PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073549

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073549

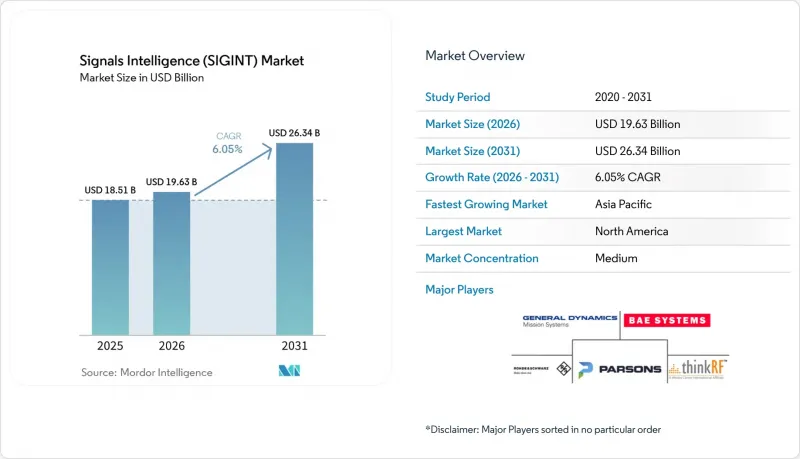

Signals Intelligence (SIGINT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the signals intelligence market size was valued at USD 18.51 billion in 2025 and estimated to grow from USD 19.63 billion in 2026 to reach USD 26.34 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

This report is Segmented by Application (Cyber Intelligence, Ground-Based Intelligence, Naval Intelligence, Space Intelligence, and More), Type (Electronic Intelligence, Communications Intelligence, and More), Platform (Airborne, Ground, and More), Component (Hardware, Software and Analytics, and More), End-User (Defense Forces, Homeland Security and Law Enforcement, and More), and Geography.

Global Signals Intelligence (SIGINT) Market Trends and Insights

AI/ML-Enabled Automated Signal Processing Efficiencies

Project Linchpin is creating a centralized AI ecosystem for the U.S. Army, delivering near-real-time insights that were previously human-intensive. The National Geospatial-Intelligence Agency now circulates AI-generated products, cutting analyst workloads and accelerating tasking cycles. Contractors are investing accordingly; General Atomics acquired North Point Defense in March 2025 to secure proprietary algorithms for autonomous signal processing. DoD AI spending grew from USD 600 million in 2016 to USD 1.8 billion in 2024 across 685 projects. Beyond speed, AI augments resilience by flagging spoofing and jamming attempts that evade rule-based filters.

Multi-Domain Operations Driving Cross-Platform SIGINT Fusion

NATO earmarked EUR 32 million in 2024 for a service-oriented architecture that links airborne early-warning, cyber, and maritime sensors into a single intelligence backbone. The U.S. Fish Hook Undersea Defence Line integrates submarine, surface, and aerial collectors across the Pacific, proving the need for ocean-to-space coverage. In parallel, OneWeb and Eutelsat validated multi-orbit terminals that hand off between GEO and LEO links during NATO exercises. Japan's 2024 surveillance satellite launches support regional monitoring and humanitarian assistance, underscoring dual-use expectations. New data-standard mandates such as STANAG 4774/4778 force vendors to deliver interoperability from day one.

Spectrum Congestion and End-to-End Encryption Challenges

Meta activated default end-to-end encryption for over 1 billion Messenger users in 2024, closing a vast data stream that intelligence agencies once exploited. The Hudson Institute argues that limited U.S. spectrum access could erode tactical options versus well-resourced adversaries. CSIS finds that spectrum availability correlates directly with national security innovation. Agencies respond by increasing cyber insertion and partnering with telecom operators for lawful access, but the margin for traditional over-the-air intercept keeps shrinking.

Other drivers and restraints analyzed in the detailed report include:

- Global Defense-Budget Expansion Across NATO and APAC

- Commercial LEO Mega-Constellations Creating New Intercept Layers

- Cyber-Physical Vulnerabilities at SIGINT Ground Stations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Space Intelligence held 27.84% of the signals intelligence market share in 2025 and is forecast at a 7.09% CAGR through 2031. This slice of the signals intelligence market gains momentum from proliferated LEO constellations that promise persistent coverage even under kinetic attack. The National Reconnaissance Office's USD 2 billion Starshield contract underscores how sovereign buyers prioritize orbital resilience for strategic awareness. Parallel civilian ventures, such as HawkEye 360's RF-mapping service, entice mid-tier militaries that cannot fund sovereign satellites yet require fast cueing.

Airborne Intelligence still captures 27.90% revenue in 2025, supported by NATO's order of six Boeing Wedgetail AEW&C jets, while Japan's dedicated surveillance satellites demonstrate complementary roles for space and air sensors. Ground-based nodes confront increasing cyber-physical risk, prompting hardened shelters and redundant routing. Naval programs benefit from India's USD 2 billion XLUUV procurement, marrying underwater stealth with satellite backhaul. Cyber Intelligence continues to grow as pervasive encryption pushes analysts toward endpoint exploitation. Lawful interception tools face regulatory headwinds, yet remain crucial for domestic security operations.

Electronic Intelligence dominates the signals intelligence market with a 51.35% 2025 share, given its centrality in radar monitoring and electronic-order-of-battle mapping. However, FISINT is pacing an 7.74% CAGR as militaries seek telemetry from missile tests and space launch vehicles. China's Yaogan clusters combine ELINT and synthetic-aperture radar, creating highly granular maritime awareness that nudges regional rivals to invest in comparable FISINT capabilities.

Communications Intelligence remains indispensable for diplomatic monitoring but is hampered by end-to-end encryption that hides voice and text payloads. Consequently, technical disciplines such as ELINT and FISINT supply alternative signatures that evade encryption barriers. Historical growth curves confirm that the signals intelligence industry shifts budget from manpower-intensive voice translation to high-throughput digital demodulation systems that feed AI analytics. This realignment favors vendors offering automated decoding, bit-level parsing, and integrated mission data files.

Complete Report Scope:

- By Application

- Cyber Intelligence (CYBINT)

- Ground-based Intelligence

- Naval Intelligence

- Space Intelligence

- Airborne Intelligence

- Lawful Interception and Telecom Monitoring

- By Type

- Electronic Intelligence (ELINT)

- Communications Intelligence (COMINT)

- Foreign Instrumentation Signals (FISINT)

- By Platform

- Airborne

- Ground

- Naval

- Space

- Unmanned Systems (UAV/UGV/USV)

- Portable/Man-pack

- By Component

- Hardware (Antennas, Receivers, SDRs)

- Software and Analytics

- Services (Integration, Training, MRO)

- By End-user

- Defense Forces

- Homeland Security and Law Enforcement

- Critical Infrastructure Operators

- Commercial Space and Telecom Providers

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America held 41.60% revenue in 2025, bolstered by the nearly USD 100 billion U.S. intelligence budget and the National Reconnaissance Office's large-scale Starshield investment. General Atomics' purchase of North Point Defense shows how domestic primes deepen AI portfolios to defend leadership positions. Supply-chain risk remains a strategic worry because Taiwan still dominates advanced node semiconductor fabrication, highlighting a geopolitical Achilles' heel.

Asia Pacific posts the fastest 8.15% CAGR, propelled by Japan's defense allocation of USD 59 billion in FY 2025 and India's push for sovereign space intelligence infrastructure. China's expanding Yaogan and Qianshao constellations raise the intelligence baseline, compelling neighbors to counter-invest. India's USD 2 billion XLUUV program illustrates maritime focus, while South Korea and Australia accelerate joint AUKUS initiatives to safeguard sea-lanes. Historical spending patterns show a pivot from platform acquisition to data-centric architectures that feed joint commands in near real time.

Europe records steady mid-single-digit growth as NATO harmonizes ISR requirements and the European Commission funds secure satellite connectivity. The EUR 32 million NATO command-and-control upgrade triggers demand for interoperable SIGINT nodes afcea.org. AUKUS export-control waivers accelerate UK collaboration with U.S. integrators, lowering program lead times. Elsewhere, the Middle East and Africa maintain moderate growth anchored in border security, while South American budgets lag amid fiscal constraints and limited access to high-end electronics.

- General Dynamics Mission Systems, Inc.

- BAE Systems plc

- Parsons Corporation

- Rohde and Schwarz GmbH and Co KG

- ThinkRF Corp.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Thales Group

- Elbit Systems Ltd.

- Saab AB

- L3Harris Technologies, Inc.

- Cobham Ltd.

- Leonardo S.p.A.

- HENSOLDT AG

- Raytheon Technologies Corp.

- Boeing Defense, Space and Security

- Airbus Defence and Space

- Israel Aerospace Industries Ltd.

- CACI International Inc.

- Leidos Holdings Inc.

- Palantir Technologies Inc.

- HawkEye 360

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened counter-terrorism and asymmetric warfare focus

- 4.2.2 Multi-domain operations driving cross-platform SIGINT fusion

- 4.2.3 Global defense-budget expansion across NATO and APAC

- 4.2.4 AI/ML-enabled automated signal processing efficiencies

- 4.2.5 Commercial LEO mega-constellations creating new intercept layers

- 4.2.6 SDR commoditization lowering entry barriers for smaller forces

- 4.3 Market Restraints

- 4.3.1 High capital cost of satellite and airborne SIGINT systems

- 4.3.2 Spectrum congestion and end-to-end encryption challenges

- 4.3.3 Tighter export-control regimes on advanced EW modules

- 4.3.4 Cyber-physical vulnerabilities at SIGINT ground stations

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of COVID-19 and Recent Conflicts

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Cyber Intelligence (CYBINT)

- 5.1.2 Ground-based Intelligence

- 5.1.3 Naval Intelligence

- 5.1.4 Space Intelligence

- 5.1.5 Airborne Intelligence

- 5.1.6 Lawful Interception and Telecom Monitoring

- 5.2 By Type

- 5.2.1 Electronic Intelligence (ELINT)

- 5.2.2 Communications Intelligence (COMINT)

- 5.2.3 Foreign Instrumentation Signals (FISINT)

- 5.3 By Platform

- 5.3.1 Airborne

- 5.3.2 Ground

- 5.3.3 Naval

- 5.3.4 Space

- 5.3.5 Unmanned Systems (UAV/UGV/USV)

- 5.3.6 Portable/Man-pack

- 5.4 By Component

- 5.4.1 Hardware (Antennas, Receivers, SDRs)

- 5.4.2 Software and Analytics

- 5.4.3 Services (Integration, Training, MRO)

- 5.5 By End-user

- 5.5.1 Defense Forces

- 5.5.2 Homeland Security and Law Enforcement

- 5.5.3 Critical Infrastructure Operators

- 5.5.4 Commercial Space and Telecom Providers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Israel

- 5.6.5.2 Turkey

- 5.6.5.3 Saudi Arabia

- 5.6.5.4 United Arab Emirates

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Dynamics Mission Systems, Inc.

- 6.4.2 BAE Systems plc

- 6.4.3 Parsons Corporation

- 6.4.4 Rohde and Schwarz GmbH and Co KG

- 6.4.5 ThinkRF Corp.

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 Thales Group

- 6.4.9 Elbit Systems Ltd.

- 6.4.10 Saab AB

- 6.4.11 L3Harris Technologies, Inc.

- 6.4.12 Cobham Ltd.

- 6.4.13 Leonardo S.p.A.

- 6.4.14 HENSOLDT AG

- 6.4.15 Raytheon Technologies Corp.

- 6.4.16 Boeing Defense, Space and Security

- 6.4.17 Airbus Defence and Space

- 6.4.18 Israel Aerospace Industries Ltd.

- 6.4.19 CACI International Inc.

- 6.4.20 Leidos Holdings Inc.

- 6.4.21 Palantir Technologies Inc.

- 6.4.22 HawkEye 360

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment