PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073566

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073566

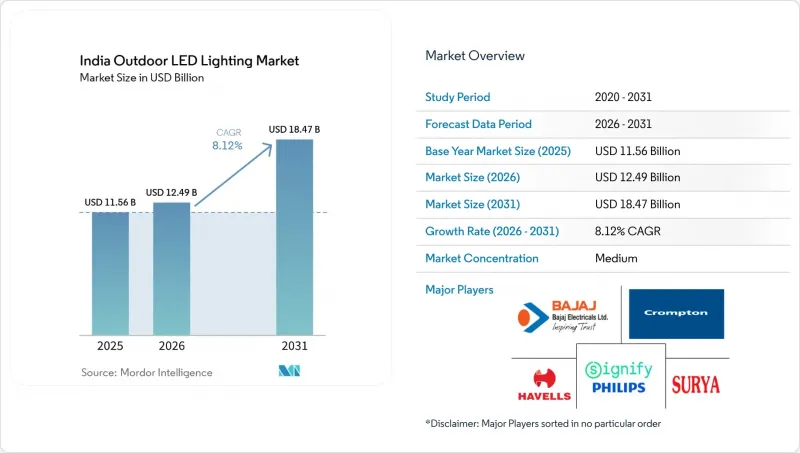

India Outdoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india outdoor LED lighting market size was valued at USD 11.56 billion in 2025 and estimated to grow from USD 12.49 billion in 2026 to reach USD 18.47 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031).

This report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Application (Street and Roadway Lighting, Architectural and Landscape, and More), Installation Type (New Installation, and Retrofit Installation), Distribution Channel (Direct Sales, Wholesale, Retail, and E-Commerce). The Market Forecasts are Provided in Terms of Value (USD).

India Outdoor LED Lighting Market Trends and Insights

Government-Led Smart Cities and Streetlight National Programme

The central government's Revamped Distribution Sector Scheme has earmarked INR 3,037.58 billion (USD 34.22) billion over five years, with LED streetlighting positioned as a cornerstone of every city-level proposal. Energy Efficiency Services Limited (EESL) aggregates municipal demand, enabling bulk procurement discounts of 15-25% compared to standalone tenders. Meanwhile, standardized Bureau of Energy Efficiency (BEE) guidelines streamline the technical evaluation process. Early deployments in Pune, Surat, and Varanasi demonstrated immediate energy savings of 40-50%, catalyzing replication in peer cities. As more municipalities witness verified bill reductions and reduced maintenance truck-rolls, LED conversion becomes an operational imperative rather than a discretionary upgrade. The program's built-in measurement and verification protocols further build lender confidence, unlocking concessional finance from public-sector banks.

Falling LED Chip and Driver Costs Reduce TCO

Semiconductor process improvements and domestic driver assembly have driven down average packaged LED prices by nearly 14% between 2023 and 2025, while driver costs fell 11% over the same period. Because chips and drivers jointly account for nearly two-thirds of a streetlight's bill of materials, these declines materially lower capex per pole. Lifecycle economics improve even further when longer service lives, often exceeding 80,000 hours, and higher luminous efficacies trim maintenance dispatches and electricity bills. Consequently, municipalities replacing 130 W sodium lamps with 70 W LED equivalents achieve 46% electricity cost savings and 32% annual savings per fixture, reducing payback periods to under 18 months. Price erosion is likely to persist as domestic fabs scale under PLI subsidies.

High Up-Front Retrofit Capex for Municipalities

Full-scale citywide LED retrofits can exceed 200% of an average municipality's annual lighting budget for lighting in India, creating an immediate financial hurdle despite the attractive lifecycle benefits. EESL's super-ESCO model offers performance-based contracts funded through energy savings, yet many smaller cities hesitate to sign 7-10 year commitments amid concerns about offtake guarantees and long-term liability. The central government's Payment Security Mechanism, recently trialed in e-bus procurement, introduces escrow guarantees that could ease vendor concerns but remains in nascent stages for lighting.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Energy-Efficiency Codes for Public Infrastructure

- Local Manufacturing Incentives (PLI) for LED Components

- Thermal and Dust-Induced Degradation in Tropical Conditions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires and fixtures secured 72.86% of 2025 revenue, reflecting municipal preference for turnkey assemblies that combine optical, thermal, and driver elements in sealed housings compliant with IP 65 or higher. This dominance stems from procurement simplicity, with one tender and one warranty, and reduced integration risk at the pole. In value terms, the India outdoor LED lighting market size for luminaires is forecast to widen steadily through 2031 as greenfield builds specify integrated units from the outset. Lamps, by contrast, recorded the quickest 9.02% CAGR outlook, due mainly to retrofit programs where existing poles remain structurally sound. These screw-in or plug-in modules enable cash-strapped municipalities to convert legacy heads without civil works, often reducing replacement costs by 35-40%.

Technological convergence also boosts the lamp category. Miniaturized chip-on-board arrays now deliver 120 lm/W efficacy in compact E27 formats, narrowing performance gaps with fixture-grade optics. Field-replaceable LED engines extend service life because municipalities can swap failed modules rather than entire housings, lowering the total cost of ownership. BIS Quality Control Orders enforce IS 16103-2 across both categories, standardizing lumen maintenance and ingress protection benchmarks that underpin multi-vendor interoperability. While luminaires will continue to anchor large-scale smart-pole deployments, lamp retrofits keep growth brisk in secondary cities where budgets remain tight yet energy codes are tightening.

Street and roadway projects maintained a 45.88% revenue share in 2025, thanks to their substantial asset base and direct alignment with traffic safety mandates. Smart Cities guidance encourages the incorporation of adaptive dimming and central management systems, positioning streetlights as the backbone for urban IoT meshes. The India outdoor LED lighting market share of sports and stadium applications, however, is climbing fastest, supported by a 10.10% CAGR prospect. Landmark builds, such as the 132,000-seat Amaravati arena and specialized trident floodlights deployed in Varanasi, illustrate how high-mast, glare-controlled arrays push average selling prices 2-3 times above those of roadway units.

Beyond marquee stadiums, regional cricket grounds, municipal soccer fields, and school complexes are upgrading to LED to satisfy broadcast-quality lux levels and reduce maintenance during tournament schedules. Architectural lighting for heritage facades and riverfront promenades is another niche expanding on the back of tourism-driven beautification schemes. Tunnel and bridge lighting garners steady orders as national highway widening and metro construction progress, requiring vibration-resistant, IP 67-rated luminaires. Taken together, these diverse application clusters reinforce a demand pattern that balances high-volume roadway contracts with premium-priced specialty jobs.

Complete Report Scope:

- By Product Type

- Lamps

- Luminaires / Fixtures

- By Application

- Street and Roadway Lighting

- Architectural and Landscape

- Sports and Stadium

- Tunnel and Bridge

- Parking and Transit Areas

- Other Applications

- By Installation Type

- New Installation

- Retrofit Installation

- By Distribution Channel

- Direct Sales

- Wholesale

- Retail

- E-commerce

List of Companies Covered in this Report:

- Signify N.V.

- Bajaj Electricals Limited

- Havells India Limited

- Crompton Greaves Consumer Electricals Limited

- Wipro Enterprises Private Limited

- Syska LED Lights Private Limited

- Surya Roshni Limited

- Osram Licht AG

- Panasonic Holdings Corporation

- Eaton Corporation plc

- Acuity Brands, Inc.

- Cree, Inc. (Wolfspeed, Inc.)

- Eveready Industries India Limited

- Orient Electric Limited

- LEDVANCE GmbH

- K-Lite Industries

- HPL Electric and Power Limited

- Delta Electronics, Inc.

- Philips Lighting Electronics (India) Ltd.

- GE Current, a Daintree company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-led Smart Cities and Street-Light National Programme

- 4.2.2 Falling LED Chip and Driver Costs Reducing TCO

- 4.2.3 Mandatory Energy-Efficiency Codes for Public Infrastructure

- 4.2.4 Local Manufacturing Incentives (PLI) for LED Components

- 4.2.5 IoT-Enabled Adaptive Lighting for Traffic and Safety Analytics

- 4.2.6 ESCO-Based Municipal Financing Models Expanding

- 4.3 Market Restraints

- 4.3.1 High Up-front Retrofit Capex for Municipalities

- 4.3.2 Thermal and Dust-Induced Degradation in Tropical Conditions

- 4.3.3 Fragmented Optical and Electrical Standards across States

- 4.3.4 Delays in Utility Approvals for Smart-Pole Integration

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on The Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Application

- 5.2.1 Street and Roadway Lighting

- 5.2.2 Architectural and Landscape

- 5.2.3 Sports and Stadium

- 5.2.4 Tunnel and Bridge

- 5.2.5 Parking and Transit Areas

- 5.2.6 Other Applications

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Wholesale

- 5.4.3 Retail

- 5.4.4 E-commerce

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Bajaj Electricals Limited

- 6.4.3 Havells India Limited

- 6.4.4 Crompton Greaves Consumer Electricals Limited

- 6.4.5 Wipro Enterprises Private Limited

- 6.4.6 Syska LED Lights Private Limited

- 6.4.7 Surya Roshni Limited

- 6.4.8 Osram Licht AG

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 Eaton Corporation plc

- 6.4.11 Acuity Brands, Inc.

- 6.4.12 Cree, Inc. (Wolfspeed, Inc.)

- 6.4.13 Eveready Industries India Limited

- 6.4.14 Orient Electric Limited

- 6.4.15 LEDVANCE GmbH

- 6.4.16 K-Lite Industries

- 6.4.17 HPL Electric and Power Limited

- 6.4.18 Delta Electronics, Inc.

- 6.4.19 Philips Lighting Electronics (India) Ltd.

- 6.4.20 GE Current, a Daintree company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment