PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073649

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073649

Green Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

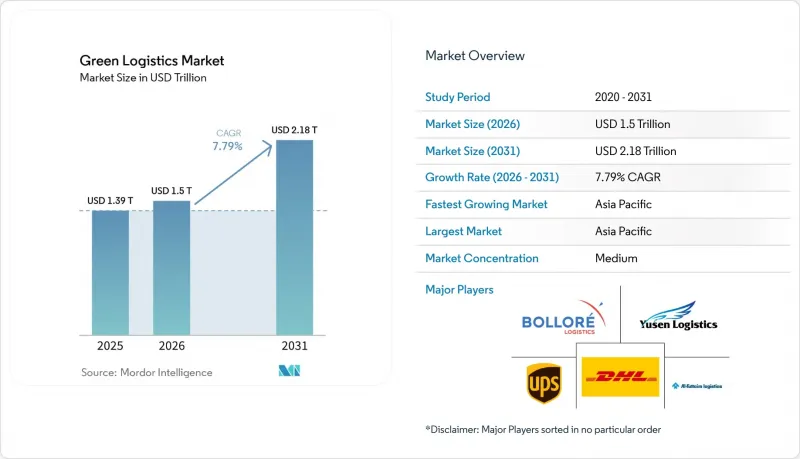

According to Mordor Intelligence, the green logistics market size was valued at USD 1.39 trillion in 2025 and estimated to grow from USD 1.5 trillion in 2026 to reach USD 2.18 trillion by 2031, at a CAGR of 7.79% during the forecast period (2026-2031).

This report Segments the Industry Into by End User (Retail and E-Commerce, Manufacturing & Industrial, Automotive, Healthcare & Pharmaceuticals, Food & Beverages, and More), by Service Type (Warehousing & Storage, Transportation, and Value-Added Services), and by Geography (North America, South America, Asia-Pacific, Europe, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Green Logistics Market Trends and Insights

Net-zero mandates tightening across supply chains

Mandatory disclosure rules such as the EU Corporate Sustainability Reporting Directive and California's Advanced Clean Truck regulation are forcing shippers to embed carbon criteria into bids, accelerating demand for certified low-emission services. DHL already targets 30% sustainable aviation fuel (SAF) blending by 2030, while UPS plans fleet-wide carbon neutrality by 2050. Procurement leaders now allocate up to 3% of logistics budgets to compliance-linked decarbonization projects, turning emissions performance into a contract-winning differentiator. Providers showing audit-ready data enjoy first-mover advantages in lane awards, especially on EU-US trade flows. Absent credible roadmaps, carriers risk exclusion from preferred supplier lists as early as 2027.

E-commerce boom accelerating low-carbon last-mile solutions

Spiking parcel volumes concentrate emissions in dense urban nodes, where municipalities deploy zero-emission zones and congestion pricing. AI-guided routing of electric vans has cut delivery times by 15-20% while lowering CO2 by as much as 40% in large European capitals. Retailers such as Mars are co-funding 300 electric Class 8 trucks with Einride, targeting 20,000 t annual reductions by 2030. Although consumer willingness to pay premiums remains muted, regulatory incentives and brand commitments are pushing "green delivery" toward default status in the green logistics market.

High upfront capex for zero-emission fleets & infrastructure

Purchase premiums on battery-electric trucks range from USD 70,000-113,000 per unit, while megawatt chargers can exceed USD 3.1 million per kilometer on dedicated electric-road projects. Smaller carriers struggle to secure financing, and uncertainty over residual values still dampens resale-based funding models. Although operating savings accumulate over time, near-term cash-flow strain hinders scale adoption in emerging economies lacking green credit facilities.

Other drivers and restraints analyzed in the detailed report include:

- Rapid cost declines in battery-electric & fuel-cell trucks

- AI-enabled route & load optimization, cutting emissions

- Limited charging & green-fuel infrastructure outside Tier-1 routes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing & industrial shippers accounted for 26.20% of the green logistics market in 2025, reflecting decades-long compliance cultures and predictable shipping patterns that simplify emissions auditing. Their embedded supplier scorecards channel freight budgets toward providers with asset-based decarbonization roadmaps, reinforcing share dominance. Energy-intensive plants increasingly negotiate integrated renewable power and electric truck packages that lock in multiyear carbon reductions. Retail & e-commerce, though smaller today, is advancing at an 17.35% CAGR, propelled by urban micro-fulfilment centers and mandated zero-emission delivery windows in metropolitan zones. The green logistics market size for e-commerce shipments is set to climb sharply as returns volumes swell and merchants internalize the cost of "free" delivery. Automotive OEMs, meanwhile, trial electric car carriers to cut distribution emissions by 40% per unit, while healthcare brands co-invest in SAF corridors to safeguard cold-chain integrity without raising carbon intensity.

Electric-vehicle density, standardized pallets, and digitized bill-of-lading systems grant manufacturers visibility into cradle-to-gate footprints, enabling continuous optimization. In contrast, e-commerce operators leverage AI to orchestrate parcel lockers, bike couriers, and dark-store networks that eliminate failed delivery attempts. Both archetypes converge on data-centric performance dashboards that convert emissions tracking into a competitive procurement variable, illustrating how diverse end users amplify growth in the green logistics market.

Complete Report Scope:

- By End User (Value, USD Bn)

- Retail & E-commerce

- Manufacturing & Industrial

- Automotive

- Healthcare & Pharmaceuticals

- Food & Beverages

- Chemicals & Hazardous Materials

- Others

- By Service Type (Value)

- Warehousing and Storage

- Transportation

- Road

- Rail

- Sea and Inland Waterways

- Air

- Value-Added Services (Packaging, Kitting, Labelling)

- Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Geography Analysis

APAC led the green logistics market with a 36.65% revenue share in 2025 and is growing fastest at 8.62% CAGR through 2031. China's nationwide green-freight corridors and subsidies for electric Class 8 trucks accelerate fleet turnover, while India leverages new-build industrial parks to embed rooftop PV and EV charging from inception . Japan continues to modernize freight rail, expanding its modal shift program to lower highway congestion and cut logistics CO2. Southeast Asian nations capitalize on technology transfer, integrating battery swapping and microgrid solutions into port expansions to leapfrog legacy infrastructure.

North America remains the second-largest regional contributor, buoyed by the US federal target for 100% zero-emission truck sales by 2040 and tax credits that slash acquisition costs on Class 7-8 electrics. California's Advanced Clean Truck rule already compels OEMs to meet escalating ZEV sales quotas, driving early deployment of charging hubs across I-5 and I-10 corridors. Canada's anti-greenwashing legislation, effective June 2024, imposes fines up to CAD 10 million for misleading environmental claims, pushing carriers toward audit-ready disclosures, while Mexico promotes green-border programs that synchronize emissions standards on North-South trade routes.

Europe enjoys the world's most sophisticated policy mix-carbon pricing, eHighway pilots, and 43% CO2 cut mandates for heavy trucks by 2030-making zero-emission freight a regulatory certainty. Sweden's electric road classes expanded to over 50 km in 2025, generating performance data that informs Germany's national rollout. Logistics firms deploy low-carbon fleets as a licence-to-operate; CEVA's addition of 23 electric trucks curbs 38,300 t of CO2 annually, while integrated charging networks protect uptime. Eastern European lanes, though lagging infrastructure, attract EU cohesion funds earmarked for green corridors, promising convergence by the end of the decade.

The Middle East and Africa are nascent but rapidly mobilizing. The UAE's Net Zero 2050 Strategy backs solar-powered logistics parks at Jebel Ali, and Saudi Arabia links green hydrogen pilots to freight trials on the Riyadh-Jeddah corridor. South Africa's carbon tax nudges carriers toward biodiesel blends, yet grid reliability challenges slow widespread fleet electrification. Overall, regional heterogeneity ensures that localized policy incentives, infrastructure readiness, and industrial baselines dictate adoption speed, but each geography now features anchor projects that signal irreversible momentum in the green logistics market.

- DHL Group

- United Parcel Service (UPS)

- FedEx Corporation

- GEODIS

- Hellmann Worldwide Logistics

- Kuehne + Nagel International AG

- Nippon Express

- CEVA Logistics

- XPO Logistics

- DSV A/S

- Yusen Logistics Co., Ltd.

- Bollore Logistics

- Al-Futtaim Logistics

- Mahindra Logistics Ltd.

- Americold Logistics

- GXO Logistics

- C.H. Robinson Worldwide, Inc.

- Lineage Logistics

- JD Logistics

- Ryder System, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Net-zero mandates tightening across global supply chains

- 4.2.2 E-commerce boom accelerating demand for low-carbon last-mile solutions

- 4.2.3 Rapid cost declines in battery-electric & fuel-cell trucks

- 4.2.4 AI-enabled route & load optimisation cutting emissions

- 4.2.5 Roll-out of electric road systems on heavy-freight corridors

- 4.2.6 Emerging "Green-as-a-Service" contractual models monetising carbon savings

- 4.3 Market Restraints

- 4.3.1 High upfront capex for zero-emission fleets & infrastructure

- 4.3.2 Fragmented global standards for carbon reporting & green fuels

- 4.3.3 Limited charging & green-fuel infrastructure outside Tier-1 routes

- 4.3.4 Rising litigation/penalties linked to ESG-greenwashing claims

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By End User (Value, USD Bn)

- 5.1.1 Retail & E-commerce

- 5.1.2 Manufacturing & Industrial

- 5.1.3 Automotive

- 5.1.4 Healthcare & Pharmaceuticals

- 5.1.5 Food & Beverages

- 5.1.6 Chemicals & Hazardous Materials

- 5.1.7 Others

- 5.2 By Service Type (Value)

- 5.2.1 Warehousing and Storage

- 5.2.2 Transportation

- 5.2.2.1 Road

- 5.2.2.2 Rail

- 5.2.2.3 Sea and Inland Waterways

- 5.2.2.4 Air

- 5.2.3 Value-Added Services (Packaging, Kitting, Labelling)

- 5.3 Geography (Value)

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Europe

- 5.3.4.1 United Kingdom

- 5.3.4.2 Germany

- 5.3.4.3 France

- 5.3.4.4 Spain

- 5.3.4.5 Italy

- 5.3.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.4.8 Rest of Europe

- 5.3.5 Middle East And Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 United Parcel Service (UPS)

- 6.4.3 FedEx Corporation

- 6.4.4 GEODIS

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Kuehne + Nagel International AG

- 6.4.7 Nippon Express

- 6.4.8 CEVA Logistics

- 6.4.9 XPO Logistics

- 6.4.10 DSV A/S

- 6.4.11 Yusen Logistics Co., Ltd.

- 6.4.12 Bollore Logistics

- 6.4.13 Al-Futtaim Logistics

- 6.4.14 Mahindra Logistics Ltd.

- 6.4.15 Americold Logistics

- 6.4.16 GXO Logistics

- 6.4.17 C.H. Robinson Worldwide, Inc.

- 6.4.18 Lineage Logistics

- 6.4.19 JD Logistics

- 6.4.20 Ryder System, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment