PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073573

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073573

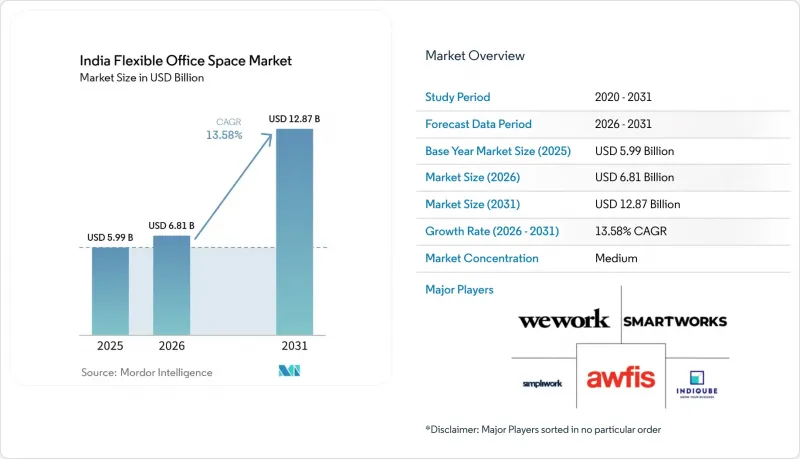

India Flexible Office Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, india flexible office space market size in 2026 is estimated at USD 6.81 billion, growing from 2025 value of USD 5.99 billion with 2031 projections showing USD 12.87 billion, growing at 13.58% CAGR over 2026-2031.

This report is Segmented by Type (Co-Working Spaces, Serviced Offices / Executive Suites, and More) by Sector (Information Technology (IT & ITES), and More), by End Use (Enterprises, Freelancers and Start Ups & Others), and by City (Mumbai Metropolitan Region, Bengaluru, Pune and More). The Report Provides Market Size and Forecasts in Value (USD) for all the Above Segments.

India Flexible Office Space Market Trends and Insights

Post-COVID Hybrid Work Models Drive Enterprise Flexibility Demand

The shift to hybrid work models post-COVID-19 has significantly transformed workspace strategies for Indian corporates. Indian corporates are increasingly viewing flexible workspaces as essential infrastructure rather than mere contingency options. The demands of hybrid work schedules necessitate on-the-fly seat allocations, a feat that traditional leases struggle to provide. Companies are turning to plug-and-play centers, armed with occupancy-management software, allowing them to slash real estate costs by up to 30% per desk, all while enjoying top-tier amenities. Once bound by nine-year leases, multinationals are now favoring one- to three-year managed-office contracts, shifting operational risks to the providers but ensuring scalability. What began as experimental projects in Mumbai and Bengaluru has now expanded to encompass full portfolios in five or more cities. As head-office spaces become predominantly reserved for branding and client interactions, these flexible hubs are not only managing daily operations but also playing a pivotal role in talent retention amidst a competitive labor market.

Startup Ecosystem Expansion Fuels On-Demand Workspace Growth

India's start-up ecosystem continues to thrive, with Haryana alone witnessing the registration of over 700 new start-ups in 2024, underscoring nationwide entrepreneurial momentum. These firms prize operational-expenditure models over capex-heavy leases and migrate to flex space that scales in weekly or monthly blocks. Venture funding rounds often translate into sudden head-count jumps; coworking contracts provide rapid seat additions without lease renegotiation. Operators, therefore, design variable seat packs, dynamic pricing, and investor lounge zones aligned with start-up cultures. As start-ups move from seed to Series B, they tend to graduate into managed offices within the same campus, giving operators built-in customer life-cycle growth.

Rental Cost Inflation Pressures Operator Profitability

Rising rental costs are increasingly challenging the profitability of flex-space operators in prime locations. In South Mumbai, Grade-A office rents have crossed the USD 2.40 per sq ft per month mark, putting a pinch on flex-operator margins, even with optimised seat density. While annual step-up clauses in master leases can hit 6%, operators frequently limit client escalations to 4%, leading to a negative spread. Since 2023, maintenance costs-covering power, cleaning, and internet-have surged by 8-10%, further constraining operating profits. To counteract these pressures, operators are pivoting to revenue-share models and seeking longer lock-ins for bulk discounts. However, the risk to margins remains significant, especially in prime CBD areas.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Metro Expansion by Brands Enhances Tier-2 Market Penetration

- Corporate Suburban and Satellite Hubs Support Distributed Teams

- Oversupply Conditions Threaten Pricing Power

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Co-working spaces accounted for 47.92% India flexible office market share in 2025, underscoring enduring demand for open, collaborative environments that suit agile teams. Meanwhile, the Hybrid & Virtual Office category is forecast to post a 14.35% CAGR, the fastest among formats, as corporates look to blend private managed suites with day-pass access for distributed staff. Within the India flexible office market size, hybrid products bundle physical seats, virtual addresses, and on-demand meeting rooms, giving tenants modular cost control. Awfis, Smartworks, and Table Space now allocate more than 35% of new supply to hybrid layouts.

Technology is the linchpin: mobile apps let employees reserve desks in 15-minute increments, while AI-driven utilisation dashboards inform real-time space reconfiguration. Operators invest in acoustic zoning and air-quality monitoring to meet ESG and employee-wellbeing metrics. As large enterprises pivot to hub-and-spoke networks, hybrid centres capable of toggling between open and enclosed zones gain strategic relevance, reinforcing the India flexible office market's gradual tilt toward multi-format service lines.

Complete Report Scope:

- By Type

- Co-Working Space

- Serviced offices / Executive suites

- Others (Hybrid, Virtual Office)

- By Sector

- Information Technology (IT and ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Service

- Other Services (Retail, Lifesciences, Energy, Legal Services)

- By End Use

- Freelancers

- Enterprises

- Start Ups and Others

- By City

- Mumbai Metropolitan Region

- Delhi NCR

- Pune

- Bengaluru

- Hyderabad

- Chennai

- Kolkata

- Rest of India

List of Companies Covered in this Report:

- WeWork

- Awfis Space Solutions

- Smartworks

- IndiQube

- Simpliwork Offices

- CoWrks

- 91Springboard

- The Hive

- BHIVE Workspace

- Skootr

- Table Space

- Regus (IWG plc)

- 315Work Avenue

- Urban Vault

- MyHQ

- WorkEz

- GoodWorks Coworking

- OYO Workspaces (PowerStation + Innov8)

- Incuspaze

- Bangalore Alpha Lab

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-COVID hybrid work models are driving enterprises to adopt flexible plug-and-play office solutions.

- 4.2.2 A boom in startups and SMEs is increasing demand for on-demand, scalable coworking spaces.

- 4.2.3 Rapid metro expansion by coworking brands like WeWork, Awfis, and Smartworks in Tier-1/2 cities is enhancing accessibility.

- 4.2.4 Corporates are launching suburban and satellite flex hubs to support geographically distributed teams.

- 4.2.5 Integration of digital amenities (e.g., app-based bookings, smart conference rooms) is improving occupier experience.

- 4.2.6 LEED or IGBC-certified flex spaces are attracting clients with ESG mandates and commanding premium prices.

- 4.3 Market Restraints

- 4.3.1 High rental escalation and maintenance costs in Mumbai, Delhi NCR, and Bangalore are compressing operator margins.

- 4.3.2 Emerging oversupply in major metros is increasing vacancy risk and pressuring renewal rates.

- 4.3.3 Diverse state-level lease and commercial regulations are complicating multi-city rollouts.

- 4.3.4 Security and data privacy concerns in shared networks are limiting corporate adoption.

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers and Asset Owners - Key Quantitative and Qualitative Insights

- 4.4.3 Workspace Design and Technology Consultants - Key Quantitative and Qualitative Insights

- 4.4.4 Modular Furniture and Smart Office Solutions Providers - Key Quantitative and Qualitative Insights

- 4.5 Government Regulations and Initiatives in the Industry

- 4.6 Technological Innovations in the Flexible Office Real Estate Market

- 4.7 Insights into the Key Office Real Estate Industry Metrics (Supply, Rentals, Prices, Occupancy/Vacancy (%))

- 4.8 Impact of Remote Working on Space Demand

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Type

- 5.1.1 Co-Working Space

- 5.1.2 Serviced offices / Executive suites

- 5.1.3 Others (Hybrid, Virtual Office)

- 5.2 By Sector

- 5.2.1 Information Technology (IT and ITES)

- 5.2.2 BFSI (Banking, Financial Services and Insurance)

- 5.2.3 Business Consulting & Professional Service

- 5.2.4 Other Services (Retail, Lifesciences, Energy, Legal Services)

- 5.3 By End Use

- 5.3.1 Freelancers

- 5.3.2 Enterprises

- 5.3.3 Start Ups and Others

- 5.4 By City

- 5.4.1 Mumbai Metropolitan Region

- 5.4.2 Delhi NCR

- 5.4.3 Pune

- 5.4.4 Bengaluru

- 5.4.5 Hyderabad

- 5.4.6 Chennai

- 5.4.7 Kolkata

- 5.4.8 Rest of India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 WeWork

- 6.3.2 Awfis Space Solutions

- 6.3.3 Smartworks

- 6.3.4 IndiQube

- 6.3.5 Simpliwork Offices

- 6.3.6 CoWrks

- 6.3.7 91Springboard

- 6.3.8 The Hive

- 6.3.9 BHIVE Workspace

- 6.3.10 Skootr

- 6.3.11 Table Space

- 6.3.12 Regus (IWG plc)

- 6.3.13 315Work Avenue

- 6.3.14 Urban Vault

- 6.3.15 MyHQ

- 6.3.16 WorkEz

- 6.3.17 GoodWorks Coworking

- 6.3.18 OYO Workspaces (PowerStation + Innov8)

- 6.3.19 Incuspaze

- 6.3.20 Bangalore Alpha Lab

7 Market Opportunities & Future Outlook