PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073608

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073608

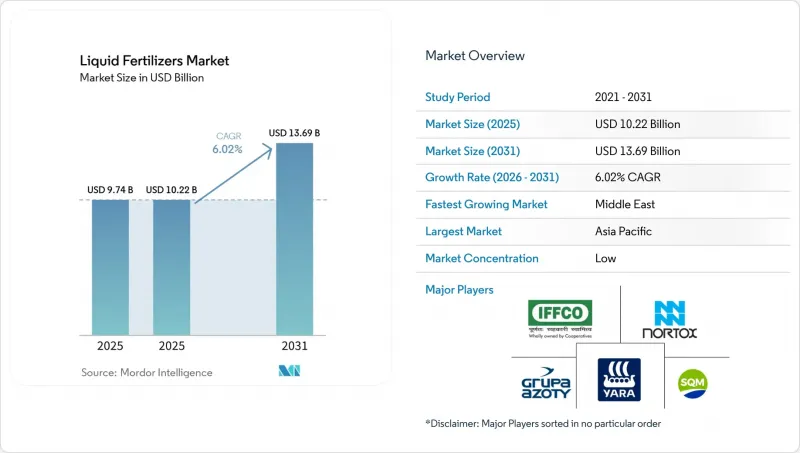

Liquid Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the liquid fertilizers market size was valued at USD 9.74 billion in 2025 and is estimated to grow from USD 10.22 billion in 2026 to USD 13.69 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031).

This report is Segmented by Type (Complex and Straight), by Application Mode (Fertigation and Foliar), by Crop Type (Field Crops, Horticultural Crops, and More), and by Geography (Asia-Pacific, Europe, North America, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Liquid Fertilizers Market Trends and Insights

Precision Irrigation Adoption Accelerates Liquid Uptake

Water scarcity is propelling drip and micro-sprinkler rollouts, and fertigation lines paired with soluble liquids reduce nutrient waste by up to 30% compared with granular broadcasting. The extensive use of drip and micro-sprinkler systems aligns water and nutrient delivery, allowing farmers to shift from granular top-dressing to in-line fertigation. This approach reduces runoff and leaching. The United States Department of Agriculture 2024 Fertilizer Production Expansion Program has allocated USD 500 million to enhance capacity, directly benefiting precision irrigation users. This reflects public acknowledgment of the 15-30% nutrient-use efficiency improvements achieved with liquid fertilizers . Liquids dissolve instantly, eliminating emitter clogging that undermines granular solubility in narrow lines.

Rapid Shift Toward Balanced Crop Nutrition Programs

The 4R stewardship framework emphasizes right source, rate, time, and placement, and multi-nutrient liquids deliver balanced blends in a single pass. Extension agents in the United States and France now recommend split nitrogen-phosphorus-micronutrient applications tied to crop growth stages, boosting uptake efficiency. Growers facing plateauing yield curves for single-nutrient programs view balanced liquids as the next lever for incremental gains. Agronomists also note that liquids lower soil acidification relative to repeated urea granule use, preserving long-term field productivity. The liquid fertilizers market benefits because reformulated blends earn premium margins while meeting sustainability metrics demanded by downstream food brands.

High Volatilization and Leaching Losses in Warm Climates

Soluble nitrogen faces rapid ammonia gas release above 30 °C, and monsoon rains wash unfixed nitrate below root zones within hours. Trials in Vietnam and Ghana showed nitrogen-use efficiency 15% to 25% lower than at temperate sites. Growers respond by limiting liquid use to greenhouses or protected horticulture, thereby capping volume growth. Inhibitor additives reduce losses but add USD 50-80 per metric ton, narrowing the cost gap with coated granules. Unless bio-based inhibitors become cheaper, adoption will lag in warm, humid regions.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies Favoring Fertigation Solutions

- Drone-Based Micro-Spray Fertilization Platforms

- Stricter Container-Weight Rules Raising Freight Expense

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers accounted for 58.7% of the liquid fertilizers market share in 2025, establishing them as the largest product category. Their dominance is attributed to their extensive use in variable-rate nutrient programs, which enable growers to address specific nutrient deficiencies with greater precision through individual nutrient applications. Nitrogenous liquid fertilizers remain a key component of straight-product demand, particularly in cereal production systems. Additionally, on-farm blending capabilities enhance their operational flexibility across various cropping environments.

Complex fertilizers are anticipated to be the fastest-growing segment, with a projected CAGR of 7.7% during 2026-2031. Multi-nutrient formulations are increasingly utilized in orchard, horticultural, and specialty crop systems, where a single application provides balanced nutrition. The ongoing development of chelated and specialty nutrient blends is driving their adoption in high-value agriculture. Furthermore, advancements in formulation technology are improving their compatibility with modern fertigation and precision nutrient management systems.

Complete Report Scope:

- Type

- Complex

- Straight

- By Nutrient

- Micronutrients

- Nitrogenous

- Phosphatic

- Potassic

- Secondary Macronutrients

- By Nutrient

- Application Mode

- Fertigation

- Foliar

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Geography

- Asia-Pacific

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

- Europe

- France

- Germany

- Italy

- Netherlands

- Russia

- Spain

- Ukraine

- United Kingdom

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- North America

- Canada

- Mexico

- United States

- Rest of North America

- South America

- Brazil

- Rest of South America

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific was the largest regional market, accounting for 39.9% of the liquid fertilizers market in 2025., buoyed by India's surge in drip subsidies and China's precision farming push. Japan and South Korea use recirculating nutrient solutions in greenhouse vegetable production to comply with strict discharge rules. Australia's broadacre cereal belt experiments with variable-rate liquid maps generated from conductivity scans, aiming to close intra-field yield gaps. Bangladesh, Pakistan, and Vietnam trail on absolute penetration, but demonstration plots under state extension programs are narrowing knowledge gaps among rice and vegetable growers.

The Middle East region is growing at an 8.1% CAGR through 2031, from a small base. Nigeria's tomato clusters and Kenya's avocado orchards adopted community fertigation hubs that pool stainless storage to manage capex hurdles. South Africa's wine and citrus exporters rely on iron and zinc chelates to meet European residue standards, and success stories travel quickly through grower networks.

North America and Europe are focusing on upgrading existing agricultural acreage with IoT-optimized dosing systems rather than expanding cultivated areas. In the United States, corn and soybean growers use real-time aerial imagery to calibrate mid-season liquid nitrogen applications, reducing excess use that could exceed state nutrient regulations. In Europe, the Nitrates Directive drives demand for precision liquid fertilizers that comply with the 170 kg N/ha limit, with notable adoption in countries such as the Netherlands and Denmark. Eastern European markets face challenges due to fragmented farms and limited fertigation infrastructure. Nonetheless, European Union carbon border taxes may provide funding opportunities for efficiency improvements. South America is experiencing significant growth rate, driven by Brazil's sugarcane fertigation practices and Argentina's specialty fruit exports.

- Yara International ASA

- Sociedad Quimica y Minera de Chile S.A.

- Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- Grupa Azoty S.A.

- Nortox SA

- ICL Group

- BMS Micro-Nutrients NV (Floridienne SA)

- Haifa Group

- Nutrien Ltd

- CF Industries Holdings, Inc.

- Kugler Company

- AgroLiquid

- Tessenderlo Kerley Inc (Tessenderlo Group)

- J. R. Simplot Company

- EuroChem Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 Report Offers

3 Executive Summary and Key Findings

4 Key Industry Trends

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision irrigation adoption accelerates liquid uptake

- 4.6.2 Rapid shift toward balanced crop nutrition programs

- 4.6.3 Government subsidies favoring fertigation solutions

- 4.6.4 Drone-based micro-spray fertilization platforms

- 4.6.5 On-farm IoT blending systems enabling just-in-time mixes

- 4.6.6 Nitrate-from-ammonia electrolysis lowering production cost

- 4.7 Market Restraints

- 4.7.1 High volatilization and leaching losses in warm climates

- 4.7.2 Corrosive storage and handling infrastructure costs

- 4.7.3 Per- and polyfluoroalkyl substances (PFAS) contamination scrutiny on certain chelating agents

- 4.7.4 Stricter container-weight rules are raising freight expenses

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 By Nutrient

- 5.1.2.1.1 Micronutrients

- 5.1.2.1.2 Nitrogenous

- 5.1.2.1.3 Phosphatic

- 5.1.2.1.4 Potassic

- 5.1.2.1.5 Secondary Macronutrients

- 5.1.2.1 By Nutrient

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest of Europe

- 5.4.3 Middle East

- 5.4.3.1 Saudi Arabia

- 5.4.3.2 United Arab Emirates

- 5.4.3.3 Turkey

- 5.4.3.4 Rest of Middle East

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Rest of South America

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Sociedad Quimica y Minera de Chile S.A.

- 6.4.3 Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- 6.4.4 Grupa Azoty S.A.

- 6.4.5 Nortox SA

- 6.4.6 ICL Group

- 6.4.7 BMS Micro-Nutrients NV (Floridienne SA)

- 6.4.8 Haifa Group

- 6.4.9 Nutrien Ltd

- 6.4.10 CF Industries Holdings, Inc.

- 6.4.11 Kugler Company

- 6.4.12 AgroLiquid

- 6.4.13 Tessenderlo Kerley Inc (Tessenderlo Group)

- 6.4.14 J. R. Simplot Company

- 6.4.15 EuroChem Group

7 Key Strategic Questions for Fertilizer CEOs