PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061670

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061670

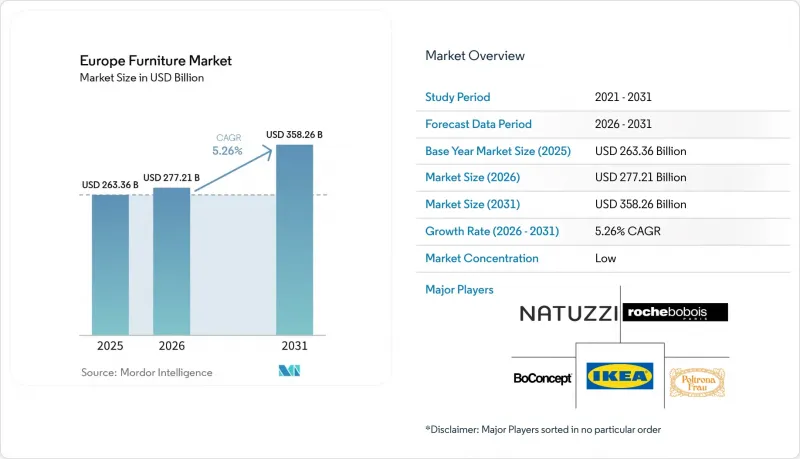

Europe Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, europe furniture market size was valued at USD 263.36 billion in 2025 and is estimated to grow from USD 277.21 billion in 2026 to reach USD 358.26 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031).

This report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and More), Material (Wood Furniture, Metal Furniture, and More), Price Range (Economy, Mid-Range, and Premium), Distribution Channel (B2C/Retail, and B2B /Project), and Geography (United Kingdom, Germany, France, Italy and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Furniture Market Trends and Insights

EU Renovation Grants and Energy Retrofits Driving Large-Scale Furniture Replacement

EU renovation policy aims to double renovation rates by 2030 and retrofit 35 million buildings, which increases replacement cycles for kitchens, living spaces, and work areas aligned to modern performance and safety standards. National programs and local funding channels complement EU-level goals and contribute to retrofits getting pulled forward as property owners address insulation, ventilation, and layout improvements. Renovated homes often require integrated storage, modular seating, and cabinetry that can accommodate efficient appliances and better air quality standards. The share of residents in dwellings with efficiency improvements rose in recent years, which supports steady furniture refresh activity as owners complete multi-year projects. These policy actions intersect with tightening chemical emissions rules for components and coatings, prompting shifts to lower emissions in materials and finishes across the supply base. Manufacturers operating in Northern Europe reported facility and process adjustments, including wider use of water-based coatings and steps to trim VOC emissions, that align with emerging compliance thresholds.

Hybrid Work Normalization Sustaining Demand for Home Office and Modular Workspace Furniture

Hybrid work settled into long-run usage levels, which keep home office equipment and compact workstations relevant for both B2C and project channels. France-based surveys show sustained interest in remote work options and continued fit-out and reconfiguration projects as employers reshape space for collaboration and shared desks. Occupiers reduced enclosed offices and expanded collaborative areas, prompting purchases of ergonomic chairs, height-adjustable desks, and acoustic solutions that raise per-employee specification levels even as total desk counts per head decline. This creates a shift in purchasing from traditional distribution to project-based procurement for shop and contract use, which partially offsets softer order books in classic office lines. The expansion of second-hand and refurbished office furniture gained momentum as sellers highlight lower cost and verified carbon reductions compared with new products. Retailers and refurbishers emphasize omnichannel merchandising, in-store configuration tools, and after-sales services to capture hybrid-driven demand that moves between home and workplace settings.

Other drivers and restraints analyzed in the detailed report include:

- Cross-Border E-Commerce, BNPL, and OSS VAT Regime Broadening Access

- Aging Demographics Increasing Spend on Ergonomic and Assisted-Living Solutions

- Persistent Inflation and Real-Wage Pressure Delaying Big-Ticket Purchases

- Volatile Certified Timber, Foam, and Metal Prices Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Home furniture held the largest market share at 57.87% in 2025, while office furniture is projected to grow at a 6.72% CAGR through 2031. Employers standardizing hybrid schedules and retrofitting spaces for collaboration drive this growth. Hybrid routines blur living and working zones, sustaining demand for multiuse sofas, dynamic storage, and compact desks for apartments and small homes. Kitchen cabinetry trends in 2024 varied by country, highlighting the role of housing market momentum in big-ticket installed furniture. Wardrobes and bedroom furniture remained resilient as consumers prioritized personal storage and sleep comfort, offsetting declines in other subcategories. Bathroom furniture benefited from small-space renovations tied to micro-housing programs and urban densification projects, emphasizing compactness and functionality.

Office furniture's recovery is shaped by return-to-office measures and a shift to project-based procurement for contract applications, altering order flows. Germany's midyear data in 2025 showed declining traditional office volumes but improving shop or contract activity, indicating a move toward broader project-based layouts. In France, sealed private offices gave way to shared and collaborative spaces, boosting demand for acoustic pods and adjustable desks with integrated power and charging.

Hospitality furniture gained traction with tourism recovery and hotel renovation projects in Southern Europe, with Spain's island destinations leading. France's reuse quotas in public procurement are fostering repair and refurbishment ecosystems, extending institutional furniture life cycles.

Wood held a 51.87% share in the market in 2025, supported by certification, consumer preference for natural finishes, and reliable supply in European regions. Compliance costs and upstream volatility remain challenges, but certified wood and recycled content in panels and boards are scaling in production. Circular material choices are increasingly integrated into product development, with higher recovery rates from wood waste and a growing share of recycled wood in board inputs reported by industry associations. Metal frames and components are essential in office seating, outdoor environments, and contract applications requiring durability and structural integrity. Energy conditions for metals and fabrication influence pricing and margins, with the net effect depending on the balance between lower commodity prices and higher energy costs.

Plastics and polymers are expected to grow fastest at a 6.38% CAGR through 2031, driven by circular design and recyclability mandates. Prototypes and product lines using post-consumer and post-industrial inputs demonstrate compliance with technical standards and viable performance in emerging applications. Large retailers are retooling packaging and small component choices to reduce plastics and support recyclability goals. Paints and coatings are adapting to stricter emissions standards, with producers advancing alternative chemistries aligned with indoor air quality targets. Polymer-based parts and recycled composites are expanding into seating shells, tabletops, and decorative elements at scale.

List of Companies Covered in this Report:

- IKEA

- Natuzzi S.p.A.

- Poltrona Frau Group

- Roche Bobois SA

- BoConcept Holding A/S

- B&B Italia

- Calligaris S.p.A.

- Molteni &C S.p.A.

- Fritz Hansen A/S

- Ligne Roset

- Hulsta-Werke Huls GmbH

- JYSK Holding A/S

- The Sofa & Chair Company

- Vitra International AG

- Nobia AB

- Howdens Joinery Group

- Wayfair Inc. (Europe Operations)

- MillerKnoll Inc.

- Kave Home, S.L.U.

- HNI Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU "Renovation Wave" Grants & Energy-Efficiency Retrofits Triggering Large-Scale Furniture Replacement

- 4.2.2 Rapid Net Household Formation via Build-to-Rent & Urban Micro-Housing Projects

- 4.2.3 Ageing Demographics Boosting Spend on Ergonomic & Assisted-Living Furniture Solutions

- 4.2.4 Hybrid Work Normalisation Sustaining Demand for Home-Office & Modular Workspace Furniture

- 4.2.5 Tourism Revival & Hotel Pipeline Expansion Accelerating Hospitality Furniture Consumption

- 4.2.6 Cross-Border E-commerce, BNPL Financing & OSS VAT Regime Broadening Consumer Access to Mid-Range Furniture

- 4.3 Market Restraints

- 4.3.1 Persistent Inflation and Real-Wage Pressure Delaying Big-Ticket Furniture Purchases

- 4.3.2 Volatile FSC-Certified Timber, Foam & Metal Prices Inflating Retail Pricing and Squeezing Margins

- 4.3.3 Mature Western European Markets Facing Lengthening Replacement Cycles & Saturation

- 4.3.4 Strict REACH & Fire-Safety Standards Raising Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (new product launches, investment, capacity expansion, partnerships, acquisitions, etc.) in the Industry

- 4.8 Insights on Regulatory Framework and Industry Policies

5 Market Size & Growth Forecasts

- 5.1 Market Size & Growth Forecasts (Value)

- 5.1.1 By Application

- 5.1.1.1 Home Furniture

- 5.1.1.1.1 Chairs

- 5.1.1.1.2 Tables (side tables, coffee tables, dressing tables, etc.)

- 5.1.1.1.3 Beds

- 5.1.1.1.4 Wardrobes

- 5.1.1.1.5 Sofas

- 5.1.1.1.6 Dining Tables/Dining Sets

- 5.1.1.1.7 Kitchen Cabinets

- 5.1.1.1.8 Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- 5.1.1.2 Office Furniture

- 5.1.1.2.1 Chairs

- 5.1.1.2.2 Tables

- 5.1.1.2.3 Storage Cabinets

- 5.1.1.2.4 Desks

- 5.1.1.2.5 Sofas and Other Soft Seating

- 5.1.1.2.6 Other Office Furniture

- 5.1.1.3 Hospitality Furniture

- 5.1.1.4 Educational Furniture

- 5.1.1.5 Healthcare Furniture

- 5.1.1.6 Other Applications (educational furniture, medical and non-medical furniture, public places, retail malls, etc.)

- 5.1.1.1 Home Furniture

- 5.1.2 By Material

- 5.1.2.1 Wood Furniture

- 5.1.2.2 Metal Furniture

- 5.1.2.3 Plastic & Polymer Furniture

- 5.1.2.4 Other Materials

- 5.1.3 By Price Range

- 5.1.3.1 Economy

- 5.1.3.2 Mid-Range

- 5.1.3.3 Premium

- 5.1.4 By Distribution Channel

- 5.1.4.1 B2C/Retail

- 5.1.4.1.1 Home Centers

- 5.1.4.1.2 Specialty Furniture Stores

- 5.1.4.1.3 Online

- 5.1.4.1.4 Other Distribution Channels

- 5.1.4.2 B2B /Project

- 5.1.4.1 B2C/Retail

- 5.1.5 By Geography

- 5.1.5.1 Germany

- 5.1.5.2 France

- 5.1.5.3 Italy

- 5.1.5.4 Spain

- 5.1.5.5 United Kingdom

- 5.1.5.6 BENELUX

- 5.1.5.7 NORDICS

- 5.1.5.8 Rest of Europe

- 5.1.1 By Application

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 IKEA

- 6.4.2 Natuzzi S.p.A.

- 6.4.3 Poltrona Frau Group

- 6.4.4 Roche Bobois SA

- 6.4.5 BoConcept Holding A/S

- 6.4.6 B&B Italia

- 6.4.7 Calligaris S.p.A.

- 6.4.8 Molteni &C S.p.A.

- 6.4.9 Fritz Hansen A/S

- 6.4.10 Ligne Roset

- 6.4.11 Hulsta-Werke Huls GmbH

- 6.4.12 JYSK Holding A/S

- 6.4.13 The Sofa & Chair Company

- 6.4.14 Vitra International AG

- 6.4.15 Nobia AB

- 6.4.16 Howdens Joinery Group

- 6.4.17 Wayfair Inc. (Europe Operations)

- 6.4.18 MillerKnoll Inc.

- 6.4.19 Kave Home, S.L.U.

- 6.4.20 HNI Corporation

7 Market Opportunities & Future Outlook

- 7.1 Sustainability & Eco-Friendly Furniture

- 7.2 E-commerce and Digital Experience