PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073664

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073664

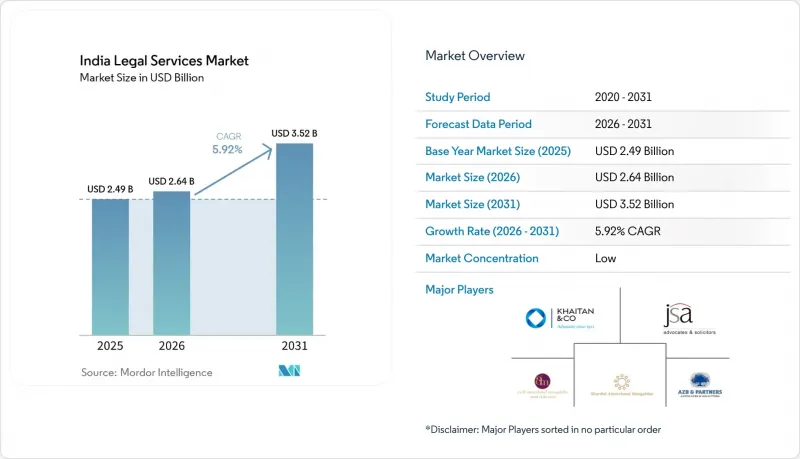

India Legal Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india legal services market size was valued at USD 2.49 billion in 2025 and estimated to grow from USD 2.64 billion in 2026 to reach USD 3.52 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

This report Segments the Industry Into by Client Type (Corporates, Small and Medium Enterprises (SMEs), and Other), by Application (Corporate, Financial, and Commercial Law, Real Estate and Property Law, and Other), by Service (Representation and Advocacy, Taxation Services, and Other), and by Geography (North India and Other). The Market Forecasts are Provided in Terms of Value (USD).

India Legal Services Market Trends and Insights

Corporate & M&A Boom Post-FDI Liberalization

India's inbound foreign direct investment (FDI) flows experienced significant growth in 2024, driven by policy reforms that removed sectoral caps in key industries such as insurance, defence, and single-brand retail. These regulatory changes have catalysed an increase in multi-jurisdictional transactions, which now demand comprehensive merger-control filings, meticulous tax structuring, and sector-specific regulatory approvals to ensure compliance and operational efficiency. Cross-border tie-ups, such as the proposed Honda-Nissan joint holding structure, require synchronized advice covering Press Note 3 compliance, indirect-transfer tax exposure, and global competition filings. Firms that field integrated teams across M&A, tax, and antitrust disciplines are best positioned to capture the rising pipeline. As foreign lawyers gain a limited foothold in arbitration and foreign-law advice, domestic firms are moving to cement referral partnerships and sector-focused desks to guard market share.

Digital-First Economy Fueling Compliance Work

India's rapid digitization, from UPI payments to on-demand services, is spawning ever-denser rules on data governance, platform liability, and algorithmic accountability. The Digital Personal Data Protection Act 2023, with detailed rules due in 2025, will obligate companies to overhaul consent workflows, breach-reporting procedures, and data-processing contracts . Revised Motor Vehicle Aggregator Guidelines further complicate compliance, as ride-sharing firms balance dynamic pricing freedom with driver-welfare metrics. Fintech regulations on digital lending and payment aggregation create continuous interpretive challenges that keep advisory pipelines full. Rather than shrinking legal spend, the uptake of AI contract-analysis tools is expanding it: enterprises retain counsel to vet training data, bias-mitigation protocols, and contractual risk allocation. Demand is therefore shifting from post-incident litigation toward preventive audits, template redesigns, and product-launch clearances.

Court Backlog & Slow Dispute Resolution

India's courts are grappling with more than 50 million pending cases, including 62,000 matters older than 30 years in the high courts, a logjam that depresses the effective value of litigation and prolongs receivables cycles for claimants. Supreme Court congestion-hovering near 80,000 cases-further pushes corporates toward arbitration and pre-institution mediation. While the Mediation Act 2023 and digitized filing systems offer incremental relief, chronic understaffing and infrastructure gaps in tier-2 cities remain. The resulting time-value erosion of claims curtails appetite for large contentious matters and shifts spend toward earlier-stage risk-mitigation reviews. Although ADR work partially offsets the lost litigation income, the negative net effect trims overall growth potential for the India legal services market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in ESG & Sustainability Mandates

- Rapid ALSP & Legal-Tech Adoption for Cost Control

- Regulatory Uncertainty on Foreign-Firm Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corporates accounted for 38.85% of India's legal services market share in 2025, reflecting their deep and recurring need for transaction support, regulatory filings, and sophisticated dispute management. SMEs are nonetheless projected to post a 11.94% CAGR, buoyed by mandatory GST registration, data-protection obligations, and mainstream ESG reporting that pull even smaller entities into the formal economy. Many mid-market companies are migrating from ad-hoc local counsel to structured retainers, prompting firms to craft tiered service packages and cloud-based subscription platforms. Individual clients continue to seek advice on property transfers, succession planning, and personal litigation, but fee sensitivity in this cohort caps revenue upside. Government and public-sector undertakings represent episodic opportunities tied to procurement cycles and infrastructure pushes, yet payment delays and rigid fee schedules temper profitability.

The divergence between stable corporate mandates and fast-growing SME work compels firms to balance bespoke partner-led teams with process-driven delivery pods. Corporate legal departments increasingly demand outcome-based pricing that pushes law firms to adopt project-management toolkits. In parallel, SMEs prefer fixed-fee compliance bundles, and AI-enabled document-generation platforms facilitate their rapid onboarding. Firms that can scale without diluting quality will capture the incremental volumes that SMEs bring to the India legal services market. Talent allocation is also evolving associates rotate between high-margin M&A deals and volume-driven SME compliance tasks, broadening skill sets while sustaining utilization rates.

Complete Report Scope:

- By Client Type

- Corporates

- Small and Medium Enterprises (SMEs)

- Individual Clients

- Government and Public Sector

- By Application

- Corporate, Financial, and Commercial Law

- Real Estate and Property Law

- Family and Personal Law

- Employment and Labor Law

- Criminal Law

- Intellectual Property and Technology Law

- Dispute Resolution and ADR

- Taxation and Regulatory Law

- By Service

- Representation and Advocacy

- Taxation Services

- Advisory and Consultancy

- Bankruptcy and Restructuring

- Notarial and Certification Services

- Legal Research and Documentation

- By Geography

- North India

- South India

- West India

- East India

- Central India

- North-East India

List of Companies Covered in this Report:

- Cyril Amarchand Mangaldas

- AZB & Partners

- Khaitan & Co.

- Shardul Amarchand Mangaldas & Co.

- JSA Advocates & Solicitors

- Trilegal

- Luthra & Luthra Law Offices India

- Saraf & Partners

- Nishith Desai Associates

- Lakshmikumaran & Sridharan

- Kochhar & Co.

- S&R Associates

- Dentons Link Legal

- Fox Mandal & Associates

- Anand & Anand

- Remfry & Sagar

- QuisLex (LPO)

- Pangea3 (LPO)

- SpotDraft (LegalTech)

- Icertis (ALSP)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Corporate & M&A boom post-FDI liberalisation

- 4.2.2 Digital-first economy fuelling compliance work

- 4.2.3 Surge in ESG & sustainability mandates

- 4.2.4 Rapid ALSP & legal-tech adoption for cost control

- 4.2.5 Third-party litigation funding gaining traction

- 4.2.6 India-seated cross-border arbitration momentum

- 4.3 Market Restraints

- 4.3.1 Court backlog & slow dispute resolution

- 4.3.2 Regulatory uncertainty on foreign-firm rules

- 4.3.3 Downward fee pressure from price-sensitive clients

- 4.3.4 Talent crunch in specialised practice areas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts

- 5.1 By Client Type

- 5.1.1 Corporates

- 5.1.2 Small and Medium Enterprises (SMEs)

- 5.1.3 Individual Clients

- 5.1.4 Government and Public Sector

- 5.2 By Application

- 5.2.1 Corporate, Financial, and Commercial Law

- 5.2.2 Real Estate and Property Law

- 5.2.3 Family and Personal Law

- 5.2.4 Employment and Labor Law

- 5.2.5 Criminal Law

- 5.2.6 Intellectual Property and Technology Law

- 5.2.7 Dispute Resolution and ADR

- 5.2.8 Taxation and Regulatory Law

- 5.3 By Service

- 5.3.1 Representation and Advocacy

- 5.3.2 Taxation Services

- 5.3.3 Advisory and Consultancy

- 5.3.4 Bankruptcy and Restructuring

- 5.3.5 Notarial and Certification Services

- 5.3.6 Legal Research and Documentation

- 5.4 By Geography

- 5.4.1 North India

- 5.4.2 South India

- 5.4.3 West India

- 5.4.4 East India

- 5.4.5 Central India

- 5.4.6 North-East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Cyril Amarchand Mangaldas

- 6.4.2 AZB & Partners

- 6.4.3 Khaitan & Co.

- 6.4.4 Shardul Amarchand Mangaldas & Co.

- 6.4.5 JSA Advocates & Solicitors

- 6.4.6 Trilegal

- 6.4.7 Luthra & Luthra Law Offices India

- 6.4.8 Saraf & Partners

- 6.4.9 Nishith Desai Associates

- 6.4.10 Lakshmikumaran & Sridharan

- 6.4.11 Kochhar & Co.

- 6.4.12 S&R Associates

- 6.4.13 Dentons Link Legal

- 6.4.14 Fox Mandal & Associates

- 6.4.15 Anand & Anand

- 6.4.16 Remfry & Sagar

- 6.4.17 QuisLex (LPO)

- 6.4.18 Pangea3 (LPO)

- 6.4.19 SpotDraft (LegalTech)

- 6.4.20 Icertis (ALSP)

7 Market Opportunities & Future Outlook

- 7.1 Rise of niche ESG-focused boutique practices

- 7.2 Explosive demand for AI-enabled contract lifecycle management