PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073563

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073563

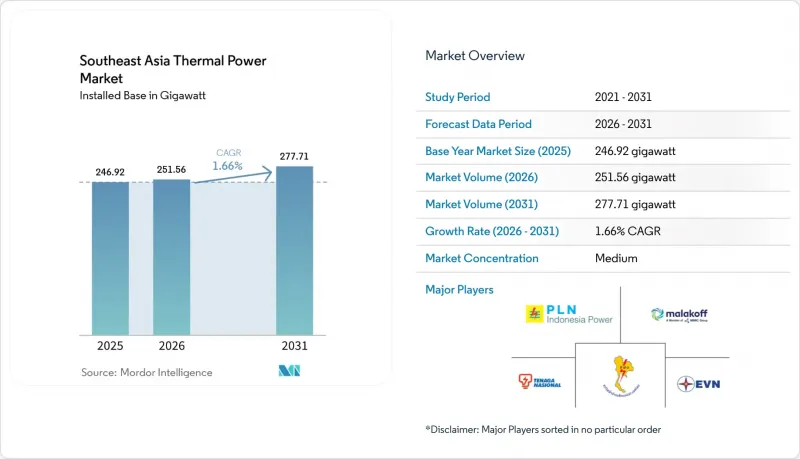

Southeast Asia Thermal Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the southeast asia thermal power market size in terms of installed base is projected to be 246.92 gigawatt in 2025, 251.56 gigawatt in 2026, and reach 277.71 gigawatt by 2031, growing at a CAGR of 1.66% from 2026 to 2031.

This report is Segmented by Fuel Type (Coal-Fired, Gas-Fired, Oil-Fired), Technology (Steam Cycle, Gas Turbine/CC, CHP), Combustion Method (PF, FBC, Gasification, ICE, Turbine-Based), Application (Utility-Scale, Captive, Distributed, Peaker), and Geography (Vietnam, Indonesia, Philippines, Thailand, Malaysia, Singapore, Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Volume (GW).

Southeast Asia Thermal Power Market Trends and Insights

Surging Baseload Demand from Industrialisation

Manufacturing relocation is pushing concentrated electricity demand into Southeast Asian grids that were not built for such rapid industrial load growth. Indonesia is at the center of this shift, as its nickel-processing corridor and other resource-based industrial clusters require round-the-clock power and continue to favor thermal generation for reliability and cost visibility . In this setting, captive coal and gas plants remain the preferred option because they can deliver firm output at the scale needed by smelters and other continuous-process facilities. Captive coal capacity in Indonesia reached 16.6 GW in 2024, and another 14 GW was either planned or under construction, which shows how industrial demand is expanding outside the grid-connected coal moratorium framework. This shadow build-out means the Southeast Asia thermal power market is larger in practice than public utility statistics alone would suggest.

Expansion of LNG-to-Power Value Chains

Vietnam's LNG-to-power program moved from policy ambition to project execution in 2026. PetroVietnam Power's Nhon Trach 3 and 4 plants entered commercial operation on January 5, 2026, as the country's first LNG-fired facility, using GE Vernova 9HA.02 turbines and a 25-year LNG supply contract with PV Gas. EVN then moved ahead with the Quang Trach II EPC contract, and the Ca Na LNG project reached financial close in April 2026 as the first LNG project selected through international competitive bidding under PDP VIII. The main challenge is not only fuel supply or equipment access, but also whether power purchase agreements can allocate risk in a way that supports project finance. Vietnam's Energy Regulatory Authority stated in May 2026 that current PPAs still do not provide adequate risk-sharing between the state and investors.

Stricter ESG Lending and Multilateral Exit

Financing conditions are tighter than they were earlier in the decade, even though natural gas still qualifies as a transition fuel under the ASEAN Taxonomy for Sustainable Finance. The 2025 divestment scorecard still showed large cumulative coal and gas financing in the region through 2024, with international banks and JBIC continuing to play major roles in project support. The harder constraint now comes from multilateral and blended-finance structures, because early retirement models still struggle when governments resist recognizing unrecovered capital losses. The cancellation of the Cirebon-1 early-retirement effort showed that even high-profile transition structures can fail when political alignment and compensation terms do not hold. This leaves the Southeast Asia thermal power market in a financing middle ground where gas remains bankable in many cases, but coal retirement is still slow and difficult.

Other drivers and restraints analyzed in the detailed report include:

- Policy Focus on Grid Stability & Energy Security

- Rise of Captive On-Site Power for Data Centres

- Rapid LCOE Decline of Solar-Battery Hybrids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coal-fired power plants held 58.1% share of installed thermal capacity in 2025, which kept coal as the largest fuel base in the Southeast Asia thermal power market. That dominance remained anchored by Indonesia's 57 GW fleet and by Vietnam's continued reliance on coal within its existing generation mix. New coal development outside Indonesia has already slowed sharply, and the most visible recent proposals have been tied to captive industrial use rather than utility-grid expansion. Natural gas-fired power plants are the fastest-growing fuel segment, with 4.9% CAGR projected through 2031 as LNG-to-power pipelines move forward in Vietnam, Malaysia, and the Philippines.

Vietnam's operating mix still showed how far the transition has to go, because EVN reported that coal thermal contributed 52.8% of electricity output in the first quarter of 2026, while gas turbines contributed 7%. Even so, that gap is likely to narrow as LNG plants move from contract award to operation over the next several years. Oil-fired plants remain a residual part of the mix and continue to serve emergency peaking roles in the Philippines and in remote Indonesian island systems where grid and fuel options remain limited. The Southeast Asia thermal power market is therefore still coal-heavy in the near term, but its new-build path is moving toward gas, efficiency, and greater fuel flexibility.

Gas turbine and combined cycle technology claimed 48.3% of installed thermal capacity in 2025, and it is projected to grow at 2.1% CAGR through 2031. This position reflects decades of investment in Singapore, Thailand, and Malaysia, where gas-based fleets were built earlier and where efficiency standards are now steering replacement decisions toward modern combined-cycle assets. The next phase of growth is coming less from single mega projects and more from a broad wave of medium-scale replacements for aging open-cycle gas units. Steam cycle plants still hold a large base because they represent most of the coal fleet in Indonesia and Vietnam, and many of those assets will remain operational through the forecast period.

Utilities are trying to extend the relevance of steam-cycle assets through ultra-supercritical upgrades and biomass co-firing programs. PLN Energi Primer Indonesia supplied 460,368 tonnes of biomass for co-firing in the first quarter of 2026 after supplying 2.4 million tonnes during 2025, which shows that retrofit activity is moving from the pilot stage to broader execution. Combined heat and power remains underused in the Southeast Asia thermal power industry, even though industrial clusters in Johor and Selangor are well suited to facilities that can supply both electricity and process heat. Mitsubishi Power's O Mon 4 award in Vietnam, using JAC-series gas turbines with combined-cycle efficiency above 64%, shows that the Southeast Asia thermal power industry is rewarding high-efficiency platforms that can make older steam-cycle assets look less competitive over time.

Complete Report Scope:

- By Fuel Type

- Coal-Fired Power Plants

- Natural Gas-Fired Power Plants

- Oil-Fired Power Plants

- By Technology

- Steam Cycle-Based

- Gas Turbine/Combined Cycle

- Combined Heat and Power (CHP)

- By Combustion Method

- Pulverized Fuel (PF) Combustion

- Fluidized Bed Combustion

- Gasification

- Internal Combustion Engines

- Turbine-Based Combustion

- By Application

- Utility-Scale Thermal Plants

- Industrial Captive Power Plants

- Distributed Thermal Plants

- Peaker Plants

- By Geography

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

- Singapore

- Rest of Southeast Asia

List of Companies Covered in this Report:

- PT PLN (Persero)

- Vietnam Electricity (EVN)

- Electricity Generating Authority of Thailand (EGAT)

- Malakoff Corporation Berhad

- First Gen Corporation

- Aboitiz Power Corp

- Tenaga Nasional Berhad

- PETRONAS Gas Berhad

- PT Adaro Energy Indonesia Tbk

- PT Bayan Resources Tbk

- Vinacomin (TKV)

- JERA Co. Inc.

- KEPCO Engineering & Construction

- Siemens Energy AG

- General Electric Co.

- Mitsubishi Power

- Shanghai Electric Group

- Doosan Enerbility

- Babcock & Wilcox

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging baseload demand from industrialisation

- 4.2.2 Expansion of LNG to Power value chains

- 4.2.3 Policy focus on grid stability & energy security

- 4.2.4 Financing of HELE coal by Japan & Korea

- 4.2.5 Rise of captive on-site power for data centres

- 4.2.6 Carbon-credit upside from coal/biomass co-firing

- 4.3 Market Restraints

- 4.3.1 Stricter ESG lending & multilateral exit

- 4.3.2 Rapid LCOE decline of solar-battery hybrids

- 4.3.3 Upstream gas decline in ID & MY raising supply risk

- 4.3.4 ASEAN power-grid trade curbing new builds

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Coal-Fired Power Plants

- 5.1.2 Natural Gas-Fired Power Plants

- 5.1.3 Oil-Fired Power Plants

- 5.2 By Technology

- 5.2.1 Steam Cycle-Based

- 5.2.2 Gas Turbine/Combined Cycle

- 5.2.3 Combined Heat and Power (CHP)

- 5.3 By Combustion Method

- 5.3.1 Pulverized Fuel (PF) Combustion

- 5.3.2 Fluidized Bed Combustion

- 5.3.3 Gasification

- 5.3.4 Internal Combustion Engines

- 5.3.5 Turbine-Based Combustion

- 5.4 By Application

- 5.4.1 Utility-Scale Thermal Plants

- 5.4.2 Industrial Captive Power Plants

- 5.4.3 Distributed Thermal Plants

- 5.4.4 Peaker Plants

- 5.5 By Geography

- 5.5.1 Vietnam

- 5.5.2 Indonesia

- 5.5.3 Philippines

- 5.5.4 Thailand

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of Southeast Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PT PLN (Persero)

- 6.4.2 Vietnam Electricity (EVN)

- 6.4.3 Electricity Generating Authority of Thailand (EGAT)

- 6.4.4 Malakoff Corporation Berhad

- 6.4.5 First Gen Corporation

- 6.4.6 Aboitiz Power Corp

- 6.4.7 Tenaga Nasional Berhad

- 6.4.8 PETRONAS Gas Berhad

- 6.4.9 PT Adaro Energy Indonesia Tbk

- 6.4.10 PT Bayan Resources Tbk

- 6.4.11 Vinacomin (TKV)

- 6.4.12 JERA Co. Inc.

- 6.4.13 KEPCO Engineering & Construction

- 6.4.14 Siemens Energy AG

- 6.4.15 General Electric Co.

- 6.4.16 Mitsubishi Power

- 6.4.17 Shanghai Electric Group

- 6.4.18 Doosan Enerbility

- 6.4.19 Babcock & Wilcox

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment