PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073555

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073555

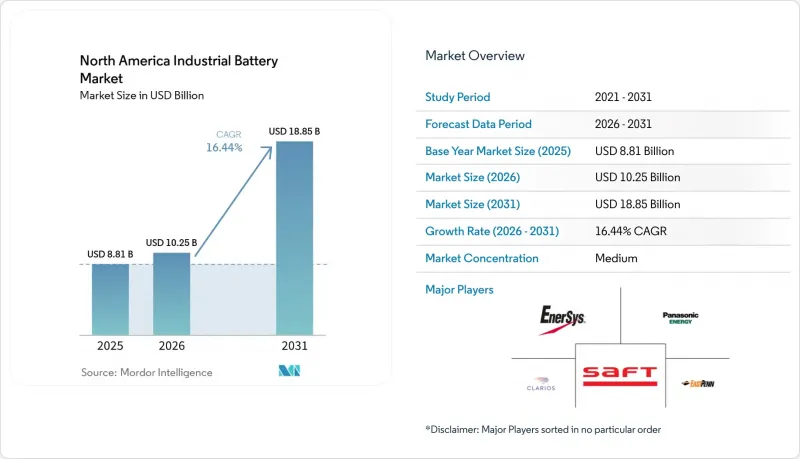

North America Industrial Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america industrial battery market size is projected to be USD 8.81 billion in 2025, USD 10.25 billion in 2026, and reach USD 18.85 billion by 2031, growing at a CAGR of 16.44% from 2026 to 2031.

This report is Segmented by Technology (Lithium-Ion, Lead-Acid, Nickel-Based, Flow & Zinc-Hybrid, Others), Application (Forklift & Automated Material Handling, Telecom Backup, UPS & Data-Center, Renewable-Integrated Industrial ESS, Rail & Marine Auxiliary Power), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Industrial Battery Market Trends and Insights

Grid-Service "Battery-as-a-Weapon" Contracts for Data-Center Resiliency

The North America industrial batteries market is seeing data centers emerge as the most important new demand center for large-scale UPS and resiliency systems. NERC issued a Level 3 Alert on May 7, 2026, and identified AI-driven hyperscale loads as a reliability risk to the US bulk power system, which raised the value of fast-response industrial batteries in critical facilities. This shift matters because battery systems are no longer being purchased only for emergency backup, they are now being evaluated as assets that can stabilize voltage, manage short-duration load swings, and support continuity in high-density compute environments. Fluence reported a contracted backlog of USD 5.6 billion as of March 2026 and signed master supply agreements with 2 major hyperscalers in fiscal Q2 2026, showing that the North America industrial batteries market is already converting this demand into booked revenue. As a result, the North America industrial batteries market is gaining support from a use case where reliability value and potential grid-service value are being assessed together instead of separately.

IRA Tax-Credit Stack for North America-Sourced Cells and Critical Minerals

The IRA production credit framework remains one of the clearest structural supports for the North America industrial batteries market. EnerSys recognized USD 136.4 million in Section 45X credits in fiscal 2024, up from USD 17.3 million in fiscal 2023, which shows how quickly compliant domestic production can change the cost position of established manufacturers. Fluence also reported USD 10.9 million in IRA-linked cost reductions in the first half of fiscal 2026 tied to its Utah battery module manufacturing, confirming that these incentives are already influencing margin structures in the North America industrial batteries market. The OBBBA restrictions that tighten prohibited foreign entity content from 2026 through 2030 deepen this advantage, because access to federal-linked demand increasingly depends on domestic sourcing compliance rather than price alone. This is reshaping procurement decisions across the North America industrial batteries market, especially for suppliers that can offer cells, modules, and pack integration from a traceable North American base.

Workplace Fire-Code Liabilities for High-Energy LFP Installations

The North America industrial batteries market faces a real execution constraint from tighter fire-code requirements around stationary storage. The 2026 edition of NFPA 855 raised the compliance threshold for many industrial installations by requiring Hazard Mitigation Analysis more broadly and reinforcing large-scale fire testing expectations for qualifying systems. Installations above 600 kWh now face stricter room design and explosion-prevention expectations, which raises project design cost and can complicate retrofits in existing warehouses and manufacturing sites. These rules do not stop deployment in the North America industrial batteries market, but they do extend approval cycles and make system selection more dependent on documentation, testing history, and installer experience. The burden is heavier for smaller suppliers, while larger integrators with tested and listed systems can move through the permitting process with fewer delays.

Other drivers and restraints analyzed in the detailed report include:

- Surging Automated-Warehouse Build-Outs Demanding 24X7 Motive Power (AGV/AMR)

- Commitment-Driven Fleet Electrification Mandates

- Lead Recycling Bottlenecks Amid Tightened EPA Thresholds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 59.2% of the North America industrial batteries market share in 2025, which confirms that it has become the default chemistry across high-cycle industrial use cases. The North America industrial batteries industry has moved steadily in this direction for several years, as US domestic manufacturing data already showed lead-acid shipment value falling from USD 5.3 billion in 2013 to USD 2.2 billion in 2022 while non-lead-acid output rose from USD 0.7 billion to USD 16.6 billion over the same period. This shift continued through 2025 and 2026 because maintenance-free operation, better cycling performance, and stronger compatibility with automated duty cycles make lithium-ion easier to justify on a total ownership basis. EnerSys's decision to close its Tijuana lead-acid plant and shift production to Springfield, Missouri shows how incumbent suppliers are redirecting capital toward product lines and manufacturing footprints that fit the new structure of the North America industrial batteries market.

Flow & Zinc-hybrid is projected to expand at an 18.3% CAGR through 2031, making it the fastest-growing technology group in the North America industrial batteries market. The appeal of these long-duration chemistries is strongest in industrial microgrids and renewable-linked installations where discharge duration, non-flammability, or operating flexibility can outweigh the space and cost advantages of mainstream lithium systems. This opens a wider technology mix than the headline share split suggests, because the North America industrial batteries industry is not moving toward a single chemistry for every application. Nickel-based batteries still retain relevance in temperature-variable telecom, rail auxiliary power, and other high-reliability settings where stability under harsher operating conditions remains more important than absolute cost. The practical result is that lithium-ion will continue to dominate the North America industrial batteries market by value, but long-duration and niche chemistries will capture a larger share of new projects where application needs are more specific than simple backup power.

Complete Report Scope:

- By Technology

- Lithium-ion

- Lead-acid

- Nickel-based

- Flow & Zinc-hybrid

- Others

- By Application

- Forklift & Automated Material Handling

- Telecom Backup

- UPS & Data-Center

- Renewable-integrated Industrial ESS

- Rail & Marine Auxiliary Power

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- EnerSys

- East Penn Manufacturing

- Exide Technologies

- Saft Groupe SA

- C&D Technologies

- Panasonic Energy (Panasonic Holdings)

- GS Yuasa Corp.

- Leoch International

- Crown Battery Mfg. Co.

- Clarios

- Tesla (Megapack & Industrial Storage)

- BYD Company Ltd.

- LG Energy Solution

- KORE Power

- Fluence Energy

- ABB (BESS division)

- Mitsubishi Power Americas

- EVE Energy USA

- Navitas Systems

- Amara Raja Batteries USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commitment-driven fleet electrification mandates (post-2026 purchase incentives)

- 4.2.2 Surging automated-warehouse build-outs demanding 24/7 motive-power (AGV/AMR)

- 4.2.3 Grid-service "battery-as-a-weapon" contracts for data-center resiliency

- 4.2.4 Declining USD/kWh lithium-ion pack costs

- 4.2.5 OEM shift from flooded lead-acid to maintenance-free chemistries

- 4.2.6 IRA tax-credit stack for NA-sourced cells and critical minerals

- 4.3 Market Restraints

- 4.3.1 Scarcity of regional Class-1 nickel & battery-grade manganese refining

- 4.3.2 Workplace fire-code liabilities for high-energy LFP installations

- 4.3.3 Lead recycling bottlenecks amid tightened EPA thresholds

- 4.3.4 Capital-intensive cell manufacturing vs. volatile forklift demand cycle

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Pricing Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Nickel-based

- 5.1.4 Flow & Zinc-hybrid

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Forklift & Automated Material Handling

- 5.2.2 Telecom Backup

- 5.2.3 UPS & Data-Center

- 5.2.4 Renewable-integrated Industrial ESS

- 5.2.5 Rail & Marine Auxiliary Power

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 EnerSys

- 6.4.2 East Penn Manufacturing

- 6.4.3 Exide Technologies

- 6.4.4 Saft Groupe SA

- 6.4.5 C&D Technologies

- 6.4.6 Panasonic Energy (Panasonic Holdings)

- 6.4.7 GS Yuasa Corp.

- 6.4.8 Leoch International

- 6.4.9 Crown Battery Mfg. Co.

- 6.4.10 Clarios

- 6.4.11 Tesla (Megapack & Industrial Storage)

- 6.4.12 BYD Company Ltd.

- 6.4.13 LG Energy Solution

- 6.4.14 KORE Power

- 6.4.15 Fluence Energy

- 6.4.16 ABB (BESS division)

- 6.4.17 Mitsubishi Power Americas

- 6.4.18 EVE Energy USA

- 6.4.19 Navitas Systems

- 6.4.20 Amara Raja Batteries USA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment