PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073552

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073552

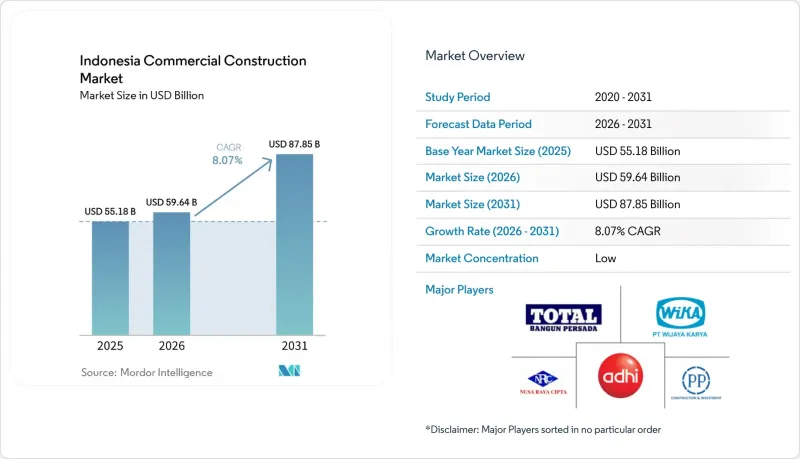

Indonesia Commercial Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia commercial construction market size was valued at USD 55.18 billion in 2025 and estimated to grow from USD 59.64 billion in 2026 to reach USD 87.85 billion by 2031, at a CAGR of 8.07% during the forecast period (2026-2031).

This report is Segmented by Commercial Sector Type (Office, Industrial & Logistics, and Others), by Construction Type (New Construction and Renovation), by Investment Source (Private and Public), and by Region (TDKI Jakarta, West Java (Jawa Barat), and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Indonesia Commercial Construction Market Trends and Insights

Retail chain expansion plans drive urban commercial development

Indonesia's retail sector is witnessing robust growth, fueled by increasing disposable incomes and changing consumer preferences. Modern retail groups are accelerating new mall and lifestyle-center rollouts to capture rising disposable incomes and evolving consumer habits. Retail sales climbed to USD 46.34 billion in 2022 and are forecast to hit USD 71.89 billion by 2031, and developers respond by clustering retail, entertainment, and F&B at high-footfall nodes. Projects such as the USD 2.56 billion PIK 2 township in North Jakarta integrate shops, theme parks, and waterfront promenades in one destination, signaling a pivot toward experiential formats. As land prices inside the capital climb, chains increasingly target satellite cities where plots are larger and zoning is flexible. This steady pipeline sustains demand for architects, MEP consultants, and fit-out specialists across the Indonesia Commercial Construction market.

Corporate demand for Grade-A office space supports premium developments

Corporate demand for Grade-A office spaces is driving premium developments in Jakarta's CBD. Prime office rents in Jakarta's CBD ticked up 0.7% year-on-year in Q3 2024, the first meaningful rise since 2015, reflecting renewed occupier confidence jll.co.id. Despite a still-high 70% occupancy level across 9.3 million sqm, multinationals in tech, finance, and advanced manufacturing are locking in larger floorplates to accommodate back-to-office mandates. Flagship towers such as the 260-meter Sahid Sudirman Center illustrate the shift toward mixed-use vertical campuses that stack offices, retail, and hospitality. Foreign direct investment in manufacturing jumped 18.6% in 2024, linking production expansion with needs for regional headquarters and support services. These trends underpin stable take-up for green, flexible, and digitally enabled workspaces in the Indonesia Commercial Construction market.

High construction input costs pressure project viability

In 2024, cement sales in Indonesia dipped by 0.9% year-on-year, totaling 64.9 million tons. Meanwhile, output saw a modest uptick of 1%. This scenario underscores the margin compression faced by producers grappling with tepid demand. Steel prices, influenced by energy market fluctuations, have been erratic. This volatility has led to a surge in structural frame budgets, escalating costs by as much as 15%. In response, developers are either pivoting to lighter modular designs or intensifying local sourcing efforts when possible. While there's a rising trend in adopting recycled aggregates and low-carbon cement, scaling these practices is essential to bridge existing cost disparities. Given the recent cost surges, many are adopting phased construction strategies. These align cash expenditures with milestones like pre-leases or pre-sales, a trend becoming prominent in Indonesia's commercial construction landscape.

Other drivers and restraints analyzed in the detailed report include:

- Integrated mixed-use projects gain momentum under urban planning frameworks

- Transit-oriented developments transform urban connectivity corridors

- Zoning and permit delays create project execution risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial & logistics assets delivered the fastest 8.93% CAGR forecast between 2026 and 2031, although retail retained a 31.22% Indonesia Commercial Construction market share in 2025. Supply-chain restructuring and e-commerce growth lowered logistics costs to 14.29% of GDP in 2023, down from 23.80% in 2018, catalyzing warehouse and inland-port demand. The New Priok expansion, tripling yearly capacity to 18 million TEU, underscores how port investments trigger adjacent industrial parks and cold-chain hubs. Major developers roll out multi-story fulfillment centers near Jakarta's ring roads to minimize last-mile mileage. Occupiers favor buildings with 12-meter clear heights, 70 kN/sqm floor loading, and solar-ready roofs, a specification set that is becoming the new normal across the Indonesia Commercial Construction market.

In contrast, brick-and-mortar retail pivots toward lifestyle and entertainment offerings that keep dwell times high amid online shopping's rise. Flagship schemes like PIK 2 blend retail with theme parks and waterfront promenades, buffering occupancy risk. Office demand shows nuanced recovery: anchor tenants consolidate older leases into green, tech-rich towers that meet WELL and LEED standards. Indonesia Data-center construction, exemplified by Telkom's 51 MW Batam campus, enters the mainstream "others" bracket, leveraging Indonesia's strategic bandwidth routes. Together, these shifts diversify revenue bases and attract institutional capital into the Indonesia Commercial Construction market.

Complete Report Scope:

- By Commercial Sector Type

- Office

- Retail

- Industrial and Logistics

- Others

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Region

- DKI Jakarta

- West Java (Jawa Barat)

- East Java (Jawa Timur)

- Rest of Indonesia

List of Companies Covered in this Report:

- PT PP(Persero) Tbk

- PT Wijaya Karya Tbk

- PT Total Bangun Persada Tbk

- PT Nusa Raya Cipta Tbk

- PT Adhi Karya Tbk

- PT Metropolitan Land Tbk

- PT SuryaSemesta Internusa Tbk

- PT Ciputra Development Tbk

- PT Pakuwon Jati Tbk

- The Mulia Group

- PT Tatamulia Nusantara Indah

- PT Tunas Jaya Sanur

- PT Shimizu Bangun Cipta Kontraktor

- PT Takenaka Indonesia

- PT Obayashi Indonesia

- PT TOKYU Construction Indonesia

- PT Jaya Konstruksi Manggala Pratama Tbk

- PT Bumi Karsa

- PT Gunung Sewu Group (Farpoint)

- PT Agung Podomoro Land Tbk

- PT Lippo Karawaci Tbk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Retail chain expansion plans are driving mall and lifestyle center construction in major cities.

- 4.2.2 Corporate demand for Grade-A office space is supporting developments in Jakarta and tier-2 cities.

- 4.2.3 Integrated mixed-use projects are gaining traction under city-led development frameworks.

- 4.2.4 Transit-oriented developments (TODs) are emerging near new rail and toll road corridors.

- 4.2.5 Tourism sector recovery is fueling hotel, resort, and supporting retail construction.

- 4.2.6 Increased foreign participation is boosting investments in commercial and high-rise assets.

- 4.3 Market Restraints

- 4.3.1 High construction input costs are putting pressure on commercial project margins.

- 4.3.2 Zoning and permit delays continue to slow project approvals and groundbreakings.

- 4.3.3 Financing limitations are affecting speculative and mid-scale commercial developments.

- 4.3.4 Excess office and retail supply in some urban markets is dampening new launches.

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights

- 4.4.3 Architectural and Engineering Companies - Key Quantitative and Qualitative Insights

- 4.4.4 Building Material and Equipment Companies - Key Quantitative and Qualitative Insights

- 4.5 Government Initiatives & Vision

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing (Construction Materials) and Construction Cost (Materials, Labour, Equipment) Analysis

- 4.10 Comparison of Key Industry Metrics of Indonesia with Other Countries

- 4.11 Key Upcoming/Ongoing Projects (with a focus on Mega Projects)

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Commercial Sector Type

- 5.1.1 Office

- 5.1.2 Retail

- 5.1.3 Industrial and Logistics

- 5.1.4 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By Investment Source

- 5.3.1 Public

- 5.3.2 Private

- 5.4 By Region

- 5.4.1 DKI Jakarta

- 5.4.2 West Java (Jawa Barat)

- 5.4.3 East Java (Jawa Timur)

- 5.4.4 Rest of Indonesia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 PT PP(Persero) Tbk

- 6.4.2 PT Wijaya Karya Tbk

- 6.4.3 PT Total Bangun Persada Tbk

- 6.4.4 PT Nusa Raya Cipta Tbk

- 6.4.5 PT Adhi Karya Tbk

- 6.4.6 PT Metropolitan Land Tbk

- 6.4.7 PT SuryaSemesta Internusa Tbk

- 6.4.8 PT Ciputra Development Tbk

- 6.4.9 PT Pakuwon Jati Tbk

- 6.4.10 The Mulia Group

- 6.4.11 PT Tatamulia Nusantara Indah

- 6.4.12 PT Tunas Jaya Sanur

- 6.4.13 PT Shimizu Bangun Cipta Kontraktor

- 6.4.14 PT Takenaka Indonesia

- 6.4.15 PT Obayashi Indonesia

- 6.4.16 PT TOKYU Construction Indonesia

- 6.4.17 PT Jaya Konstruksi Manggala Pratama Tbk

- 6.4.18 PT Bumi Karsa

- 6.4.19 PT Gunung Sewu Group (Farpoint)

- 6.4.20 PT Agung Podomoro Land Tbk

- 6.4.21 PT Lippo Karawaci Tbk

7 Market Opportunities & Future Outlook