PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073572

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073572

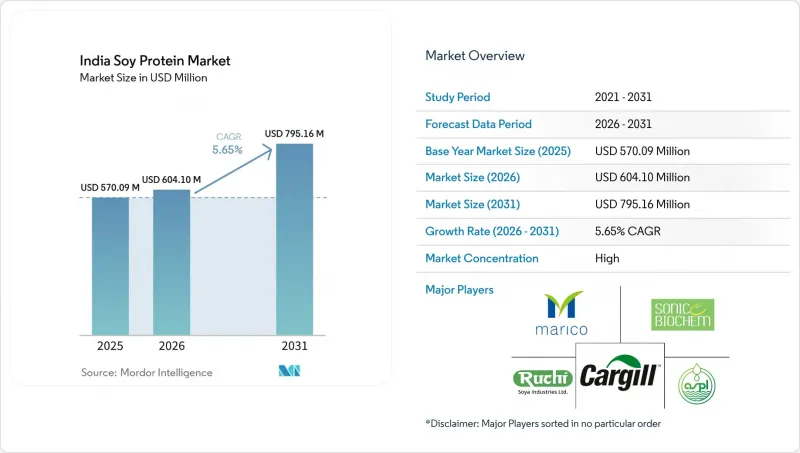

India Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india soy protein market size was valued at USD 570.09 million in 2025 and expected to grow from USD 604.10 million in 2026 to reach USD 795.16 million by 2031, at a CAGR of 5.65% during the forecast period (2026-2031).

This report is Segmented by Form (Soy Protein Concentrates, Soy Protein Hydrolyzed, Soy Protein Isolates), Category (Organic, Conventional), End User (Animal Feed, Food and Beverages, Nutritional Supplements), and Geography (India). The Market Forecasts are Provided in Terms of Value (USD Million) and Volume (Tons).

India Soy Protein Market Trends and Insights

Growing Vegetarian, Vegan, and Flexitarian Diets Drive Soy Protein

India's protein consumption landscape reveals a structural deficit: 73% of the population falls short of daily protein requirements, with vegetarians showing 91% deficiency and non-vegetarians 85%, according to data released by Country Delight in August 2025. This gap creates latent demand for affordable plant-based proteins, where soy isolates and concentrates offer cost advantages over dairy and meat. The Ministry of Statistics and Programme Implementation's Nutritional Intake in India report (June 2025) quantifies per-capita protein intake by state and identifies regions with the highest cereal-dominant diets as priority markets for soy-fortified staples. Urban consumers are shifting toward flexitarian diets not solely for ethical reasons but due to rising meat prices and health awareness campaigns linking plant proteins to cardiovascular benefits. Tata Consumer Products entered the plant protein powder segment in September 2022 with Tata GoFit, leveraging brand equity to capture health-conscious consumers. Akshayakalpa Organic announced a protein-focused strategy, targeting Rs 550 crore (USD 66 million) in revenue in fiscal 2025, signaling a pivot by FMCG players toward protein portfolios.

Rising Demand for Plant-Based Protein-Fortified Snacks, Beverages, and Ready-to-Drink Products

The convergence of convenience, nutrition, and clean-label demands is reshaping product development cycles in packaged foods. Country Delight launched a high-protein cow's milk in August 2025, delivering 30 grams of protein per 450 ml serving, positioning it as a meal replacement and addressing the 90% of urban consumers unaware of the recommended daily protein intake. While dairy-based, this innovation signals broader acceptance of protein fortification across beverage categories, creating adjacency opportunities for soy protein isolates in plant-based RTD shakes and protein waters. Patanjali Foods' Food & FMCG segment, which explicitly includes textured soy protein, grew revenue 57% year-on-year to Rs 6,938.71 crore (USD 829 million) in the nine months ending December 2023, with biscuits alone contributing Rs 1,225.72 crore (USD 146 million), suggesting soy protein's integration into mass-market snack formulations according to Patanjali Foods Limited. The Production Linked Incentive scheme for food processing, announced in December 2024, incentivizes capacity expansion and technology upgradation for processed food manufacturers, lowering barriers to soy protein adoption in snack extrusion and beverage fortification, according to the Press Information Bureau. FSSAI's labeling regulations mandate allergen declaration for soy and compositional thresholds for protein claims, ensuring transparency but also raising compliance costs for smaller players.

Soybean Price Volatility

Raw material cost instability is the most immediate threat to processor margins and downstream pricing competitiveness. Soybean production for the marketing year 2025/26 fell to 10.7 million metric tons, down 12% from initial forecasts of 12.1 million metric tons, due to untimely rainfall, re-sowing delays, and farmer shifts to rice, sugarcane, and corn, according to the FAS New Delhi (USDA). The government raised minimum support prices 9% to Rs 5,328 per quintal (USD 62.6 per quintal) in May 2025, yet market-yard prices in July-August 2025 hovered at Rs 5,500-5,600 per quintal, expected to climb toward Rs 5,900-6,000 per quintal as lower production tightens supplies. Crushers face a double squeeze: higher input costs and reduced import duty on crude edible oils (effective 16.5% from 27.5% per the May 30, 2025, notification), which increases the competitiveness of imported soybean oil and depresses domestic crush incentives. Soymeal ending stocks for 2025/26 are forecast at 455,000 metric tons, a 52% reduction from prior levels, which will constrain availability for food-grade protein extraction. Weather variability and limited irrigation in rainfed soybean belts of Madhya Pradesh and Maharashtra amplify year-to-year production swings, preventing processors from securing long-term fixed-price contracts with food manufacturers. The National Mission on Edible Oils aims to stabilize supply through higher yields and expanded acreage, but its impact will materialize only over the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Soy-Based Proteins in Indian Pet Food and Aquafeed

- Growth of Sports Nutrition and High-Protein Supplements

- High Processing and Isolation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soy protein isolates captured 49.43% of the market share in 2025, reflecting their dominance in applications that demand high protein purity, neutral flavor, and superior emulsification properties, such as meat analogues, protein bars, and clinical nutrition formulas. Textured and hydrolyzed soy proteins, while holding smaller shares, are expanding at a 5.95% CAGR through 2031, driven by ready-to-eat snacks, extruded meat substitutes, and convenience foods where texture and chewiness are critical. Soy protein concentrates occupy the middle ground, offering 70% protein content at a lower cost than isolates, and find use in bakery, dairy analogues, and animal feed where extreme purity is unnecessary. The shift toward textured forms is evident in Patanjali Foods' Food & FMCG segment, which explicitly includes textured soy protein and grew 64% year-on-year in Q3FY24, with biscuits and snacks contributing significant volumes to market share in 2025, reflecting their dominance in applications that demand them.

Processing technology differentiates from performance: isolates require aqueous extraction and spray drying, concentrates use alcohol washing or acid leaching, and textured variants employ extrusion cooking under high temperature and pressure. Anand Agro's extruder-based plant, producing 220 metric tons per day of soya meal with 47-48% protein and 6% fat, demonstrates the technical capability to produce higher-fat, higher-energy extruded products suitable for feed and food applications. Hydrolyzed soy proteins, produced via enzymatic or acid hydrolysis, offer improved solubility and reduced allergenicity, positioning them for infant formula and medical nutrition, though regulatory scrutiny around allergen labeling under FSSAI rules remains stringent. The Production Linked Incentive scheme's support for technology upgradation is expected to accelerate adoption of advanced extrusion and isolation equipment, narrowing the cost gap between domestic and imported soy protein forms.

Complete Report Scope:

- By Form

- Soy Protein Concentrates

- Soy Protein Hydrolyzed

- Soy Protein Isolates

- By Category

- Organic

- Conventional

- By End User

- Animal Feed

- Food and Beverages

- Bakery

- Beverages

- Breakfast Cereals

- Condiments/Sauces

- Confectionery

- Dairy and Dairy Alternatives

- Meat/Poultry/Seafood and Meat Alternative Products

- RTE/RTC Foods

- Snacks

- Nutritional Supplements

- Baby and Infant Formula

- Elderly and Medical Nutrition

- Sport/Performance Nutrition

List of Companies Covered in this Report:

- Ruchi Soya Industries Ltd (Patanjali Foods)

- Sonic Biochem Extractions Pvt Ltd

- Agro Solvent Products Pvt Ltd

- Vippy Industries Limited

- Rejoice Life Ingredients

- Soy Protein Ltd

- Cargill India

- Bunge India

- Wilmar International

- Shandong Yuwang Group

- CHS Inc.

- Devansoy Inc.

- Tata Consumer Products

- Marico Ltd

- GoodDot

- Blue Tribe Foods

- AS-IT-IS Nutrition

- International Flavors & Fragrances Inc.

- Kerry Group plc

- Archer Daniels Midland Company (ADM)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing vegetarian, vegan, and flexitarian diets drive soy protein

- 4.2.2 Rising demand for plant-based protein-fortified snacks, beverages, and ready-to-drink products

- 4.2.3 Adoption of soy-based proteins in Indian pet food and aquafeed

- 4.2.4 Growth of sports nutrition and high-protein supplements

- 4.2.5 Government and industry initiatives to promote plant-based proteins

- 4.2.6 Use of soy protein in infant formulas, weaning foods, and dairy-free milks

- 4.3 Market Restraints

- 4.3.1 Soybean price volatility

- 4.3.2 High processing and isolation costs

- 4.3.3 Stringent FSSAI and regulatory scrutiny around soy safety, labeling, and health claims

- 4.3.4 Limited domestic soybean processing capacity

- 4.4 Supply Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Form

- 5.1.1 Soy Protein Concentrates

- 5.1.2 Soy Protein Hydrolyzed

- 5.1.3 Soy Protein Isolates

- 5.2 By Category

- 5.2.1 Organic

- 5.2.2 Conventional

- 5.3 By End User

- 5.3.1 Animal Feed

- 5.3.2 Food and Beverages

- 5.3.2.1 Bakery

- 5.3.2.2 Beverages

- 5.3.2.3 Breakfast Cereals

- 5.3.2.4 Condiments/Sauces

- 5.3.2.5 Confectionery

- 5.3.2.6 Dairy and Dairy Alternatives

- 5.3.2.7 Meat/Poultry/Seafood and Meat Alternative Products

- 5.3.2.8 RTE/RTC Foods

- 5.3.2.9 Snacks

- 5.3.3 Nutritional Supplements

- 5.3.3.1 Baby and Infant Formula

- 5.3.3.2 Elderly and Medical Nutrition

- 5.3.3.3 Sport/Performance Nutrition

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ruchi Soya Industries Ltd (Patanjali Foods)

- 6.4.2 Sonic Biochem Extractions Pvt Ltd

- 6.4.3 Agro Solvent Products Pvt Ltd

- 6.4.4 Vippy Industries Limited

- 6.4.5 Rejoice Life Ingredients

- 6.4.6 Soy Protein Ltd

- 6.4.7 Cargill India

- 6.4.8 Bunge India

- 6.4.9 Wilmar International

- 6.4.10 Shandong Yuwang Group

- 6.4.11 CHS Inc.

- 6.4.12 Devansoy Inc.

- 6.4.13 Tata Consumer Products

- 6.4.14 Marico Ltd

- 6.4.15 GoodDot

- 6.4.16 Blue Tribe Foods

- 6.4.17 AS-IT-IS Nutrition

- 6.4.18 International Flavors & Fragrances Inc.

- 6.4.19 Kerry Group plc

- 6.4.20 Archer Daniels Midland Company (ADM)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS