PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073519

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073519

Smartphones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

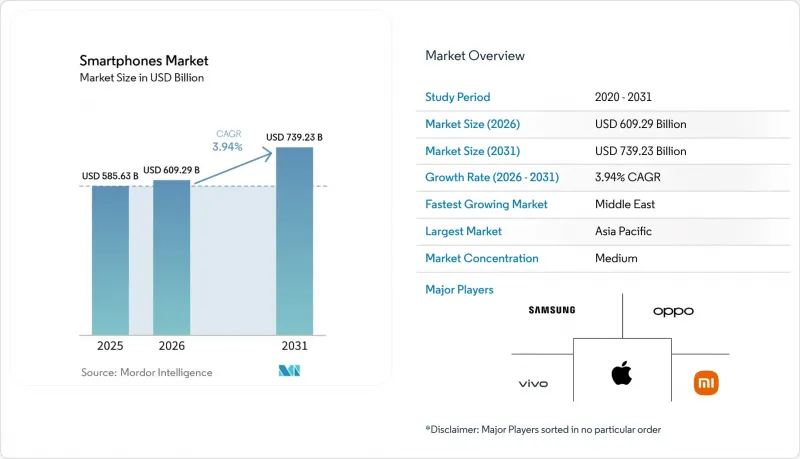

According to Mordor Intelligence, the smartphones market size is expected to grow from USD 585.63 billion in 2025 to USD 609.29 billion in 2026 and is forecast to reach USD 739.23 billion by 2031 at 3.94% CAGR over 2026-2031.

This report is Segmented by Operating System (Android, IOS, and More), Price Band (Entry-Level, Mid-Range and More), Technology (5G, 4G/LTE, and More), Form Factor (Bar, Foldable/Flip, and More), Distribution Channel (Operator/Carrier Stores, Brand-Owned Retail, and More), End-User (Consumer/Individual and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Smartphones Market Trends and Insights

AI-Enabled Upgrade Cycle Accelerates Replacements

On-device generative AI, now capable of more than 40 trillion operations per second, has become a headline feature in flagship launches. Apple's A18 Pro and Qualcomm's Snapdragon 8 Elite showcase neural engines that deliver real-time translation, image synthesis, and personal-assistant tasks without cloud latency. In North America and Europe, this capability shortened replacement cycles in the smartphones market, as 38% of surveyed users in 2025 cited AI as their primary upgrade trigger. Premium buyers perceive tangible day-to-day benefits, such as instant meeting summaries and on-device photo editing, which reinforce a willingness to pay flagship pricing. Chinese vendors are responding quickly: MediaTek's Dimensity 9400 delivers a 30% power-efficiency gain for multimodal assistants, making AI a cross-platform baseline. The arms race is likely to persist through 2029 as chipmakers chase ever-larger parameter models optimized for handset thermals.

Premiumization Sustained by Financing, Trade-Ins, and Extended Software Support

Zero-interest installment plans and aggressive trade-in credits are shifting consumer focus from upfront cost to monthly affordability. U.S. carriers now stretch payments over 36 months, effectively turning a USD 1,200 flagship into a USD 33 obligation, while Apple processed more than 12 million trade-ins in 2024 that shaved up to USD 500 off the sticker price. Seven-year update pledges from Samsung and Google further lower total cost of ownership, reassuring buyers that premium models will stay secure and current well past typical refresh cycles. Together, these mechanisms keep premium demand in the smartphones market resilient even during macro softness and funnel more revenue into higher ASP tiers. Emerging markets are beginning to mirror this behavior as local banks and fintechs roll out installment-based handset loans.

Memory Supply Tightness Lifts BoM Costs

DRAM spot prices climbed roughly 20% in late 2024 as wafer capacity was diverted to high-bandwidth server modules. Samsung and SK Hynix prioritized automotive and data-center customers, leaving mobile LPDDR shortfalls that forced entry-level Android vendors to dial back memory configurations. In price-sensitive markets, a USD 10 increase pushes buyers toward 4 GB variants or even feature phones, eroding volume forecasts. Component inflation also squeezes razor-thin gross margins, prompting some tier-two brands to postpone launches or bundle fewer accessories. Relief is unlikely before mid-2026 when new fabs ramp, keeping pressure on low-end ASPs across the smartphones market and potentially widening the digital divide.

Other drivers and restraints analyzed in the detailed report include:

- Entry-Level 5G Proliferation in Emerging Markets

- Foldable Maturation Expands High-Value Niches

- Used or Refurbished Smartphone Growth Cannibalizes New Device Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Android retained 69.21% smartphones market share in 2025, yet HarmonyOS and KaiOS are growing at 5.29% annually, signaling gradual fragmentation. Huawei shipped more than 70 million HarmonyOS phones in 2024, fortifying a China-centric ecosystem that operates without Google services. KaiOS, powering ultra-low-cost devices, surpassed 150 million cumulative activations, introducing first-time internet users to app-based experiences. The smartphones market size for alternative platforms remains small today, but their trajectory challenges Android's ubiquity in specific niches. Regulatory shifts, including the EU Digital Markets Act and India's interoperability proposals, level the playing field by mandating third-party app stores and cross-platform messaging. As compliance costs rise, both iOS and Android may concede incremental share to regional or purpose-built platforms that promise data sovereignty or superior low-end performance.

Apple's iOS meanwhile consolidates pricing power: fiscal 2024 iPhone revenue hit USD 200 billion, driven by Pro variants that anchor the ultra-premium tranche. Apple's vertical integration of silicon, operating system, and services delivers a cohesive experience that justifies a USD 1,100 ASP, insulating iOS from price-based competition. For Android vendors, strategic responses include faster update pledges and tighter Google security certifications. Over the forecast, platform diversification in the smartphones market will hinge on localized regulation, app-store economics, and developer incentives rather than pure technological capability.

Ultra-premium smartphones above USD 800 are projected to grow at 6.42% through 2031, outpacing every other tier. Flagships such as iPhone 16 Pro Max and Galaxy S25 Ultra integrate titanium frames, periscope lenses, and on-device AI that elevate perceived value. Trade-in credits and carrier financing reduce the effective purchase hurdle, drawing aspirational buyers into the segment. At the other extreme, entry-level models below USD 200 face BoM inflation and heightened competition from refurbished units, which narrows already thin margins.

Mid-range devices, priced USD 200-499, captured the bulk of 2025 revenue by offering 5G connectivity, multi-sensor cameras, and fast charging at palatable prices. Vendors use this band as a stepping stone, upselling via limited-time promotions or bundling accessories. Premium (USD 500-799) occupies a shrinking middle ground as consumers polarize toward either value or flagship experiences. The smartphones market size for mid-range will still expand, but the revenue mix will tilt toward ultra-premium where incremental hardware upgrades command outsized margins.

Complete Report Scope:

- Overall Market Estimates

- Total Market Value (USD)

- Total Market Volume (Units)

- By Operating System (Value, and Volume)

- Android

- iOS

- Others (HarmonyOS, KaiOS)

- By Price Band (Value, and Volume)

- Entry-Level (Less Than USD 200)

- Mid-Range (USD 200-499)

- Premium (USD 500-799)

- Ultra-Premium (More Than USD 800)

- By Technology (Network Generation) (Value)

- 5G

- 4G or LTE

- 3G and Below

- By Form Factor (Value)

- Bar

- Foldable or Flip

- Rugged or Industrial

- By Distribution Channel (Value)

- Operator or Carrier Stores

- Brand-Owned Retail

- Multi-Brand Physical Retail

- Online Direct-to-Consumer

- By End User (Value)

- Consumer or Individual

- Enterprise or SME

- Public Sector or Government

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Southeast Asia (Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia)

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of the Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia Pacific retained leadership with 42.81% of 2025 revenue, driven by China's vast installed base and India's manufacturing momentum. China's shift to domestically designed silicon, exemplified by Huawei's Mate 60 Pro, is steering premium buyers toward local brands, while India's Production-Linked Incentive scheme attracted USD 15 billion in cumulative handset investment, scaling export capacity and lowering global ASPs.

North America's upgrade cadence relies on carrier financing that conceals flagship prices. Apple captured over half of the U.S. premium segment in 2025, aided by trade-in credits, while Samsung boosted pre-orders 15% year-over-year with Galaxy S25 incentives. Canada and Mexico echo similar dynamics, balancing premium demand in metro areas with mid-range uptake in less affluent regions.

Europe's market remains fragmented: Germany and France highlight data-privacy features, whereas the United Kingdom leans on carrier deals that bundle unlimited data. The Digital Markets Act may reshape app-store economics, creating openings for regional players and alternative payment systems.

South America's growth hinges on Brazil's localized production, where Lenovo-owned Motorola commands share through mid-range devices adapted to local spending power. Currency volatility complicates pricing, yet 5G deployments in major cities stimulate replacement demand.

The Middle East leads forecast growth at a 10.83% CAGR. High disposable incomes in Saudi Arabia and the United Arab Emirates, coupled with government digitalization agendas, lift premium device sales. Operators accelerate mmWave rollouts, supporting AR tourism guides and enterprise IoT pilots that require flagship-grade smartphones.

Africa's market remains fiercely price sensitive, dominated by Transsion brands optimized for dual-SIM use and long battery life. 5G spectrum auctions in Nigeria and Kenya will spur gradual upgrades, but affordability constraints keep entry-level and refurbished devices prominent in the near term.

- Apple Inc.

- Samsung Electronics Co. Ltd

- Xiaomi Corporation

- OPPO (incl. OnePlus)

- Vivo Communication Technology Co., Ltd.

- Transsion Holdings Co., Ltd. (TECNO, Infinix, itel)

- Huawei Technologies Co., Ltd

- Honor Device Co., Ltd.

- Google LLC

- Motorola Mobility LLC (Lenovo Group Ltd)

- Realme Chongqing Mobile Telecommunications Corp., Ltd.

- HMD Global Oy (Nokia)

- Sony Corp.

- ASUSTeK Computer Inc.

- ZTE Corp.

- TCL Technology (Group) Co. Ltd (Alcatel)

- Nothing Technology Ltd

- Kyocera Corporation

- Sharp Corporation

- Fairphone B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Enabled Upgrade Cycle Accelerates Replacements (On-Device GenAI, Multimodal Assistants)

- 4.2.2 Premiumization Sustained by Financing, Trade-Ins, and Extended Software Support

- 4.2.3 Entry-Level 5G Proliferation in Emerging Markets

- 4.2.4 Foldable Maturation Expands High-Value Niches

- 4.2.5 Carrier-Led Promotions and Device Financing in Mature Markets

- 4.2.6 Regional Manufacturing Localization Incentives (India, Vietnam, Middle East, and Africa) Reduce Costs and Lead Times

- 4.3 Market Restraints

- 4.3.1 Memory Supply Tightness Lifts BoM Costs, Pressuring Low-End Android

- 4.3.2 Used or Refurbished Smartphone Growth Cannibalizes New Device Demand

- 4.3.3 Slower Refresh Cycles from Durability and Incremental Innovation

- 4.3.4 Geopolitics and Tariffs Shifting SKUs, Raising Logistics Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Macroeconomic Impact Analysis

- 4.6 Regulatory Landscape

- 4.6.1 Spectrum Allocation and Licensing (2G/3G/4G/5G)

- 4.6.2 eSIM Readiness and IoT Device Enablement

- 4.6.3 Device Import Policy and Local Manufacturing or Assembly Rules

- 4.7 Technological Outlook

- 4.7.1 SoC Roadmaps (NPU TOPS, RF Integration, Satellite NTN)

- 4.7.2 Display Stack (LTPO, Micro-Lens OLED, UDR Glass, Anti-Reflective Coatings)

- 4.7.3 Camera or Computational Photography (Periscope, Stacked Sensors, ISP or AI Fusion)

- 4.7.4 Battery or Charging (Silicon Anodes, GaN Fast Charge, BMS Safety)

- 4.7.5 Connectivity (Wi-Fi 7, Bluetooth LE Audio, UWB, 5G-Advanced)

- 4.8 Smartphone Device Lifecycle Analysis

- 4.8.1 Stakeholder Lifecycle Mapping

- 4.8.2 Key Pain-Point Analysis by Stakeholder

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Overall Market Estimates

- 5.1.1 Total Market Value (USD)

- 5.1.2 Total Market Volume (Units)

- 5.2 By Operating System (Value, and Volume)

- 5.2.1 Android

- 5.2.2 iOS

- 5.2.3 Others (HarmonyOS, KaiOS)

- 5.3 By Price Band (Value, and Volume)

- 5.3.1 Entry-Level (Less Than USD 200)

- 5.3.2 Mid-Range (USD 200-499)

- 5.3.3 Premium (USD 500-799)

- 5.3.4 Ultra-Premium (More Than USD 800)

- 5.4 By Technology (Network Generation) (Value)

- 5.4.1 5G

- 5.4.2 4G or LTE

- 5.4.3 3G and Below

- 5.5 By Form Factor (Value)

- 5.5.1 Bar

- 5.5.2 Foldable or Flip

- 5.5.3 Rugged or Industrial

- 5.6 By Distribution Channel (Value)

- 5.6.1 Operator or Carrier Stores

- 5.6.2 Brand-Owned Retail

- 5.6.3 Multi-Brand Physical Retail

- 5.6.4 Online Direct-to-Consumer

- 5.7 By End User (Value)

- 5.7.1 Consumer or Individual

- 5.7.2 Enterprise or SME

- 5.7.3 Public Sector or Government

- 5.8 By Geography (Value)

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Chile

- 5.8.2.4 Colombia

- 5.8.2.5 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 France

- 5.8.3.3 United Kingdom

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 India

- 5.8.4.3 Japan

- 5.8.4.4 South Korea

- 5.8.4.5 Southeast Asia (Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia)

- 5.8.4.6 Australia

- 5.8.4.7 Rest of Asia-Pacific

- 5.8.5 Middle East

- 5.8.5.1 Saudi Arabia

- 5.8.5.2 United Arab Emirates

- 5.8.5.3 Rest of the Middle East

- 5.8.6 Africa

- 5.8.6.1 South Africa

- 5.8.6.2 Nigeria

- 5.8.6.3 Rest of Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, Local Assembly MoUs)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd

- 6.4.3 Xiaomi Corporation

- 6.4.4 OPPO (incl. OnePlus)

- 6.4.5 Vivo Communication Technology Co., Ltd.

- 6.4.6 Transsion Holdings Co., Ltd. (TECNO, Infinix, itel)

- 6.4.7 Huawei Technologies Co., Ltd

- 6.4.8 Honor Device Co., Ltd.

- 6.4.9 Google LLC

- 6.4.10 Motorola Mobility LLC (Lenovo Group Ltd)

- 6.4.11 Realme Chongqing Mobile Telecommunications Corp., Ltd.

- 6.4.12 HMD Global Oy (Nokia)

- 6.4.13 Sony Corp.

- 6.4.14 ASUSTeK Computer Inc.

- 6.4.15 ZTE Corp.

- 6.4.16 TCL Technology (Group) Co. Ltd (Alcatel)

- 6.4.17 Nothing Technology Ltd

- 6.4.18 Kyocera Corporation

- 6.4.19 Sharp Corporation

- 6.4.20 Fairphone B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment