PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073658

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073658

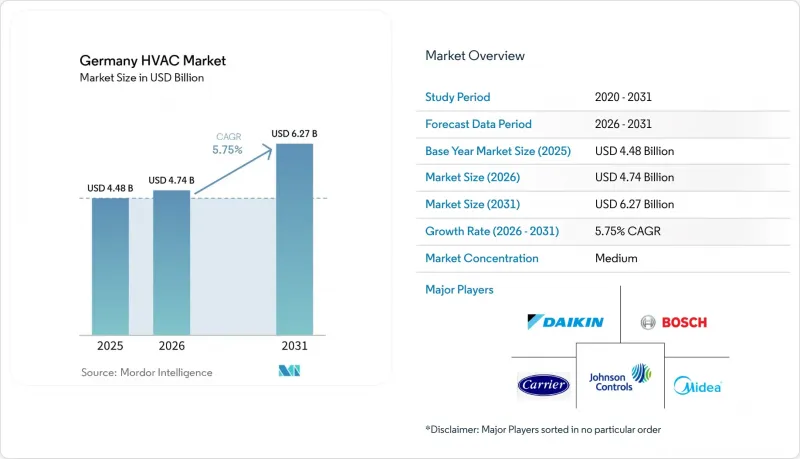

Germany HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany HVAC market size was valued at USD 4.48 billion in 2025 and estimated to grow from USD 4.74 billion in 2026 to reach USD 6.27 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031).

This report is Segmented by Component (HVAC Equipment, HVAC Services), End-User Industry (Residential, Commercial, Industrial, Public and Institutional), Implementation Type (New Construction, Retrofit), and Geography (North, South, East, West, Central). The Market Forecasts are Provided in Terms of Value (USD).

Germany HVAC Market Trends and Insights

Building Energy Act Electrification Push

The Building Energy Act took effect in 2024, obligating every new heating system to source at least 65% of its energy from renewables. Enforcement triggered a rapid shift toward heat pumps in Germany, which powered nearly seven in ten new residential projects in 2024. The rule also created a predictable retrofit pipeline because fossil-fuel systems may operate until their economic end of life, but must be replaced with compliant alternatives by 2045. More than 10,000 municipalities are drafting local heat plans that favor networked heat pumps and low-temperature district grids. Together, these measures lock in sustained demand across the Germany HVAC market.

Heat Pump Uptake in New-Build Residential Segment

Heat pump penetration skyrocketed after 2024 as total system cost dropped 12% year over year while gas prices stayed elevated. Air-source units claim 78% of new installations because of their lower capex and easier siting, whereas ground-source models serve noise-sensitive or space-constrained projects. The transition fuels parallel growth in thermal storage, smart thermostats, and envelope upgrades that maximize heat-pump efficiency. Contractors deepen specialization in refrigerant handling, commissioning, and digital controls, reinforcing the service orientation of the Germany HVAC market.

Skilled Installer Shortage

Roughly 60,000 HVAC positions were vacant in 2024, and apprenticeship enrollment fell 23% in five years. Heat pumps demand additional competencies in electrical wiring, refrigerant management, and digital commissioning, creating bottlenecks in residential and small-commercial projects. Rural districts feel the pinch most acutely because training centers cluster in urban areas. To bridge the gap, manufacturers such as Daikin opened large training campuses and rolled out mobile academies that travel to underserved regions.

Other drivers and restraints analyzed in the detailed report include:

- Smart HVAC and Building-Automation Retrofits

- Corporate Net-Zero Commitments Boosting Commercial Upgrades

- Supply-Chain Volatility for Key Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Germany HVAC market size for equipment stood at USD 3.21 billion in 2025, equal to 71.75% of total revenue. Heat pumps alone added more than 34% annual unit growth as consumers chased compliance and long-term savings. Boilers slipped 28% because gas options face an uncertain future under the Building Energy Act. Variable refrigerant flow systems won a greater share in offices and retail centers owing to zone-specific temperature control.

Service income recorded the highest trajectory at a 7.02% forecast CAGR. Complex commissioning, remote monitoring, and predictive maintenance drive spending that frequently exceeds original equipment cost over the life cycle. Energy-management projects in commercial buildings average EUR 45,000 to 65,000 (USD 48,000 to 69,000), roughly triple a standard preventive-maintenance contract. As heat-pump density grows, specialized leak testing and F-gas compliance checks become recurring revenue streams, further deepening the service dimension of the Germany HVAC market.

Complete Report Scope:

- By Component

- HVAC Equipment

- Heating Equipment

- Heat Pumps

- Boilers

- Radiators

- Cooling Equipment

- Air Conditioners

- Chillers

- Variable Refrigerant Flow Systems

- Ventilation Equipment

- Air Handling Units

- Energy Recovery Ventilators

- Heating Equipment

- HVAC Services

- Installation

- Maintenance and Repair

- Energy Management and Building Automation

- HVAC Equipment

- By End-User Industry

- Residential

- Commercial

- Industrial

- Public and Institutional

- By Implementation Type

- New Construction

- Retrofit

- By Region

- North

- South

- East

- West

- Central

List of Companies Covered in this Report:

- Carrier Corporation

- Robert Bosch GmbH

- Midea Group Co. Ltd

- Johnson Controls International PLC

- Daikin Industries Ltd

- Systemair AB

- LG Electronics Inc.

- Mitsubishi Electric Hydronics And IT Cooling Systems S.p.A.

- FlaktGroup Holding GmbH

- Danfoss A/S

- Vaillant Group

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH & Co. KG

- NIBE Industrier AB

- BDR Thermea Group B.V.

- Panasonic Holdings Corporation

- Trane Technologies plc

- Fujitsu General Limited

- Gree Electric Appliances Inc. of Zhuhai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Construction and Retrofit Activity to Aid Demand

- 4.2.2 Electrification Push via Building Energy Act (GEG) Targets

- 4.2.3 Rapid Uptake of Heat Pumps in New-Build Residential Segment

- 4.2.4 Growth of Smart HVAC and Building Automation Retrofits

- 4.2.5 Surge in Climate-Resilient Cooling Demand During Heatwaves

- 4.2.6 Corporate Net-Zero Commitments Boosting Commercial HVAC Upgrades

- 4.3 Market Restraints

- 4.3.1 High Initial Cost of Energy Efficient Systems

- 4.3.2 Shortage of Skilled HVAC Installers and Technicians

- 4.3.3 Policy Uncertainty Around Subsidy Continuity and GEG Timelines

- 4.3.4 Supply Chain Volatility for Key Components (Compressors, Electronics)

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 HVAC Equipment

- 5.1.1.1 Heating Equipment

- 5.1.1.1.1 Heat Pumps

- 5.1.1.1.2 Boilers

- 5.1.1.1.3 Radiators

- 5.1.1.2 Cooling Equipment

- 5.1.1.2.1 Air Conditioners

- 5.1.1.2.2 Chillers

- 5.1.1.2.3 Variable Refrigerant Flow Systems

- 5.1.1.3 Ventilation Equipment

- 5.1.1.3.1 Air Handling Units

- 5.1.1.3.2 Energy Recovery Ventilators

- 5.1.1.1 Heating Equipment

- 5.1.2 HVAC Services

- 5.1.2.1 Installation

- 5.1.2.2 Maintenance and Repair

- 5.1.2.3 Energy Management and Building Automation

- 5.1.1 HVAC Equipment

- 5.2 By End-User Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Public and Institutional

- 5.3 By Implementation Type

- 5.3.1 New Construction

- 5.3.2 Retrofit

- 5.4 By Region

- 5.4.1 North

- 5.4.2 South

- 5.4.3 East

- 5.4.4 West

- 5.4.5 Central

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Carrier Corporation

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Midea Group Co. Ltd

- 6.4.4 Johnson Controls International PLC

- 6.4.5 Daikin Industries Ltd

- 6.4.6 Systemair AB

- 6.4.7 LG Electronics Inc.

- 6.4.8 Mitsubishi Electric Hydronics And IT Cooling Systems S.p.A.

- 6.4.9 FlaktGroup Holding GmbH

- 6.4.10 Danfoss A/S

- 6.4.11 Vaillant Group

- 6.4.12 Viessmann Climate Solutions SE

- 6.4.13 Stiebel Eltron GmbH & Co. KG

- 6.4.14 NIBE Industrier AB

- 6.4.15 BDR Thermea Group B.V.

- 6.4.16 Panasonic Holdings Corporation

- 6.4.17 Trane Technologies plc

- 6.4.18 Fujitsu General Limited

- 6.4.19 Gree Electric Appliances Inc. of Zhuhai

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment