PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073587

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073587

Semiconductor Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

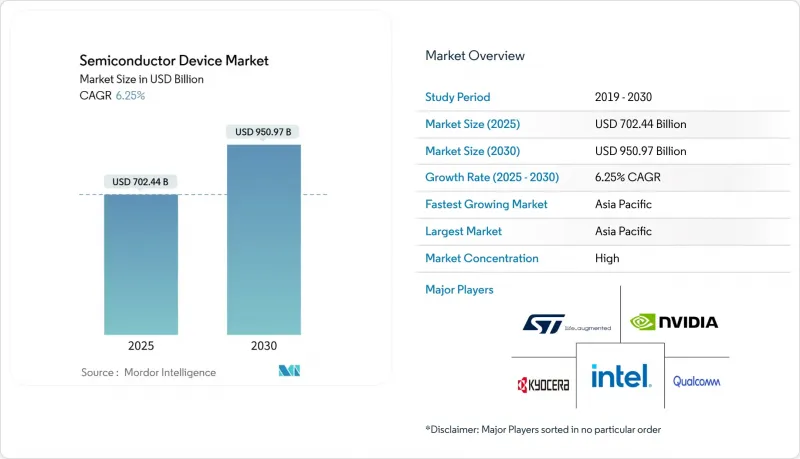

According to Mordor Intelligence, the semiconductor device market size reached USD 702.44 billion in 2025 and is forecast to attain USD 950.97 billion by 2030, translating into a 6.25% CAGR over the period.

This report is Segmented by Device Type (Discrete Semiconductors [Diodes, and More], Optoelectronics, Sensors and MEMS, and Integrated Circuits), Business Model (IDM, and Design/ Fabless Vendor), End-Use Industry (Automotive, Communication, Consumer, Industrial, Computing/Data Storage, Data Center, AI, and Government), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Semiconductor Device Market Trends and Insights

AI accelerator demand in hyperscale data centers

Hyperscale operators in the United States and China are retrofitting server halls to support accelerator cards that draw over 1 kW each, prompting capital-expenditure plans topping USD 1 trillion by 2029. The shift requires custom silicon with high-bandwidth memory and advanced packaging, pushing foundry utilization above 90% at leading-edge nodes. The resulting backlog underlines why the semiconductor market continues to outpace earlier forecasts. Scarcity of advanced substrates and thermal-management materials further amplifies pricing power for suppliers.

EV power-electronics content per vehicle surging.

Transition from internal-combustion to electric drivetrains lifts silicon content from roughly USD 600 to more than USD 2,000 per car. Silicon-carbide MOSFETs raise inverter efficiency by up to 3 percentage points, directly extending driving range. European automakers spearhead 800-V architectures, accelerating demand for wide-bandgap devices. The semiconductor market benefits from parallel growth in charging infrastructure that employs the same power modules.

Lithography tool lead times> 18 months

High-NA extreme-ultraviolet steppers priced near USD 380 million each face production bottlenecks, with deliveries stretching beyond 18 months. Limited tool availability caps capacity additions even as demand for 3 nm-and-below processes climbs. Early tool recipients obtain temporary pricing leverage, while laggards risk design wins migrating to competitors. Prolonged supply gaps temper the semiconductor market's otherwise strong growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- ADAS semiconductor penetration in next-gen vehicles

- Industrial edge-IoT sensor proliferation

- Export-control curbs on advanced nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated circuits captured 86.1% of the semiconductor market in 2024 and are projected to advance at a 7.9% CAGR through 2030. Logic and analog sub-segments gain from AI inference engines, vehicle-electrification control, and industrial automation rollouts. High-bandwidth memory and 3-D NAND remain cornerstones of AI accelerator performance, reinforcing premium pricing. Discrete power devices, optoelectronics, and sensors, though smaller in dollar terms, enable system-level functionality vital for EV inverters and optical-communication modules. Silicon-carbide MOSFETs and gallium-nitride HEMTs post double-digit volume gains, reflecting drivetrain voltage escalation trends. MEMS inertial and environmental sensors proliferate in Industry 4.0 projects, ensuring balanced growth across device classes. These trends collectively position integrated circuits at the forefront of the semiconductor market size expansion while permitting specialized components to capture emerging niches.

Complete Report Scope:

- By Device Type (Shipment Volume for Device Type is Complementary)

- Discrete Semiconductors

- Diodes

- Transistors

- Power Transistors

- Rectifier and Thyristor

- Other Discrete Devices

- Optoelectronics

- Light-Emitting Diodes (LEDs)

- Laser Diodes

- Image Sensors

- Optocouplers

- Other Device Types

- Sensors and MEMS

- Pressure

- Magnetic Field

- Actuators

- Acceleration and Yaw Rate

- Temperature and Others

- Integrated Circuits

- By Integrated Circuit Type

- Analog

- Micro

- Microprocessors (MPU)

- Microcontrollers (MCU)

- Digital Signal Processors

- Logic

- Memory

- By Technology Node (Shipment Volume Not Applicable)

- < 3nm

- 3nm

- 5nm

- 7nm

- 16nm

- 28nm

- > 28nm

- By Integrated Circuit Type

- Discrete Semiconductors

- By Business Model

- IDM

- Design/ Fabless Vendor

- By End-user Industry

- Automotive

- Communication (Wired and Wireless)

- Consumer

- Industrial

- Computing/Data Storage

- Data Center

- AI

- Government (Aerospace and Defense)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Mexico

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- Taiwan

- South Korea

- Japan

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific commanded 63.2% of global revenue in 2024 and is forecast to grow at a 7.1% CAGR to 2030, anchored by Taiwan's advanced-node leadership and South Korea's USD 471 billion megacluster build-out. Mainland China, while constrained at leading nodes, invests heavily in mature-process parks and domestic equipment suppliers, aiming to lift local content ratios. Japan channels ¥3.9 trillion (USD 26.1 billion) into joint ventures that couple domestic materials prowess with external foundry expertise, while India accelerates assembly-test and design-services growth.

North America ranks second by value, catalyzed by USD 52 billion CHIPS Act incentives that underwrite new fabs in Arizona, Ohio, and Texas. Intel secured USD 7.865 billion, TSMC USD 6.6 billion, and Samsung USD 4.745 billion for U.S. expansions. The region houses a dense cluster of fabless AI and networking chip designers, translating into sustained demand for advanced wafers. Automotive electrification programs in Michigan and California further diversify revenue streams, ensuring the semiconductor market remains robust even amid cyclical consumer-electronics swings. Section 5949 of the 2023 NDAA will phase in procurement restrictions in 2027, nudging supply chains toward domestic nodes for defense-linked workloads.

Europe, holding under 10% share, nonetheless influences technology direction through stringent automotive and environmental regulations that shape chip specifications worldwide. The EU Chips Act targets a 20% production share by 2030 via incentive pools for Dresden and Eindhoven projects focusing on power electronics and specialty analog. Germany anchors premium vehicle semiconductor demand, while Nordic grids adopt wide-bandgap devices for renewables. Collaborative R&D alliances leverage university-industry ties, positioning the continent as a competence center for reliability and safety certification-attributes prized across the semiconductor market.

- Intel Corporation

- Taiwan Semiconductor Manufacturing Co. Ltd. (TSMC)

- Samsung Electronics Co. Ltd.

- Nvidia Corporation

- Qualcomm Incorporated

- Texas Instruments Inc.

- SK Hynix Inc.

- Micron Technology Inc.

- Broadcom Inc.

- Advanced Micro Devices Inc. (AMD)

- Analog Devices Inc.

- NXP Semiconductors NV

- Infineon Technologies AG

- STMicroelectronics NV

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Wolfspeed Inc.

- GlobalFoundries Inc.

- United Microelectronics Corp. (UMC)

- ASE Technology Holding Co. Ltd.

- ROHM Co. Ltd.

- Kyocera Corp.

- Toshiba Corp.

- Fujitsu Semiconductor Ltd.

- Marvell Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI Accelerator Demand in Hyperscale Data Centers (US and China)

- 4.2.2 EV Power-Electronics Content per Vehicle Surging

- 4.2.3 ADAS Semiconductor Penetration in Next-Gen Vehicles

- 4.2.4 Industrial Edge-IoT Sensor Proliferation (Europe)

- 4.2.5 5G RF-Front-End Complexity (Korea and China)

- 4.2.6 US/EU CHIPS-Act Fab Incentives

- 4.3 Market Restraints

- 4.3.1 Lithography Tool Lead-Times >18 Months

- 4.3.2 Export-Control Curbs on Advanced Nodes (China)

- 4.3.3 High Fab Capex and Energy Intensity

- 4.3.4 Engineering-Talent Shortage

- 4.4 Technological Trends

- 4.5 Industry Value Chain Analysis

- 4.6 Semiconductor Foundry Landscape

- 4.6.1 Foundry Revenue and Share by Player

- 4.6.2 IDM vs Fabless Semiconductor Sales

- 4.6.3 Installed Wafer Capacity by Fab Location

- 4.6.4 Wafer Capacity by Company and Node Technology

- 4.7 Regulatory and Trade-Policy Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

- 4.10 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type (Shipment Volume for Device Type is Complementary)

- 5.1.1 Discrete Semiconductors

- 5.1.1.1 Diodes

- 5.1.1.2 Transistors

- 5.1.1.3 Power Transistors

- 5.1.1.4 Rectifier and Thyristor

- 5.1.1.5 Other Discrete Devices

- 5.1.2 Optoelectronics

- 5.1.2.1 Light-Emitting Diodes (LEDs)

- 5.1.2.2 Laser Diodes

- 5.1.2.3 Image Sensors

- 5.1.2.4 Optocouplers

- 5.1.2.5 Other Device Types

- 5.1.3 Sensors and MEMS

- 5.1.3.1 Pressure

- 5.1.3.2 Magnetic Field

- 5.1.3.3 Actuators

- 5.1.3.4 Acceleration and Yaw Rate

- 5.1.3.5 Temperature and Others

- 5.1.4 Integrated Circuits

- 5.1.4.1 By Integrated Circuit Type

- 5.1.4.1.1 Analog

- 5.1.4.1.2 Micro

- 5.1.4.1.2.1 Microprocessors (MPU)

- 5.1.4.1.2.2 Microcontrollers (MCU)

- 5.1.4.1.2.3 Digital Signal Processors

- 5.1.4.1.3 Logic

- 5.1.4.1.4 Memory

- 5.1.4.2 By Technology Node (Shipment Volume Not Applicable)

- 5.1.4.2.1 < 3nm

- 5.1.4.2.2 3nm

- 5.1.4.2.3 5nm

- 5.1.4.2.4 7nm

- 5.1.4.2.5 16nm

- 5.1.4.2.6 28nm

- 5.1.4.2.7 > 28nm

- 5.1.4.1 By Integrated Circuit Type

- 5.1.1 Discrete Semiconductors

- 5.2 By Business Model

- 5.2.1 IDM

- 5.2.2 Design/ Fabless Vendor

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Communication (Wired and Wireless)

- 5.3.3 Consumer

- 5.3.4 Industrial

- 5.3.5 Computing/Data Storage

- 5.3.6 Data Center

- 5.3.7 AI

- 5.3.8 Government (Aerospace and Defense)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Mexico

- 5.4.2.3 Argentina

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Nordics

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Taiwan

- 5.4.4.3 South Korea

- 5.4.4.4 Japan

- 5.4.4.5 India

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Taiwan Semiconductor Manufacturing Co. Ltd. (TSMC)

- 6.4.3 Samsung Electronics Co. Ltd.

- 6.4.4 Nvidia Corporation

- 6.4.5 Qualcomm Incorporated

- 6.4.6 Texas Instruments Inc.

- 6.4.7 SK Hynix Inc.

- 6.4.8 Micron Technology Inc.

- 6.4.9 Broadcom Inc.

- 6.4.10 Advanced Micro Devices Inc. (AMD)

- 6.4.11 Analog Devices Inc.

- 6.4.12 NXP Semiconductors NV

- 6.4.13 Infineon Technologies AG

- 6.4.14 STMicroelectronics NV

- 6.4.15 ON Semiconductor Corp.

- 6.4.16 Renesas Electronics Corp.

- 6.4.17 Wolfspeed Inc.

- 6.4.18 GlobalFoundries Inc.

- 6.4.19 United Microelectronics Corp. (UMC)

- 6.4.20 ASE Technology Holding Co. Ltd.

- 6.4.21 ROHM Co. Ltd.

- 6.4.22 Kyocera Corp.

- 6.4.23 Toshiba Corp.

- 6.4.24 Fujitsu Semiconductor Ltd.

- 6.4.25 Marvell Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment