PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066716

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066716

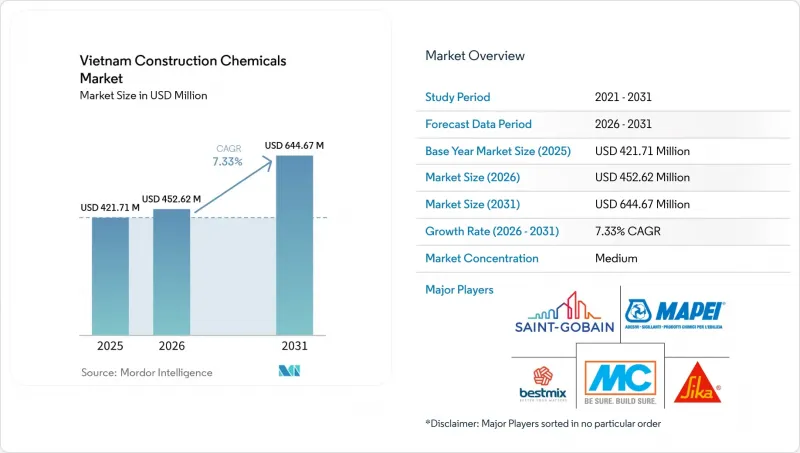

Vietnam Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vietnam construction chemicals market size is expected to increase from USD 421.71 million in 2025 to USD 452.62 million in 2026 and reach USD 644.67 million by 2031, growing at a CAGR of 7.33% over 2026-2031.

This report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, and Waterproofing Solutions) and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Construction Chemicals Market Trends and Insights

Mega-Infrastructure Pipeline Boosts Specialty-Admixture Demand

Expressways, bridges, and airport projects such as CT.33, Dai Ngai Bridge, and Long Thanh International Airport require chloride-resistant mortars and third-generation polycarboxylate ether superplasticizers that maintain workability at ambient temperatures above 35 °C. The Eastern North-South Expressway Phase 2 alone is estimated to require 200,000 tonnes of admixtures, repair mortars, and surface treatments over five construction seasons Contractors pre-qualify branded systems such as SikaPlast-396 VN and BestFlow A325 to achieve water-cement ratios below 0.35 and 28-day compressive strengths exceeding 60 MPa. Suppliers embedding technical service teams in site laboratories secure recurring volume orders across multiyear project phases, ensuring specification compliance throughout the design-build-operate cycle.

Transition from On-Site Mixed to Ready-Mixed Concrete

Urban ordinances restricting on-site batching to reduce dust and traffic congestion are accelerating the shift toward ISO 9001-certified ready-mixed concrete (RMC) plants. RMC logistics drive demand for retarders and viscosity modifiers that extend slump life over delivery distances of up to 30 km in peri-urban areas such as Binh Duong. Digital dosing platforms, which measure admixtures with +-0.1% precision, have reduced material waste by 20% and compressive-strength variability by up to 25%, reinforcing the preference for premium admixtures with precise formulation tolerances.

Volatility in Petrochemical-Based Resin Prices

In 2024, prices for PVC, epoxy, and polyurethane feedstocks surged by 15-20% within three months, impacting manufacturers reliant on imported resins and unable to hedge long-term contracts. Smaller producers with annual outputs below 5,000 tonnes faced challenges, including price increases and delayed product launches. In contrast, larger companies diversified into bio-based inputs and recycled polyols to reduce dependency on crude oil prices. For example, Saint-Gobain's biomass-powered DURAflex line reduces Scope 1 CO2 emissions by 2,000 tonnes annually, demonstrating how localized feedstocks can mitigate price volatility.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Penetration of Green-Label Certified Products

- Growth of Renovation and Reconstruction Projects

- Fragmented Applicator Ecosystem Limits Spec-Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions accounted for 45.66% of the Vietnam construction chemicals market share in 2025, driven by Ho Chi Minh City regulations requiring high-elasticity membranes for basements situated below 3 meters sea level. This category includes crystalline admixtures, penetrating sealers, and membrane rolls, with membranes holding higher value due to their use in metro tunnels, wastewater plants, and deep-podium car parks that need multi-layer, crack-bridging systems. Bestmix delivered 100,000 tonnes of BestSeal membranes to 75 mega factories in 2024, reflecting the high-volume demand in the Vietnam construction chemicals market.

Concrete admixtures is the fastest-growing segment, with an 8.19% CAGR projected through 2031, steadily increasing its share in the Vietnam construction chemicals market. Ready-mixed concrete plants pre-dose polycarboxylate ether superplasticizers like SikaPlast-396 VN and MC-PowerFlow 2116 to achieve 28-day strengths exceeding 60 MPa, even under 35 °C coastal humidity. The demand for admixtures is also rising due to high-speed railway viaducts and 40-story composite towers that require slump-retaining retarders and rheology-modifying agents to pump concrete above 200 meters.

Adhesives, anchors and grouts, sealants, protective coatings, flooring resins, and repair chemicals cater to high-value niches such as seismic anchorage and (Good Manufacturing Practice)-compliant flooring. Epoxy anchors certified to TCVN 10304:2025 are used for wind-turbine foundations and port crane rails, while electrostatic-discharge-safe floor toppings dominate electronics clean rooms in Bac Ninh. Carbon-fiber laminates and injection epoxies are now standard for bridge rehabilitation projects.

List of Companies Covered in this Report:

- Adchem Construction Chemical (Amcor)

- BESTMIX CORPORATION

- GPS Vietnam

- MAPEI S.p.A.

- MC-Bauchemie

- Saint-Gobain

- Schomburg

- Sika AG

- Thermax Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mega-infrastructure pipeline boosts specialty-admixture demand

- 4.2.2 Transition from on-site mixed to ready-mixed concrete

- 4.2.3 Rapid penetration of green-label certified products

- 4.2.4 Growth of renovation and reconstruction projects

- 4.2.5 Digitalised job-site dosing and QA systems lift premium uptake

- 4.3 Market Restraints

- 4.3.1 Volatility in petro-chemical-based resin prices

- 4.3.2 Fragmented applicator ecosystem limits spec-compliance

- 4.3.3 Counterfeit waterproofing products erode brand trust

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticiser

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Concrete Admixtures

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Concrete Protective Coatings

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Flooring Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Sealants

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Surface-Treatment Chemicals

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Adchem Construction Chemical (Amcor)

- 6.4.2 BESTMIX CORPORATION

- 6.4.3 GPS Vietnam

- 6.4.4 MAPEI S.p.A.

- 6.4.5 MC-Bauchemie

- 6.4.6 Saint-Gobain

- 6.4.7 Schomburg

- 6.4.8 Sika AG

- 6.4.9 Thermax Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment