PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073655

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073655

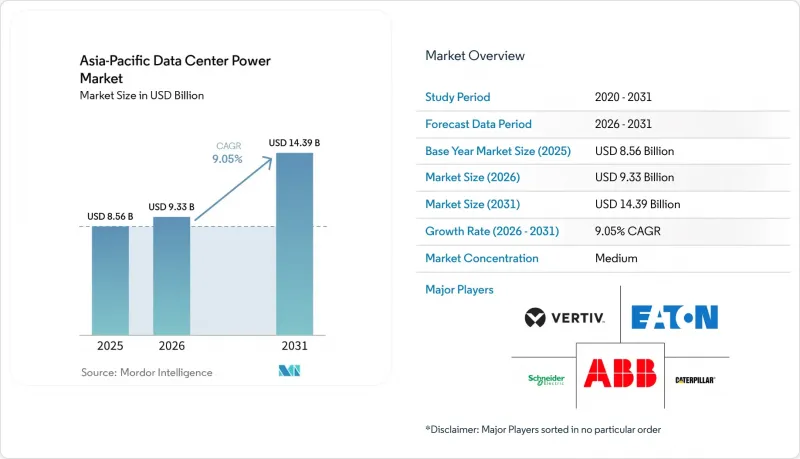

Asia-Pacific Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific data center power market size was valued at USD 8.56 billion in 2025 and estimated to grow from USD 9.33 billion in 2026 to reach USD 14.39 billion by 2031, at a CAGR of 9.05% during the forecast period (2026-2031).

This report is Segmented by Component (Electrical Solutions and Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV) and by Country. The Market Forecasts are Provided in Terms of Value (USD)

Asia-Pacific Data Center Power Market Trends and Insights

Hyperscale & AI-led Mega-Campus Build-out

AI training clusters now demand 40-50 kW per rack, more than five times traditional deployments, forcing total redesigns of distribution topologies and redundancy schemes. Wide-bandgap power semiconductors such as silicon carbide reduce conversion losses, while liquid cooling becomes standard in new halls to maintain thermal stability, Oak Ridge National Laboratory. Projects like Singtel's Banyan Park II in Singapore specify seismic-resilient busways and rack-level liquid manifolds to future-proof against higher AI loads. These systems integrate battery storage for ride-through support, smoothing grid transients, and enabling more aggressive load step changes without generator starts. The cascading effect raises specification levels across colocation builds as tenants request AI-ready capacity.

Government Digital-Economy & Data-Sovereignty Incentives

Policies in China and India require domestic data residency, obliging cloud providers to commission local hyperscale campuses and upgrade power distribution for higher availability tiers. Singapore's public-private research program with Equinix funds USD 4 million in sustainable power prototypes targeting tropical operating conditions. ASEAN frameworks encourage renewable integration that could meet 30% of data-center demand by 2030. Incentive schemes in Malaysia and Vietnam grant tariff rebates for facilities that deploy on-site solar and high-efficiency UPS. As regulation sets clear procurement timelines, volume commitments for switchgear and energy storage rise, supporting predictable supply-chain scaling.

Up-front Capex for High-Efficiency Power Systems

Advanced UPS and silicon-carbide converters cost up to 40% more than legacy equipment, a hurdle for smaller providers with constrained balance sheets. Liquid-cooling integration demands factory-prefabricated busbar and pump manifolds, raising installation complexity and lead times. In emerging economies where average rack loads still hover near 8 kW, operators often delay upgrades until customer demand materializes. Financing mechanisms such as energy-as-a-service contracts are beginning to spread, but adoption remains uneven, limiting near-term penetration of the most efficient architectures.

Other drivers and restraints analyzed in the detailed report include:

- Cloud/5G Traffic Surge Elevating Power Density

- High Electricity Tariffs Boosting Demand for Efficient UPS & PDUs

- Grid & Land Constraints in Tier-1 APAC Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UPS systems held the largest 31.65% revenue share in 2025 within the Asia-Pacific data center power market, underscoring their role in safeguarding always-on digital services. Adoption of lithium-ion batteries and silicon-carbide power trains pushes online efficiency above 96%, trimming operating expenditures despite higher unit prices. The component mix is changing as integrated UPS-battery modules reduce footprint and simplify maintenance. Intelligent PDUs, the fastest-growing sub-segment with a 10.3% CAGR, embed per-outlet metering that feeds AI analytics for workload placement, reducing stranded power capacity. Generators retain critical backup status but fuel-cell prototypes are gaining pilot traction among sustainability-focused hyperscalers.

External pressures from electricity-price volatility accelerate the deployment of battery energy storage that doubles as ride-through support and demand-charge mitigation. Switchgear advances concentrate on arc-flash safety and remote diagnostics that lower truck rolls. Remote power panels rise in edge deployments where technicians are scarce and uptime tolerance is low. Service revenue grows as operators contract OEMs for predictive maintenance tied to digital twins, reflecting the rising complexity of modern power trains across the Asia-Pacific data center power industry.

Colocation operators commanded 53.85% of the Asia-Pacific data center power market in 2025 by aggregating enterprise demand and leveraging economies of scale. Their business model supports large multitenant halls where modular 2-3 MW blocks standardize power design and shorten build schedules. Hyperscale cloud providers, however, are expanding at 10.05% CAGR as sovereign-cloud mandates drive local build commitments from global platforms. These sites integrate high-density AI clusters, necessitating direct-to-chip liquid cooling and dedicated 400 VAC busways that traditional colocation layouts rarely accommodate.

Enterprises adopt hybrid architectures, retaining latency-sensitive workloads on-premises while renting burst capacity from colo and hyperscale platforms. Edge nodes proliferate near 5G towers, requiring compact yet highly reliable power shelves that share design DNA with large facilities. Consequently, solutions vendors tailor portfolios that span kilowatt-class edge racks to 150 MW hyperscale farms, reinforcing cross-segment technology transfer within the Asia-Pacific data center power market.

Complete Report Scope:

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

- By Country

- Australia

- China

- India

- Indonesia

- Philippines

- Singapore

- Malaysia

- Japan

- New Zealand

- Other Asia-Pacific Countries

List of Companies Covered in this Report:

- ABB

- Schneider Electric

- Vertiv

- Eaton

- Huawei Digital Power

- Caterpillar

- Cummins

- Rolls-Royce Power Systems (MTU)

- Delta Electronics

- Legrand

- Mitsubishi Electric

- Socomec

- Piller Power Systems

- Rittal

- Kohler Power

- Cisco (DCIM and Smart-UPS integration)

- Fujitsu (facility services)

- AEG Power Solutions

- Tripp Lite

- Generac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale and AI-led mega-campus build-out

- 4.2.2 Government digital-economy and data-sovereignty incentives

- 4.2.3 Cloud/5G traffic surge elevating power density

- 4.2.4 High electricity tariffs boosting demand for efficient UPS and PDUs

- 4.2.5 Grid-connection delays driving onsite micro-grids

- 4.2.6 Corporate 100 %-renewable commitments (on-site solar and BESS)

- 4.3 Market Restraints

- 4.3.1 Up-front capex for high-efficiency power systems

- 4.3.2 Grid and land constraints in Tier-1 APAC hubs

- 4.3.3 Diesel-price volatility inflating generator OPEX

- 4.3.4 Skilled-labour gap for liquid-cooling power installs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Electrical Solutions

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.2.1 Diesel Generators

- 5.1.1.2.2 Gas Generators

- 5.1.1.2.3 Hydrogen Fuel-cell Generators

- 5.1.1.3 Power Distribution Units

- 5.1.1.4 Switchgear

- 5.1.1.5 Transfer Switches

- 5.1.1.6 Remote Power Panels

- 5.1.1.7 Energy-storage Systems

- 5.1.2 Service

- 5.1.2.1 Installation and Commissioning

- 5.1.2.2 Maintenance and Support

- 5.1.2.3 Training and Consulting

- 5.1.1 Electrical Solutions

- 5.2 By Data Center Type

- 5.2.1 Hyperscaler/Cloud Service Providers

- 5.2.2 Colocation Providers

- 5.2.3 Enterprise and Edge Data Center

- 5.3 By Data Center Size

- 5.3.1 Small Size Data Centers

- 5.3.2 Medium Size Data Centers

- 5.3.3 Large Size Data Centers

- 5.3.4 Massive Size Data Centers

- 5.3.5 Mega Size Data Centers

- 5.4 By Tier Level

- 5.4.1 Tier I and II

- 5.4.2 Tier III

- 5.4.3 Tier IV

- 5.5 By Country

- 5.5.1 Australia

- 5.5.2 China

- 5.5.3 India

- 5.5.4 Indonesia

- 5.5.5 Philippines

- 5.5.6 Singapore

- 5.5.7 Malaysia

- 5.5.8 Japan

- 5.5.9 New Zealand

- 5.5.10 Other Asia-Pacific Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB

- 6.4.2 Schneider Electric

- 6.4.3 Vertiv

- 6.4.4 Eaton

- 6.4.5 Huawei Digital Power

- 6.4.6 Caterpillar

- 6.4.7 Cummins

- 6.4.8 Rolls-Royce Power Systems (MTU)

- 6.4.9 Delta Electronics

- 6.4.10 Legrand

- 6.4.11 Mitsubishi Electric

- 6.4.12 Socomec

- 6.4.13 Piller Power Systems

- 6.4.14 Rittal

- 6.4.15 Kohler Power

- 6.4.16 Cisco (DCIM and Smart-UPS integration)

- 6.4.17 Fujitsu (facility services)

- 6.4.18 AEG Power Solutions

- 6.4.19 Tripp Lite

- 6.4.20 Generac

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment