PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073632

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073632

North America Industrial Air Quality Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

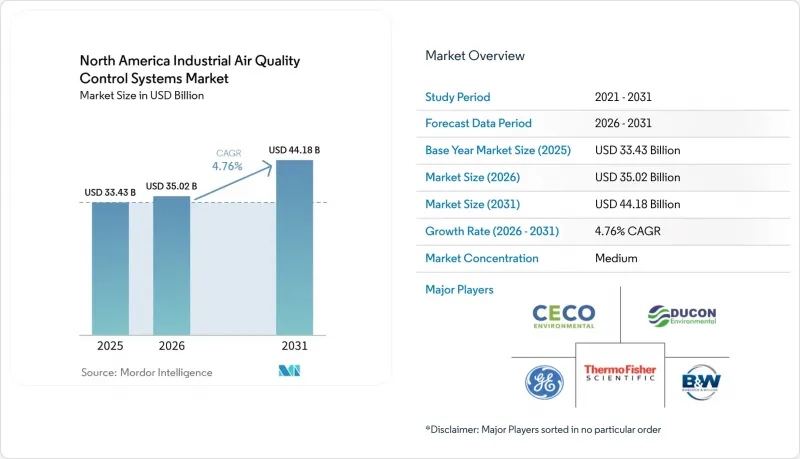

According to Mordor Intelligence, the north america industrial air quality control systems market size is expected to grow from USD 33.43 billion in 2025 to USD 35.02 billion in 2026 and is forecast to reach USD 44.18 billion by 2031 at 4.76% CAGR over 2026-2031.

This report is Segmented by Type (Electrostatic Precipitators, Flue-Gas Desulfurization, Scrubbers, and More), Pollutant Controlled (PM, Sox, Nox, VOC, and More), End-User Industry (Power Generation, Cement, Iron and Steel, Chemicals and Petrochemicals, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Industrial Air Quality Control Systems Market Trends and Insights

Stricter PM2.5 and Ozone Compliance Reshapes Permitting Economics

The U.S. Environmental Protection Agency lowered the primary annual PM2.5 standard to 9.0 µg/m3 in February 2024, which immediately tightened the compliance context for large industrial sources. This change reduced the operating cushion that many facilities had relied on when planning plant expansions or permit renewals. Projects that could once move forward with limited control upgrades now face a stronger need to prove lower emissions performance under stricter air quality review. The pressure increased further when Dallas-Fort Worth, Houston-Galveston-Brazoria, and San Antonio were reclassified from Moderate to Serious ozone nonattainment, effective in July 2024. That change lowered major source thresholds to 50 tons per year and pushed RACT obligations toward 2026 implementation windows. In the North America air quality control systems market, these combined rules are moving filter, scrubber, and NOx-control spending into current capital planning cycles.

Oil and Gas Methane and Sulfur Control Upgrades Expand Multi-Pollutant Demand

The EPA finalized a major package of methane and VOC controls for the oil and natural gas sector in March 2024, making this one of the most important compliance shifts affecting heavy industrial emissions equipment. The rule covers 28% of U.S. anthropogenic methane emissions and 23% of anthropogenic VOC emissions from the sector. It requires zero-emissions pneumatic controllers, quarterly optical gas imaging at multi-well sites, and 99.9% SO2 reduction from certain sweetening units. This is changing purchase behavior because gas processing and refining sites are increasingly evaluating sulfur scrubbing, vapor recovery, NOx reduction, and continuous monitoring as part of one investment cycle rather than as separate projects. Canada is also tightening industrial emissions policy for large emitters, which supports a broader regional procurement base for air quality control equipment. As a result, the North America air quality control systems market is seeing stronger multi-pollutant demand across the Gulf Coast, the Permian Basin, Alberta, and British Columbia.

Coal Retirements Reduce Legacy Retrofit Demand, but the Pace Is Uneven

Coal retirements are reducing one of the oldest recurring revenue pools for scrubbers, SCR systems, and particulate control retrofits. Coal-fired plants historically required frequent compliance upgrades, which made them a dependable source of aftermarket and replacement demand. As older units leave the grid, the installed base becomes smaller across the Midwest, Appalachia, the Southeast, and parts of Canada. The decline is still uneven because reliability concerns and fuel-price shifts have kept some aging units online longer than earlier assumptions suggested. That uneven retirement pattern preserves catalyst replacement, baghouse maintenance, and scrubber service work as part of the fleet even as total coal exposure falls. For the North America air quality control systems market, the effect is a gradual mix shift toward gas, waste-to-energy, and CCUS-related pretreatment rather than a sudden collapse in power-sector demand.

Other drivers and restraints analyzed in the detailed report include:

- CCUS-Ready Cement and Steel Retrofit Wave Creates Pre-Treatment Hardware Demand

- AI-Enabled Optimization and Predictive Maintenance Shifts the Value Proposition

- High Retrofit Capex and Outage Complexity Constrain Project Conversion Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flue-gas desulfurization held 32.1% of the North America air quality control systems market share in 2025, which kept it as the leading technology group across regulated heavy industrial sites. Its position reflects the continued need for sulfur control in power generation, refining, and sour-gas processing, where wet, dry, and semi-dry systems each serve different operating conditions. Wet FGD remains the preferred route in large-capacity power and refinery settings where sulfur loads are high and removal efficiency requirements are strict. Semi-dry systems are gaining ground in industrial boilers and similar sites where water handling and wastewater disposal are harder to manage. This leaves FGD with a broad installed base and strong replacement demand even as the technology mix evolves within the North America air quality control systems market.

Fabric and ceramic filters are the fastest-growing type, and the North America air quality control systems market size for this segment is expected to rise at a 5.3% CAGR through 2031. Demand is strongest in cement kilns, waste-to-energy plants, and steel facilities that need finer particulate capture than older electrostatic precipitators can consistently deliver under tighter PM limits. Pulse-jet fabric filters remain attractive because they can achieve very high collection efficiency while keeping pressure drop manageable in many high-temperature settings. SCR and SNCR systems also remain important for facilities managing NOx obligations, especially where ozone compliance is tightening in nearby air basins. Electrostatic precipitators still provide stable maintenance revenue, but growth is slower because more retrofit decisions are shifting toward filters, scrubbers, and integrated multi-pollutant platforms in the North America air quality control systems industry.

Complete Report Scope:

- By Type

- Electrostatic Precipitators (Dry & Wet)

- Flue-Gas Desulfurization (Wet, Dry, Semi-dry)

- Scrubbers (Wet, Dry, Marine)

- Selective Catalytic and Non-Catalytic Reduction

- Fabric/Ceramic Filters

- Mercury and VOC Control Units

- By Pollutant Controlled

- Particulate Matter (PM)

- SOx

- NOx

- Volatile Organic Compounds (VOC)

- Mercury and Air Toxics

- By End-user Industry

- Power Generation

- Cement

- Iron and Steel

- Chemicals and Petrochemicals

- Pulp and Paper

- Waste-to-Energy

- Others (Glass, Mining, etc.)

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Babcock & Wilcox Enterprises, Inc.

- CECO Environmental Corp.

- Ducon Technologies Inc.

- GE Vernova Inc.

- ANDRITZ AG

- Fuel Tech, Inc.

- Tri-Mer Corporation

- SLY LLC

- Donaldson Company, Inc.

- Nederman Holding AB

- Anguil Environmental Systems, Inc.

- Camfil AB

- ProcessBarron

- Valmet Oyj

- FLSmidth & Co. A/S

- Mitsubishi Power, Ltd.

- Thermax Limited

- Monroe Environmental Corporation

- Beltran Technologies, Inc.

- Hamon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends and Developments

- 4.3 Market Drivers

- 4.3.1 Stricter PM2.5 and ozone compliance

- 4.3.2 Oil and gas methane and sulfur control upgrades

- 4.3.3 CCUS-ready cement and steel retrofit wave

- 4.3.4 AI-enabled optimization and predictive maintenance

- 4.3.5 Tighter permit headroom from lower PM2.5 SILs

- 4.4 Market Restraints

- 4.4.1 Coal retirements reduce legacy retrofit demand

- 4.4.2 High retrofit capex and outage complexity

- 4.4.3 Skilled labor and catalyst lead-time bottlenecks

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Electrostatic Precipitators (Dry & Wet)

- 5.1.2 Flue-Gas Desulfurization (Wet, Dry, Semi-dry)

- 5.1.3 Scrubbers (Wet, Dry, Marine)

- 5.1.4 Selective Catalytic and Non-Catalytic Reduction

- 5.1.5 Fabric/Ceramic Filters

- 5.1.6 Mercury and VOC Control Units

- 5.2 By Pollutant Controlled

- 5.2.1 Particulate Matter (PM)

- 5.2.2 SOx

- 5.2.3 NOx

- 5.2.4 Volatile Organic Compounds (VOC)

- 5.2.5 Mercury and Air Toxics

- 5.3 By End-user Industry

- 5.3.1 Power Generation

- 5.3.2 Cement

- 5.3.3 Iron and Steel

- 5.3.4 Chemicals and Petrochemicals

- 5.3.5 Pulp and Paper

- 5.3.6 Waste-to-Energy

- 5.3.7 Others (Glass, Mining, etc.)

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Babcock & Wilcox Enterprises, Inc.

- 6.4.2 CECO Environmental Corp.

- 6.4.3 Ducon Technologies Inc.

- 6.4.4 GE Vernova Inc.

- 6.4.5 ANDRITZ AG

- 6.4.6 Fuel Tech, Inc.

- 6.4.7 Tri-Mer Corporation

- 6.4.8 SLY LLC

- 6.4.9 Donaldson Company, Inc.

- 6.4.10 Nederman Holding AB

- 6.4.11 Anguil Environmental Systems, Inc.

- 6.4.12 Camfil AB

- 6.4.13 ProcessBarron

- 6.4.14 Valmet Oyj

- 6.4.15 FLSmidth & Co. A/S

- 6.4.16 Mitsubishi Power, Ltd.

- 6.4.17 Thermax Limited

- 6.4.18 Monroe Environmental Corporation

- 6.4.19 Beltran Technologies, Inc.

- 6.4.20 Hamon

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment