PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073543

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073543

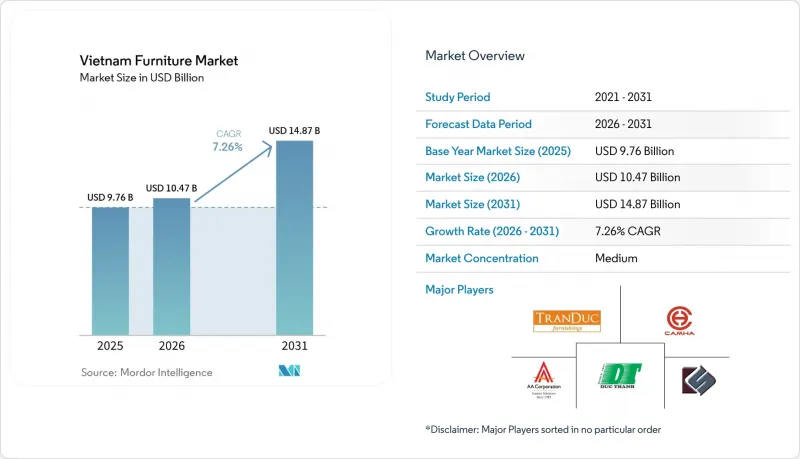

Vietnam Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vietnam furniture market size is expected to grow from USD 9.76 billion in 2025 to USD 10.47 billion in 2026 and is forecast to reach USD 14.87 billion by 2031 at a 7.26% CAGR over 2026-2031.

This report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and More), Material (Wood, Metal, Plastic & Polymer, and More), Price Range (Economy, Mid-Range, and Premium), Distribution Channel (B2C/Retail, and B2B /Project), and Geography (Northern Vietnam, Central Vietnam, and Southern Vietnam). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Furniture Market Trends and Insights

China+1 Strategy Driving Large-Scale Production Capacity Additions

Foreign direct investment is concentrating in processing and manufacturing, with new and additional registered capital of USD 7.97 billion during the first ten months of 2025, representing 56.7% of total FDI, which signals continued capacity additions in wood processing and downstream furniture lines. A large base of export-ready plants supports this shift, with approximately 1,500 factories exporting and foreign-invested enterprises contributing nearly 40% of export value in 2025, reinforcing the role of multinational capital in scaling productivity and compliance systems. The presence of global operators in Southern and Central Vietnam underscores sustained investment sentiment and links to North American and European retail programs that require stable suppliers and consistent quality standards. Production expansion plans announced in 2025 by leading exporters point to near-term job creation and throughput increases in key clusters such as Binh Duong and Quang Ngai, alongside investments in bonded warehousing and logistics solutions to streamline container flows. Collectively, these initiatives support the Vietnam furniture market by balancing export-led growth with rising domestic demand, while lowering switching risks for international buyers through broader geographic plant footprints and deeper supplier integration.

Growing Urban Consumer Base Driving Home Furnishing and Interior Upgrades

Vietnam's urbanization rate reached 40% by 2025 and continues to expand at 2.5% to 3% annually, which increases the pool of households purchasing living, dining, and bedroom goods across major cities and emerging urban nodes. The domestic market is benefiting from improved income profiles and a steady flow of new housing, reinforcing retail demand across mid-range and premium price tiers where differentiation is driven by design and materials. E-commerce and digital payments are improving access for consumers outside core urban districts, which helps brands test direct-to-consumer formats while maintaining targeted store footprints in high-traffic locations. The category mix shows stickiness in home furniture staples, while younger cohorts respond to ready-to-assemble options and modular configurations that align with compact urban living spaces and flexible usage requirements. Overall, the urban middle-class dynamic provides a stable backbone of repeat purchases and household upgrades that supports the Vietnam furniture market through cycles, including phases of export volatility.

Rising Raw Material and Logistics Expenses Squeezing Profitability

Vietnam relies on imported timber for higher-grade inputs, with total timber and forest product imports rising in 2024 and reaching USD 1.29 billion in the first half of 2024, which placed upward pressure on material costs for domestic processors. The composition of imports shows a high share of logs and sawn timber, and fluctuations in these categories can influence production schedules and pricing strategies for export contracts. Container shipping volatility compounds cost dynamics, affecting exporters concentrated near Southern ports where throughput is high, and scheduling flexibility is critical. To keep orders, enterprises have absorbed discounts in some export lanes, which narrows margins during tariff and freight spikes and challenges smaller operators with limited working capital buffers. These conditions pressure the Vietnam furniture market's cost structure, pushing companies to optimize material yields, expand plantation sourcing, and negotiate longer-term contracts with logistics partners to stabilize input and transport costs.

Other drivers and restraints analyzed in the detailed report include:

- Multilateral Trade Frameworks Unlocking Premium Market Entry Opportunities

- Digital Commerce Infrastructure Enabling Direct-to-Consumer Distribution Models

- Stricter US Customs Scrutiny and Anti-Circumvention Measures Elevating Export Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Home furniture accounts for the largest share at 57.84% in 2025, supported by expanding urban households that prioritize living, dining, and bedroom categories, and this share anchors demand stability while the Vietnam furniture market advances into 2026. Office furniture remains the second-largest application by value, with steady demand from corporate users and public sector facilities that favor established casegoods and seating specifications aligned with durability and ergonomic standards. Hospitality furniture is the fastest-growing application with an 8.76% CAGR during 2026 to 2031 as new hotel and resort projects progress across coastal and gateway markets, which increases demand for contract-grade outdoor, lobby, and guestroom furniture. Educational and healthcare furniture respond to public and private capital expenditure cycles, supplying desks, storage, beds, and seating variants for institutional settings where specifications and certification requirements are more stringent. The Vietnam furniture market also scales ready-to-assemble formats for younger urban consumers, which supports value-engineered designs in wood-based panels and mixed materials.

Export composition into the United States shows wood-framed chairs as a leading item by value in 2025, with living and dining room products, bedroom sets, and kitchen furniture also contributing to growing order books, reflecting recovery from the 2023 trough and diversified category momentum in 2024 and 2025. The office category is strengthening after a period of decline earlier in the decade, supported by post-pandemic refurbishment programs and a focus on task seating and modular systems that satisfy hybrid work patterns. Home category upgrades are influenced by urban apartment layouts and storage needs, favoring compact dining, sofa beds, and configurable storage that optimize small spaces without sacrificing aesthetics, which differentiates products in the Vietnam furniture market through practical design. Hospitality's growth path spans indoor and outdoor applications, with emphasis on resistant finishes, moisture tolerance, and ease of maintenance as tourism continues to normalize across key destinations. Over the forecast period, suppliers that blend compliance, design versatility, and competitive lead times remain well-positioned to capture incremental value in each major application.

Wood remains the dominant material with a 68.49% share in 2025, supplied by plantation species such as acacia and rubberwood as well as imported logs and sawn timber, which collectively underpin the Vietnam furniture market's scale in mass and premium segments. Production data indicate strong activity in early 2025, with industrial forestry indicators rising year-on-year, which supports input availability for manufacturers focusing on export-grade finishing and assembly. Plastic and polymer furniture is the fastest-growing material category at a 9.48% CAGR from 2026 to 2031, reflecting gains in outdoor, hospitality, and value-focused consumer segments where weight, durability, and weather resistance are decisive. Metal-based furniture remains important for commercial and outdoor applications, although price dynamics for steel and aluminum inputs can influence product mix in project channels. Across materials, suppliers are upgrading environmental management and chain-of-custody systems to align with customer and regulatory expectations in export markets, which supports the Vietnam furniture market's diversification into higher-value products.

Import composition for timber rose during 2024, with logs and sawn timber handling a large share of value, and those shifts required factories to recalibrate unit economics while maintaining on-time deliveries during freight volatility. Companies are investing in environmental certifications, solar power, and biomass consumption to support cleaner operations and cost stability, which strengthens positioning with European and North American buyers that require verified environmental practices. Plastic and polymer advances are supported by new compounds with UV resistance and recyclability features, which broaden outdoor and family-use categories that demand easy cleaning and durability. Material diversification helps the Vietnam furniture market reduce exposure to timber price swings while allowing brands to maintain a price ladder across economy, mid-range, and premium tiers. From 2026 to 2031, suppliers that optimize material sourcing and sustainability credentials are positioned to capture category growth led by wood and accelerated by polymers in targeted segments.

Complete Report Scope:

- By Application

- Home Furniture

- Chairs

- Tables (side tables, coffee tables, dressing tables, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables/Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- Office Furniture

- Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas and Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (public places, retail malls, government offices, etc.)

- Home Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B /Project

- B2C/Retail

- By Geography

- Southern Vietnam

- Northern Vietnam

- Central Vietnam

List of Companies Covered in this Report:

- Duc Thanh Wood Processing JSC

- AA Corporation

- Kaiser 1 Furniture Industry (Vietnam) Co., Ltd

- Tran Duc Furnishings

- Cam Ha Furniture JSC

- Hoang Moc Furniture

- An Viet Furniture

- MoHo Furniture

- The One Furniture (Hoa Phat Interiors)

- BAYA (AKA Furniture Group)

- Truong Thanh Wood Industries (TTF)

- Phu Tai JSC (PTB)

- Vinafor

- Scaviwood

- Xuan Hoa Furniture

- Foster Vietnam

- Glory Oceanic

- IKEA

- JYSK

- BoConcept

- Nitori Co. Ltd

- Wanek Furniture Co. Ltd

- Cassina S.p.A

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 China+1 Strategy Driving Large-Scale Production Capacity Additions

- 4.2.2 Growing Urban Consumer Base Driving Home Furnishing and Interior Upgrades

- 4.2.3 Multilateral Trade Frameworks Unlocking Premium Market Entry Opportunities

- 4.2.4 Digital Commerce Infrastructure Enabling Direct-to-Consumer Distribution Models

- 4.2.5 Commercial Real Estate Pipeline Creating Sustained Institutional Buyer Demand

- 4.2.6 Industry 4.0 Adoption and Automation Driving Production Efficiency and Quality Upgrades

- 4.3 Market Restraints

- 4.3.1 Rising Raw Material and Logistics Expenses Squeezing Profitability

- 4.3.2 Stricter US Customs Scrutiny and Anti-Circumvention Measures Elevating Export Costs

- 4.3.3 Elevated Real Estate Costs and Disjointed Distribution Networks Limiting Retail Expansion

- 4.3.4 Evolving Environmental Standards and Trade Regulations Creating Certification Barriers

- 4.4 Industry Value Chain Analysis

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Home Furniture

- 5.1.1.1 Chairs

- 5.1.1.2 Tables (side tables, coffee tables, dressing tables, etc.)

- 5.1.1.3 Beds

- 5.1.1.4 Wardrobes

- 5.1.1.5 Sofas

- 5.1.1.6 Dining Tables/Dining Sets

- 5.1.1.7 Kitchen Cabinets

- 5.1.1.8 Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- 5.1.2 Office Furniture

- 5.1.2.1 Chairs

- 5.1.2.2 Tables

- 5.1.2.3 Storage Cabinets

- 5.1.2.4 Desks

- 5.1.2.5 Sofas and Other Soft Seating

- 5.1.2.6 Other Office Furniture

- 5.1.3 Hospitality Furniture

- 5.1.4 Educational Furniture

- 5.1.5 Healthcare Furniture

- 5.1.6 Other Applications (public places, retail malls, government offices, etc.)

- 5.1.1 Home Furniture

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic & Polymer

- 5.2.4 Other Materials

- 5.3 By Price Range

- 5.3.1 Economy

- 5.3.2 Mid-Range

- 5.3.3 Premium

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail

- 5.4.1.1 Home Centers

- 5.4.1.2 Specialty Furniture Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B /Project

- 5.4.1 B2C/Retail

- 5.5 By Geography

- 5.5.1 Southern Vietnam

- 5.5.2 Northern Vietnam

- 5.5.3 Central Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Duc Thanh Wood Processing JSC

- 6.4.2 AA Corporation

- 6.4.3 Kaiser 1 Furniture Industry (Vietnam) Co., Ltd

- 6.4.4 Tran Duc Furnishings

- 6.4.5 Cam Ha Furniture JSC

- 6.4.6 Hoang Moc Furniture

- 6.4.7 An Viet Furniture

- 6.4.8 MoHo Furniture

- 6.4.9 The One Furniture (Hoa Phat Interiors)

- 6.4.10 BAYA (AKA Furniture Group)

- 6.4.11 Truong Thanh Wood Industries (TTF)

- 6.4.12 Phu Tai JSC (PTB)

- 6.4.13 Vinafor

- 6.4.14 Scaviwood

- 6.4.15 Xuan Hoa Furniture

- 6.4.16 Foster Vietnam

- 6.4.17 Glory Oceanic

- 6.4.18 IKEA

- 6.4.19 JYSK

- 6.4.20 BoConcept

- 6.4.21 Nitori Co. Ltd

- 6.4.22 Wanek Furniture Co. Ltd

- 6.4.23 Cassina S.p.A

7 Market Opportunities & Future Outlook

- 7.1 Market Diversification to Emerging High-Growth Markets (China, India, Middle East)

- 7.2 Sustainable and Certified Product Development with Carbon Credit Revenue Potential