PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073603

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073603

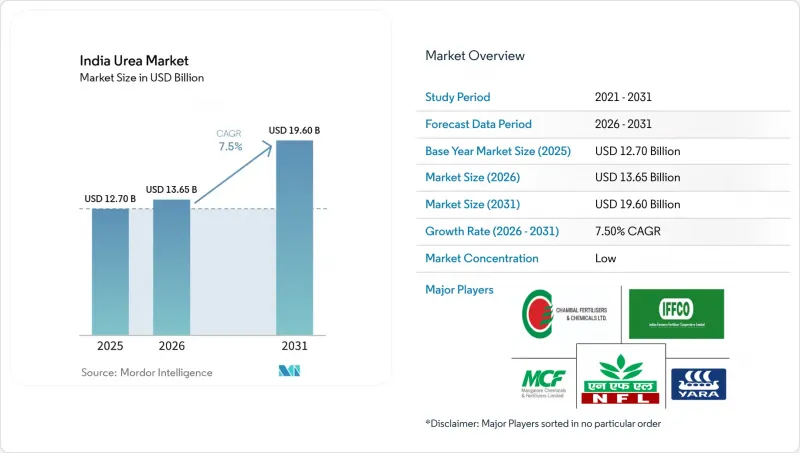

India Urea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india urea market size was valued at USD 12.70 billion in 2025 and estimated to grow from USD 13.65 billion in 2026 to reach USD 19.60 billion by 2031, at a CAGR of 7.50% during the forecast period (2026-2031).

This report is Segmented by Specialty Type (Controlled-Release Fertilizers, Slow-Release Fertilizers, Liquid Fertilizers, and Water-Soluble Fertilizers), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Form (Conventional and Specialty). The Market Forecasts are Provided in Terms of Value (USD) and Volume (metric Tons).

India Urea Market Trends and Insights

Nitrogen stands out as the most widely used nutrient in field crop cultivation

Nitrogen, with an average application rate of 223.5 kg/ha, stands out as the most widely utilized nutrient. As a primary nutrient, nitrogen is crucial for high-yield crops, notably rice, which dominates India's agricultural landscape. Yet, a nationwide struggle with nitrogen deficiencies is undermining rice productivity. Concerns about India's soil health are underscored in the "State of Biofertilizers and Organic Fertilizers" report. It highlights an alarming trend: a heavy dependence on chemical fertilizers, with 97.0%, 83.0%, and 71.0% of tested soils exhibiting deficiencies in nitrogen, phosphorus, and potassium, respectively. Wheat and rice, staples on both domestic and global tables, grapple with challenges stemming from multiple nutrient deficiencies. Grains and cereals, as field crops, have an insatiable demand for primary nutrients, especially nitrogen fertilizers. With these crops being extensively cultivated across India, the depletion of the soil's nutrient content is becoming increasingly pronounced.

Adoption of Micro-Irrigation Systems Boosting Water-Soluble Demand

Micro-irrigation coverage expansion under the Pradhan Mantri Krishi Sinchayee Yojana has created a structural demand shift toward water-soluble fertilizers, with drip and sprinkler systems requiring fully dissolved nutrients to prevent clogging and ensure uniform distribution. The scheme's allocation of INR 4,000 crore (USD 478.06 million) for 2024-25 targets coverage of 1.5 million hectares, directly translating to increased fertigation demand. In 2024, urea was priced at USD 328.25 per metric tonne, yet it boasts a high nutrient use efficiency. This efficiency becomes economically compelling for high-value crops where input costs represent a smaller share of total production expenses. Companies like Haifa Group have demonstrated yield improvements of 15-20% through precision fertigation protocols, establishing technical credibility that drives adoption among progressive farmers.

High Price Premium Versus Conventional Urea

The 2-4x price differential between specialty fertilizers and conventional urea creates a significant adoption barrier, particularly among price-sensitive smallholder farmers who represent 86% of India's agricultural population. In 2024, urea's wholesale price hovered around USD 328.2 per metric tonne, allowing farmers to avoid significant increases in working capital, even with enhanced nutrient use efficiency. For nearly a decade, the effective price has remained stable, granting nitrogen-heavy nutrition programs an artificial cost edge. The economic justification for specialty fertilizers requires demonstration of yield improvements that offset higher input costs, a value proposition that becomes challenging during periods of commodity price volatility. Credit constraints among smallholder farmers further limit their ability to invest in premium inputs, despite potential long-term soil health benefits.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Horticulture Acreage With Protected Cultivation

- Growth of Ag-Input E-Commerce Platforms Improving Last-Mile Access

- Fragmented Distribution Enabling Counterfeit Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-soluble fertilizers are the largest segment, command 53.3% of the India urea market share in 2025, reflecting their compatibility with modern irrigation systems and their superior nutrient-use efficiency, which justifies premium pricing. The segment's dominance stems from its alignment with the expansion of micro-irrigation and the growth of protected cultivation, where precise nutrient delivery becomes critical for optimizing crop performance. Controlled-release fertilizers represent the fastest-growing specialty type, with a 8.6% CAGR through 2031, driven by their ability to reduce application frequency and minimize nutrient losses from leaching and volatilization. Slow-release fertilizers maintain a smaller but stable market presence, primarily serving turf and ornamental applications where extended feeding periods are valued.

Liquid fertilizers occupy a niche position focused on foliar applications and fertigation systems, offering rapid nutrient uptake and flexibility in formulation adjustments. IFFCO's development of nano fertilizers represents an emerging category that could disrupt traditional specialty types, with their nano urea and nano DAP products demonstrating 20-year patent protection and government approval for commercial launch. The regulatory framework under the Fertilizer Control Order 1985 governs product specifications and quality standards, with recent amendments introducing streamlined registration processes for water-soluble fertilizers that enable faster market entry for innovative formulations.

Complete Report Scope:

- Speciality Type

- CRF

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Liquid Fertilizer

- SRF

- Water Soluble

- CRF

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Form

- Conventional

- Specialty

List of Companies Covered in this Report:

- Indian Farmers Fertiliser Cooperative Limited

- Chambal Fertilizers and Chemicals Limited

- National Fertilizers Limited

- Coromandel International Limited

- Gujarat Narmada Valley Fertilizers and Chemicals Limited

- Mangalore Chemicals and Fertilizers Limited

- Yara International ASA

- Zuari Agro Chemicals Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Rashtriya Chemicals and Fertilizers Limited

- Nagarjuna Fertilizers and Chemicals Limited

- Haifa Group

- ICL Group

- Mosaic Company

- IPL Biologicals Limited

- Smartchem Technologies Limited

- Aries Agro Limited

- Hifield Organics Inc.

- Aries Agro Produce India Private Limited

- K+S Aktiengesellschaft

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Nitrogen stands out as the most widely used nutrient in field crop cultivation

- 4.6.2 Adoption of micro-irrigation systems boosting water-soluble demand

- 4.6.3 Expansion of horticulture acreage with protected cultivation

- 4.6.4 Growth of ag-input e-commerce platforms improving last-mile access

- 4.6.5 Corporate/contract farming models favoring yield-maximizing inputs

- 4.6.6 Domestic polymer capacity additions lowering CRF production cost

- 4.7 Market Restraints

- 4.7.1 High price premium versus conventional urea

- 4.7.2 Fragmented distribution enabling counterfeit products

- 4.7.3 Limited agronomic advisory causing crop-burn risk

- 4.7.4 Import-dependence for coating materials and FX volatility

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Form

- 5.3.1 Conventional

- 5.3.2 Specialty

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Indian Farmers Fertiliser Cooperative Limited

- 6.4.2 Chambal Fertilizers and Chemicals Limited

- 6.4.3 National Fertilizers Limited

- 6.4.4 Coromandel International Limited

- 6.4.5 Gujarat Narmada Valley Fertilizers and Chemicals Limited

- 6.4.6 Mangalore Chemicals and Fertilizers Limited

- 6.4.7 Yara International ASA

- 6.4.8 Zuari Agro Chemicals Limited

- 6.4.9 Deepak Fertilisers and Petrochemicals Corporation Limited

- 6.4.10 Rashtriya Chemicals and Fertilizers Limited

- 6.4.11 Nagarjuna Fertilizers and Chemicals Limited

- 6.4.12 Haifa Group

- 6.4.13 ICL Group

- 6.4.14 Mosaic Company

- 6.4.15 IPL Biologicals Limited

- 6.4.16 Smartchem Technologies Limited

- 6.4.17 Aries Agro Limited

- 6.4.18 Hifield Organics Inc.

- 6.4.19 Aries Agro Produce India Private Limited

- 6.4.20 K+S Aktiengesellschaft

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS