PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073633

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073633

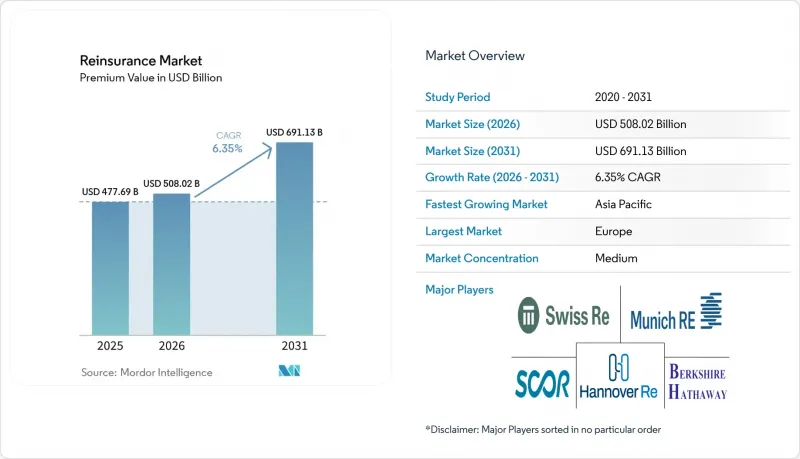

Reinsurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the reinsurance market size in terms of premium value is expected to grow from USD 477.69 billion in 2025 to USD 508.02 billion in 2026 and is forecast to reach USD 691.13 billion by 2031 at 6.35% CAGR over 2026-2031.

This report is Segmented by Reinsurance Type (Facultative, Treaty), Line of Business (Property and Casualty, Life and Health, and More), Distribution Channel (Direct Writing, Broker-Mediated), Capital Source (Traditional Rated Reinsurers, Alternative Capital), and Region (North America, Europe, South America, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Reinsurance Market Trends and Insights

Growing Insurance Penetration in Emerging Economies

Insurance uptake continues to rise across high-growth markets, driving sustained demand for the reinsurance market as cedents seek diversified capacity beyond domestic risk pools. India is on pace to hold the world's third-largest insurance sector by decade-end, with health and motor products expanding quickly under regulatory encouragement . China's favorable treatment of Hong Kong-based reinsurers underscores Beijing's aim of integrating financial services while retaining access to foreign capital. Rapid cyber-risk accumulation in Asia-Pacific, already 7% of global cyber premiums, is another catalyst, producing double-digit reinsurance growth as local carriers seek balance-sheet relief. Mandatory lines such as crop and motor third-party liability are maturing ahead of GDP, further cementing structural demand for outward reinsurance. Regional solvency regimes, however, impose compliance costs that only well-capitalized reinsurers can absorb, reinforcing industry consolidation.

Escalating Climate-Related Natural Catastrophe Losses Raise Demand

Insured NatCat losses topped historical averages again in 2024, making that year among the costliest on record and elevating the reinsurance market's centrality in risk transfer. Munich Re alone absorbed EUR 3.89 billion of major losses, including USD 1.3 billion from California wildfires. The growing frequency of severe convective storms is widening the loss footprint beyond familiar hurricane and earthquake zones, requiring fresh capital and new modeling approaches. Investors now view heightened catastrophe activity as a structural shift rather than transient volatility, prompting repricing across catastrophe bonds and collateralized reinsurance. Parametric covers that pay out rapidly on objective triggers are proliferating, helping close protection gaps where indemnity products lag. Governments are also partnering with reinsurers to craft public-private pools that share residual risk and support post-disaster rebuilding.

Geopolitical & Macro-Economic Volatility

Rising geopolitical tension and uneven macroeconomic conditions weaken primary insurance growth and complicate cross-border reinsurance placements. Currency swings and inflation induce model risk, especially for reinsurers reporting in hard currencies but paying claims in depreciating local currencies. Trade frictions add regulatory checks that elongate placement timetables and inflate compliance costs. Supply-chain disruptions are forcing higher risk premiums in marine and contingent business interruption covers, dampening cedent appetites where margins are thin. Finally, higher interest-rate volatility complicates asset-liability management, challenging reinsurers' investment returns at the very time cat losses remain elevated.

Other drivers and restraints analyzed in the detailed report include:

- Tight Primary-Insurer Capital Buffers Post-IFRS 17

- Hard-Market Pricing Cycle Boosts Reinsurer Returns

- Regulatory Capital Constraints (Solvency II, RBC)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Treaty business accounted for 76.20% reinsurance market share in 2025, a level that translated into USD 358.2 billion of ceded premium and underscored cedents' preference for portfolio-wide protection. Facultative placements, though smaller, are forecast to grow at an 8.05% CAGR as underwriters respond to large-scale solar plants, offshore wind, and bespoke cyber exposures that standard treaties omit. Digital administration platforms are simplifying bordereaux handling, allowing treaty programs to embed parametric triggers for quicker recoveries and reducing frictional costs by up to 25% according to Swiss Re's internal metrics.

Demand for facultative coverage is also bolstered by mega-projects such as smart-city infrastructure and green hydrogen facilities that exceed individual treaty limits. Insurtech analytics now enable cedents to assess facultative quotes in hours rather than days, closing placement gaps more efficiently. Many reinsurers are bundling treaty and facultative offerings to deepen client penetration, thereby tightening switching costs and sustaining the reinsurance market's overall growth trajectory.

Property and Casualty held 62.40% of the reinsurance market size in 2025, supported by consistent demand for catastrophe and liability capacity. Specialty lines - cyber, aviation, marine, energy - are projected to grow at 11.18% CAGR, adding more than USD 20 billion in ceded premium by 2031. Growth is fueled by digitization, supply-chain complexity, and new energy transition risks that fall outside classic P&C frameworks.

Hannover Re's cloud outage cat bond signals a broader wave of specialty risk securitization that could eventually influence P&C program design. ESG expectations are spurring demand for renewable-energy performance guarantees, another niche requiring tailored reinsurance. As specialty lines mature, reinsurers are forming dedicated teams and forging partnerships with cybersecurity firms, enabling more granular pricing and loss prevention services. These initiatives diversify earnings and help reinsurers manage correlation risk across their portfolios.

Complete Report Scope:

- By Reinsurance Type

- Facultative Reinsurance

- Treaty Reinsurance

- By Line of Business

- Property & Casualty

- Life & Health

- Specialty (Aviation, Marine, Energy)

- Others

- By Distribution Channel

- Direct Writing

- Broker-Mediated

- By Capital Source

- Traditional Rated Reinsurers

- Alternative Capital (ILS, Sidecars)

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East & Africa

- North America

Geography Analysis

Europe anchored 31.40% of the 2025 reinsurance market size, supported by mature insurance penetration, sophisticated solvency oversight, and hub ecosystems in London, Zurich, and continental centers. Severe convective storm losses and evolving ESG mandates are reshaping product development and capital deployment, prompting reinsurers to integrate climate-science data into continental pricing. Solvency UK's divergence may gradually redirect some placements to European entities while London retains strength in specialty risk through Lloyd's syndicates.

Asia-Pacific is the fastest-expanding region at a projected 7.23% CAGR through 2031, bringing the reinsurance market new premium pools in India, China, and Southeast Asia. Preferential capital treatment for Hong Kong-domiciled reinsurers facilitates Mainland access, illustrating policymakers' support for cross-border risk transfer. Rapid cyber exposure growth - nearly 50% annually - positions the region as a testing ground for digital parametric solutions. Mandatory health and motor schemes in India and the GCC also pull in proportional reinsurance, bolstering multi-line diversification in local markets.

North America remains the largest single-country market, underpinned by the United States' deep capital markets and substantial catastrophe needs. The NAIC's review of RBC factors could influence the reinsurance market share of offshore collateralized providers that currently enjoy credit for clean letters of credit. Meanwhile, reinsurers are expanding Latin American footprints via Miami hubs to tap growth in agriculture and parametric earthquake covers. The Middle East and Africa, though smaller, show rising demand linked to infrastructure investments and health-insurance mandates, areas where reinsurance supports solvency and product innovation.

- Munich Re

- Swiss Re

- Hannover Re

- Berkshire Hathaway Re

- SCOR SE

- Lloyd's

- China Re

- Reinsurance Group of America

- Everest Re

- PartnerRe

- RenaissanceRe

- Sompo Re

- AXA XL Re

- General Re

- Tokio Marine Kiln / TMR

- Mapfre Re

- QBE Re

- Korean Re

- Peak Re

- Odyssey Re

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing insurance penetration in emerging economies

- 4.2.2 Escalating climate-related NatCat losses raise demand

- 4.2.3 Tight primary-insurer capital buffers post-IFRS 17

- 4.2.4 Hard-market pricing cycle boosts reinsurer returns

- 4.2.5 Parametric & cyber reinsurance innovation (under-reported)

- 4.2.6 Embedded-finance platforms ceding micro-risk pools (under-reported)

- 4.3 Market Restraints

- 4.3.1 Geopolitical & macro-economic volatility

- 4.3.2 Regulatory capital constraints (Solvency II, RBC)

- 4.3.3 ILS investors' risk-return fatigue (under-reported)

- 4.3.4 AI-driven model risk & data-privacy hurdles (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Market Risks & Impact Analysis

5 Market Size & Growth Forecasts

- 5.1 By Reinsurance Type

- 5.1.1 Facultative Reinsurance

- 5.1.2 Treaty Reinsurance

- 5.2 By Line of Business

- 5.2.1 Property & Casualty

- 5.2.2 Life & Health

- 5.2.3 Specialty (Aviation, Marine, Energy)

- 5.2.4 Others

- 5.3 By Distribution Channel

- 5.3.1 Direct Writing

- 5.3.2 Broker-Mediated

- 5.4 By Capital Source

- 5.4.1 Traditional Rated Reinsurers

- 5.4.2 Alternative Capital (ILS, Sidecars)

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Munich Re

- 6.4.2 Swiss Re

- 6.4.3 Hannover Re

- 6.4.4 Berkshire Hathaway Re

- 6.4.5 SCOR SE

- 6.4.6 Lloyd's

- 6.4.7 China Re

- 6.4.8 Reinsurance Group of America

- 6.4.9 Everest Re

- 6.4.10 PartnerRe

- 6.4.11 RenaissanceRe

- 6.4.12 Sompo Re

- 6.4.13 AXA XL Re

- 6.4.14 General Re

- 6.4.15 Tokio Marine Kiln / TMR

- 6.4.16 Mapfre Re

- 6.4.17 QBE Re

- 6.4.18 Korean Re

- 6.4.19 Peak Re

- 6.4.20 Odyssey Re

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment