PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073570

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073570

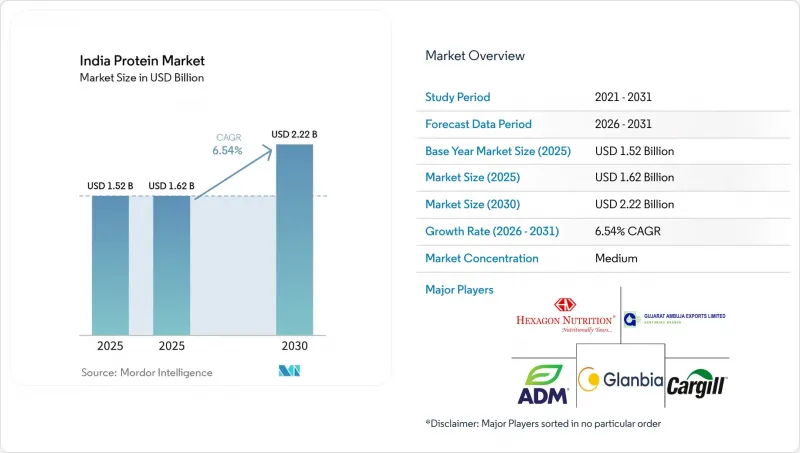

India Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india protein market size is projected to expand from USD 1.52 billion in 2025 and USD 1.62 billion in 2026 to USD 2.22 billion by 2031, registering a CAGR of 6.54% between 2026 to 2031.

This report is Segmented by Source (Animal, Microbial, Plant), Form (Concentrates, Isolates, Hydrolysates, Other Forms), Application (Food and Beverages, Personal Care and Cosmetics, Animal Feed, Dietary Supplements and Sports Nutrition), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

India Protein Market Trends and Insights

Growing mainstream adoption of high-protein diets and sports nutrition

Protein consumption is transitioning from a gym-centric niche to a mainstream dietary priority, catalyzed by the COVID-19 pandemic's emphasis on immunity and long-term health resilience. The sports nutrition and dietary supplements segment is forecast to grow at a 6.6% CAGR, according to the India Brand Equity Foundation. This expansion is underpinned by rising gym memberships, fitness app adoption, and the normalization of protein supplementation among non-athletes, including working professionals, parents, and seniors seeking muscle maintenance and metabolic health. E-commerce and direct-to-consumer channels have democratized access, with quick-commerce platforms enabling impulse purchases of protein powders and ready-to-drink shakes in tier-2 and tier-3 cities where modern retail penetration remains limited. MuscleBlaze and Optimum Nutrition jointly command approximately 20% of the protein powder market, while plant-based challengers such as Oziva and TrueBasics, whose Clean Whey launch in June 2025 emphasized transparency and purity, are capturing younger, health-conscious consumers. The shift is further amplified by influencer-driven narratives on social media, which frame protein intake as a marker of wellness and social currency, thereby extending adoption beyond traditional fitness enthusiasts.

Protein Fortification of Everyday Staples

Government-led fortification programs are embedding protein into the national food supply, targeting vulnerable populations with inadequate dietary diversity. The Union Cabinet allocated INR 170,820 million (USD 2.04 billion) in 2024 to continue free distribution of fortified rice through the Public Distribution System, Integrated Child Development Services, and mid-day meal schemes, reaching hundreds of millions of beneficiaries. While the primary focus is micronutrient fortification (iron, folic acid, and vitamin B12), the infrastructure and policy momentum create pathways for protein enrichment of staples such as wheat flour, edible oils, and dairy blends. FSSAI's Food Fortification Regulations specify permissible fortificants, labeling requirements, and compositional standards, providing a regulatory framework for manufacturers to introduce protein-fortified atta, biscuits, and ready-to-cook mixes. The World Bank's support for transforming India's Poshan Abhiyaan nutrition program emphasizes scaling evidence-based interventions, including supplementary foods with adequate protein content for pregnant women, lactating mothers, and children under five. This policy-driven demand creates predictable procurement volumes for protein ingredient suppliers and incentivizes innovation in affordable, culturally acceptable formulations that blend plant and animal proteins.

Volatility in Prices and Supply of Key Inputs

Input cost fluctuations for soybean, milk powder, and feed grains create margin pressure and supply uncertainty across the protein value chain. India's soybean production and crushing capacity are concentrated in Gujarat and Madhya Pradesh, where monsoon variability and global commodity price swings drive year-on-year volatility in soymeal availability and pricing. Milk production exhibits seasonal peaks and troughs, with flush periods during winter and lean months in summer, affecting whey and casein by-product volumes and necessitating imports of high-purity isolates for premium applications. Feed grain prices, critical to the poultry, aquaculture, and dairy sectors, are influenced by domestic procurement policies, buffer stock management, and international trade in maize and soybean meal, with any tightening of supply raising livestock production costs and compressing protein output. Processors mitigate risk through forward contracts, vertical integration, and diversification of protein sources, yet smaller players lack hedging capacity and face working capital constraints during price spikes. Exchange rate movements further complicate import-dependent segments, as rupee depreciation raises landed costs for whey protein isolates, specialty plant proteins, and fermentation media components.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Ready-to-Drink Protein Shakes, Bars, and Sachet-Based Formats

- Emerging Use of Precision Fermentation to Produce Animal-Free Dairy Proteins

- Allergenicity Concerns and Consumer Skepticism

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal Protein held a 58.43% market share in 2025, underpinned by India's status as the world's largest milk producer, with annual output supporting robust whey, casein, and milk protein concentrate supply. Whey Protein, the largest animal-derived segment, benefits from vertical integration by dairy processors such as Parag Milk Foods, which invested INR 30,000 million (USD 360 million) to expand production. Egg Protein and Collagen serve niche applications in bakery, confectionery, and clinical nutrition, while Gelatin finds use in pharmaceuticals and functional foods. Insect Protein remains in pilot stages, awaiting FSSAI human consumption approvals despite potential for aquafeed and pet food applications. Microbial Protein is the fastest-growing source, with a 7.95% CAGR through 2031, driven by the commercialization of Algae Protein and Mycoprotein. Perfect Day's Gujarat facility, set to start operations in 2026, will produce recombinant whey via precision fermentation, offering dairy-identical proteins without animal agriculture. Mycoprotein production leverages submerged fermentation of filamentous fungi, delivering high-quality protein with complete amino acid profiles and low saturated fat, suitable for meat analogues and ready-to-eat meals. The Department of Biotechnology's BioE3 plan, approved in January 2025, provides funding, pilot infrastructure, and regulatory facilitation to accelerate microbial protein scale-up.

Plant Protein sources, Soy, Pea, Rice, Wheat, Potato, Hemp, and others, are expanding rapidly, targeting vegetarian consumers, lactose-intolerant individuals, and sustainability-conscious buyers. Soy Protein remains the workhorse of plant-based formulations, with Gujarat and Madhya Pradesh hosting major crushing and processing clusters, yet faces allergenicity concerns and GMO-related consumer hesitancy. Pea Protein is gaining traction in meat analogues, dairy alternatives, and sports nutrition, valued for its neutral flavor profile and non-allergenic status, though earthy off-notes require masking. Rice and Wheat Proteins serve bakery and snack applications, while Potato and Hemp Proteins target premium, clean-label segments. FSSAI's Food Fortification Regulations enable protein enrichment of staples, creating demand for cost-effective plant protein concentrates in atta, biscuits, and ready-to-cook mixes. Cargill's expanded partnership with ENOUGH to scale mycoprotein and biomass fermentation signals multinational commitment to alternative protein platforms adaptable to Indian feedstocks.

Complete Report Scope:

- By Source

- Animal

- Casein and Caseinates

- Collagen

- Egg Protein

- Gelatin

- Insect Protein

- Milk Protein

- Whey Protein

- Other Animal Proteins

- Microbial

- Algae Protein

- Mycoprotein

- Plant

- Hemp Protein

- Pea Protein

- Potato Protein

- Rice Protein

- Soy Protein

- Wheat Protein

- Other Plant Proteins

- Animal

- By Form

- Concentrates

- Isolates

- Hydrolysates

- Other Forms

- By Application

- Food and Beverages

- Bakery

- Beverages

- Breakfast Cereals

- Condiments/Sauces

- Confectionery

- Dairy and Dairy Alternative Products

- Meat/Poultry/Seafood and Meat Alternative Products

- RTE/RTC Food Products

- Snacks

- Infant Nutrition

- Other Food and Beverage Applications

- Personal Care and Cosmetics

- Animal Feed

- Dietary Supplements and Sports Nutrition

- Food and Beverages

List of Companies Covered in this Report:

- Archer Daniels Midland Company (ADM)

- Fonterra Co-operative Group Ltd

- Glanbia plc

- Hilmar Cheese Company Inc.

- International Flavors & Fragrances Inc. (IFF)

- Kerry Group plc

- Nakoda Dairy Pvt Ltd

- Nitta Gelatin Inc.

- Roquette Freres

- Sudzucker AG (BENEO)

- VIPPY Industries Ltd

- Cargill Incorporated

- DSM-Firmenich AG

- Gujarat Ambuja Exports Ltd

- Shree Panchvati Soy Industries

- Hexagon Nutrition Ltd

- Axiom Foods Inc.

- Novozymes A/S

- Devansoy Inc.

- AMCO Proteins

- Ingredion Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing mainstream adoption of high-protein diets and sports nutrition

- 4.2.2 Protein fortification of everyday staples

- 4.2.3 Expansion of ready-to-drink protein shakes, bars, and sachet-based formats

- 4.2.4 Emerging use of precision fermentation to produce animal-free dairy proteins

- 4.2.5 Rising demand for premium pet food and aquafeed

- 4.2.6 Strong digital-led marketing and influencer-driven health-and-wellness narratives

- 4.3 Market Restraints

- 4.3.1 Volatility in prices and supply of key inputs

- 4.3.2 Allergenicity concerns and consumer skepticism

- 4.3.3 Regulatory approvals slowing insect/microbial protein adoption

- 4.3.4 Flavor off-notes/processing challenges driving higher costs

- 4.4 Technological Outlook

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Source

- 5.1.1 Animal

- 5.1.1.1 Casein and Caseinates

- 5.1.1.2 Collagen

- 5.1.1.3 Egg Protein

- 5.1.1.4 Gelatin

- 5.1.1.5 Insect Protein

- 5.1.1.6 Milk Protein

- 5.1.1.7 Whey Protein

- 5.1.1.8 Other Animal Proteins

- 5.1.2 Microbial

- 5.1.2.1 Algae Protein

- 5.1.2.2 Mycoprotein

- 5.1.3 Plant

- 5.1.3.1 Hemp Protein

- 5.1.3.2 Pea Protein

- 5.1.3.3 Potato Protein

- 5.1.3.4 Rice Protein

- 5.1.3.5 Soy Protein

- 5.1.3.6 Wheat Protein

- 5.1.3.7 Other Plant Proteins

- 5.1.1 Animal

- 5.2 By Form

- 5.2.1 Concentrates

- 5.2.2 Isolates

- 5.2.3 Hydrolysates

- 5.2.4 Other Forms

- 5.3 By Application

- 5.3.1 Food and Beverages

- 5.3.1.1 Bakery

- 5.3.1.2 Beverages

- 5.3.1.3 Breakfast Cereals

- 5.3.1.4 Condiments/Sauces

- 5.3.1.5 Confectionery

- 5.3.1.6 Dairy and Dairy Alternative Products

- 5.3.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 5.3.1.8 RTE/RTC Food Products

- 5.3.1.9 Snacks

- 5.3.1.10 Infant Nutrition

- 5.3.1.11 Other Food and Beverage Applications

- 5.3.2 Personal Care and Cosmetics

- 5.3.3 Animal Feed

- 5.3.4 Dietary Supplements and Sports Nutrition

- 5.3.1 Food and Beverages

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Archer Daniels Midland Company (ADM)

- 6.4.2 Fonterra Co-operative Group Ltd

- 6.4.3 Glanbia plc

- 6.4.4 Hilmar Cheese Company Inc.

- 6.4.5 International Flavors & Fragrances Inc. (IFF)

- 6.4.6 Kerry Group plc

- 6.4.7 Nakoda Dairy Pvt Ltd

- 6.4.8 Nitta Gelatin Inc.

- 6.4.9 Roquette Freres

- 6.4.10 Sudzucker AG (BENEO)

- 6.4.11 VIPPY Industries Ltd

- 6.4.12 Cargill Incorporated

- 6.4.13 DSM-Firmenich AG

- 6.4.14 Gujarat Ambuja Exports Ltd

- 6.4.15 Shree Panchvati Soy Industries

- 6.4.16 Hexagon Nutrition Ltd

- 6.4.17 Axiom Foods Inc.

- 6.4.18 Novozymes A/S

- 6.4.19 Devansoy Inc.

- 6.4.20 AMCO Proteins

- 6.4.21 Ingredion Incorporated

7 MARKET OPPORTUNITIES AND FUTURE TRENDS