Suppliers therefore align research and development pipelines to resilient-infrastructure guidelines, releasing fiber-reinforced polymer systems and crystalline waterproofing lines for cut-and-cover segments exposed to groundwater ingress. These dynamics keep the India construction chemicals market closely tethered to public-sector rollout timetables, with regional stocking hubs springing up near project clusters to minimize lead times. Consequently, integrated producers with backward linkages to key monomers secure a competitive cost advantage as specialty-grade resin inputs become increasingly scarce globally.

Transition from on-site mixed concrete to ready-mixed concrete

RMC penetration is increasing, reshaping reagent ordering cycles toward bulk-supply contracts with batching plant operators. Consistent slump retention across long haul times pushes demand for retarding admixtures, viscosity-modifying agents, and pumping aids that small on-site mixers seldom use. Automated dosing systems now integrate directly with ERP platforms, enabling suppliers to monitor real-time consumption and remotely optimize formulation tweaks. Metro contractors in land-scarce downtown cores favor RMC to curtail traffic disruptions, strengthening the captive pull for additive packages bundled under multi-year framework agreements. As regional players invest in inline moisture sensors and rheology controllers, the India construction chemicals market deepens its shift from commodity bulk powders toward service-wrapped chemistry solutions that embed technical advisory fees within product invoices. This transformation raises entry barriers for unorganized formulators lacking application engineering bandwidth.

Volatility in petro-chemical-based resin prices

Price swings in epoxy and polyurethane resins during 2024 hindered project budgeting and eroded the working capital buffers of small manufacturers. Currency fluctuation layered extra cost-pass-through risk onto imports of MDI and TDI, while Red Sea freight disruptions extended lead times by a month. Larger players absorbed shocks by tapping term crude contracts and using hedging instruments, but regional blenders struggled to synchronize selling prices with volatile input costs, resulting in delivery delays. Contractors, wary of mid-project price resets, sometimes reverted to basic cement-sand blends, which dampened the uptake of premium-grade materials. Government Production-Linked Incentive (PLI) frameworks for specialty chemicals may alleviate exposure over the medium term; however, in the interim, margin compression weighs on new capacity decisions, tempering the otherwise upbeat trajectory of the India construction chemicals market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid penetration of green-label certified products

- Growth of renovation and reconstruction projects

- Fragmented applicator ecosystem limits specification compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions captured 35.15% of India's construction chemicals market share in 2025 as monsoon-exposed cities and rising basement construction heightened the need for robust hydrostatic protection. The segment benefits from mandated roof-treatment warranties in Mumbai, Chennai, and Kochi, where saline spray accelerates corrosion. Bitumen-based sheets are gradually being replaced by crystalline admixtures and modified polyurethane membranes, which offer longer life-cycle value with thinner profiles. Suppliers bundle site diagnostics and IR-thermography services into product packages, leveraging value engineering to upsell solvent-free primers and moisture-curing topcoats. Across Western India, tunnel waterproofing for metro extensions sustains a steady volume of PVC membrane sales, injecting scale efficiencies into domestic extrusion lines. Complementary growth arises from balcony, podium, and water tank applications within the mid-income housing boom, broadening SKU rotation beyond big-ticket infrastructure projects.

Concrete admixtures are driven by the uptake of RMC plants and performance-based tender norms. Early-strength superplasticizers secure night concreting windows for metro contractors, while slump-retention retarding blends support 60-minute haul distances in congested metros. As value-added grades grow, the India construction chemicals market size for admixtures is projected to outpace that of commodity grey powders. Adhesives, anchors, and grouts gain traction from precast modules and facade panels, with rapid-curing polyester resins supporting vertical construction speed targets. Protective coatings line sewage lift stations, desalination plants, and chemical storage yards where high acid resistance is critical. Flooring resins, led by epoxy terrazzo and polyurethane cement, are gaining traction in pharmaceutical and food and beverage plants to meet HACCP and cleanroom standards. Repair chemicals unlock premium price points through specialty carbon-fiber wraps for bridge girders and chimney stack rehabilitation, adding resilience to revenue mixes during new-build pauses.

Complete Report Scope:

- By Product

- Adhesives

- Hot-Melt

- Reactive

- Solvent-borne

- Water-borne

- Anchors and Grouts

- Cementitious Fixing

- Resin Fixing

- Concrete Admixtures

- Accelerator

- Air-Entraining

- Super-plasticizer

- Retarder

- Shrinkage-Reducer

- Viscosity-Modifier

- Plasticizer

- Other Types

- Concrete Protective Coatings

- Acrylic

- Alkyd

- Epoxy

- Polyurethane

- Other Resins

- Flooring Resins

- Acrylic

- Epoxy

- Polyaspartic

- Polyurethane

- Other Resins

- Repair and Rehabilitation Chemicals

- Fiber-Wrapping Systems

- Injection Grouting

- Micro-concrete Mortars

- Modified Mortars

- Rebar Protectors

- Sealants

- Acrylic

- Epoxy

- Polyurethane

- Silicone

- Other Resins

- Surface-Treatment Chemicals

- Curing Compounds

- Mold-Release Agents

- Other Types

- Waterproofing Solutions

- Chemicals

- Membranes

- Adhesives

- By End-Use Sector

- Commercial

- Industrial and Institutional

- Infrastructure

- Residential

List of Companies Covered in this Report:

- 3M

- ADT Industries Private Limited

- Ardex Endura (India) Pvt Ltd

- Arkema (Bostik)

- Asian Paints

- Berger Paints India Ltd.

- Chembond Chemicals Limited

- CICO Group

- ECMAS Group

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jotun

- Kansai Nerolac Paints Ltd.

- MAPEI S.p.A.

- MC-Bauchemie

- MYK LATICRETE India, Inc.

- PENETRON

- Pidilite Industries Ltd.

- RPM International

- Saint-Gobain

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mega-infrastructure pipeline boosts specialty admixture demand

- 4.2.2 Transition from on-site mixed concrete to ready-mixed concrete

- 4.2.3 Rapid penetration of green-label certified products

- 4.2.4 Growth of renovation and reconstruction projects

- 4.2.5 Rising need for affordable housing projects

- 4.3 Market Restraints

- 4.3.1 Volatility in petro-chemical-based resin prices

- 4.3.2 Fragmented applicator ecosystem limits specification compliance

- 4.3.3 Import dependency on specialty raw materials amid geopolitical risks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ADT Industries Private Limited

- 6.4.3 Ardex Endura (India) Pvt Ltd

- 6.4.4 Arkema (Bostik)

- 6.4.5 Asian Paints

- 6.4.6 Berger Paints India Ltd.

- 6.4.7 Chembond Chemicals Limited

- 6.4.8 CICO Group

- 6.4.9 ECMAS Group

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Jotun

- 6.4.13 Kansai Nerolac Paints Ltd.

- 6.4.14 MAPEI S.p.A.

- 6.4.15 MC-Bauchemie

- 6.4.16 MYK LATICRETE India, Inc.

- 6.4.17 PENETRON

- 6.4.18 Pidilite Industries Ltd.

- 6.4.19 RPM International

- 6.4.20 Saint-Gobain

- 6.4.21 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment