PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073667

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073667

Automated Blinds and Shades - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

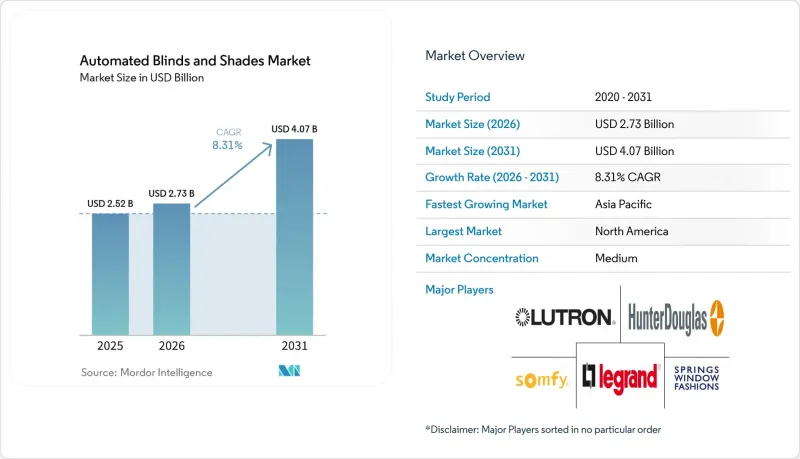

According to Mordor Intelligence, the global automated blinds and shades market size was valued at USD 2.52 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 4.07 billion by 2031, at a CAGR of 8.31% during the forecast period (2026-2031).

This report is Segmented by Product (Blinds (Venetian, Vertical, Roller, and More), Shades (Cellular, Roman, Pleated, and More)), Control Type (Motorized, Smart), End-Users (Residential, Commercial), Distribution Channel (B2C and B2B), and Geography (North America, Europe, Asia-Pacific, South America, and the Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Automated Blinds and Shades Market Trends and Insights

Energy-Efficiency Regulations on Glazing & Facades

The 2024 IECC trimmed allowable U-factors and mandated automatic daylight controls in commercial zones, channeling non-discretionary budgets toward intelligent shading hardware. Title 24 stipulates Net-Zero Energy performance in California residential construction, effectively guaranteeing automated daylight harvesting on every new build. Federal facilities must meet 10 CFR Part 434, a rule set expanded in 2025 to cover leased buildings, magnifying public-sector opportunity. In Europe, ASHRAE/IES 90.1-2022 underpins nine-percent site-energy cuts largely attributed to automated glare mitigation, and similar directives are surfacing in Asia-Pacific capitals. These codes decouple demand from macro construction cycles and protect the automated blinds and shades market against short-term real-estate slowdowns.

Cost Decline of IoT Motors & Batteries

Volume silicon production and refined motor winding processes have carved double-digit costs out of brushless DC drives since 2022. Lithium battery densification allows two-to-three-year service intervals, reducing homeowner maintenance anxiety. Somfy's Sonesse 40 PoE motor bypasses separate power wiring altogether, simplifying installation and trimming labor hours by up to 18%. Meanwhile, the CHIPS and Science Act is steering USD 39 billion into domestic fabs that will mitigate semiconductor shortages by 2027, smoothing component supply and preserving margin headroom for manufacturers in the automated blinds and shades market.

High Upfront Installation Cost

Hardware prices have fallen, yet a professional install still commands a 15-25% labor premium, making do-it-yourself aspirants think twice. Retrofit jobs in existing masonry often require conduit routing or battery replacements in inaccessible clerestory windows, pushing total invoices beyond comfort levels for cost-conscious buyers. Commercial budgets also face capital-allocation scrutiny when juxtaposing shading automation against HVAC upgrades. Utility rebates exist but remain patchy, with only 27 U.S. investor-owned utilities offering incentive programs in 2025. Until financing products normalize, cost friction will shave points off the automated blinds and shades market growth, particularly in emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Aging-In-Place Retrofits Demanding Touch-Free Shading

- Smart-Home Penetration Surge

- Inter-Brand Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blinds held 59.85% revenue in 2025, giving them the commanding height within the automated blinds and shades market. Venetian formats benefit from incremental slat-tilt motor design that offers fine lumen control, vital for open-plan offices pursuing glare-free laptop environments. Roller variants capitalize on minimalist aesthetics prized by modern architects, while vertical blinds remain indispensable for expansive glazing in convention centers. Over the forecast, wood and faux-wood models are expected to migrate to recycled composites, a shift that pairs sustainability credentials with resistance to warping.

Shades, advancing at a 8.98% CAGR, are pulling spend away from blinds in thermally demanding zones. Cellular (honeycomb) constructions can cut heat gain by up to 46%, a metric now embedded in many U.S. utility rebate calculators. Roman and pleated silhouettes dovetail with luxury residential interiors, prompting premium positioning by top brands. Manufacturers bundle these styles with ultra-quiet micro-motors that operate at sub-35 dB, satisfying noise-sensitive hospital patient rooms. Among specialty models, light-transmitting but opaque fabrics meet WELL Building Standard glare criteria, broadening shade appeal in commercial retrofits.

Motorized devices remain the mass-market workhorse, representing 69.90% of 2025 spend. They suit spec-grade apartment blocks that need reliable motion but not full cloud integration, and their installers value stable RS-485 or dry-contact wiring that aligns with existing building automation systems. Battery-powered versions particularly thrive in retrofit skylights where rewiring would breach vapor barriers.

Smart-enabled lines, rising at 10.72% CAGR, splice Wi-Fi, Thread, or Matter chips directly into the headrail. Facility managers accessing dashboards such as Somfy SDN Connect gain motor-health telemetry, which cuts downtime and service calls. Voice-assistant compatibility is now a table-stakes, with 78% of U.S. smart-speaker households having issued at least one shading command in 2024. Predictive algorithms tethered to weather forecasts adopt a pre-emptive stance, lowering shades ahead of afternoon heat spikes and trimming HVAC usage. This closed-loop automation underscores why connected products will keep enlarging their automated blinds and shades market footprint.

Complete Report Scope:

- By Product

- Blinds

- Venetian

- Vertical

- Roller

- Others

- Shades

- Cellular

- Roman

- Pleated

- Others

- Blinds

- By Control Type

- Motorized

- Smart

- By End-User

- Residential

- Commercial

- Hospitality

- Offices

- Healthcare

- Other Commercial End-Users

- By Distribution Channel

- B2C / Retail Channels

- Multi-Brand Stores

- Specialty Stores

- Online

- Other Distribution Channels

- B2B / Directly From Manufacturers

- B2C / Retail Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest Of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, And Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, And Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, And Philippines)

- Rest Of Asia-Pacific

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest Of Middle East And Africa

- North America

Geography Analysis

North America, holding 38.55% of 2025 revenue, sits at the intersection of mature smart-home adoption and the continent's tightest energy codes. California's Title 24 revision and Canada's National Energy Code for Buildings each force automated daylight control into mainstream building budgets. The United States additionally benefits from the Inflation Reduction Act tax credits that reimburse up to 30% of installed shading systems when part of a whole-home energy upgrade, cushioning payback concerns. Contractors, however, must navigate high union labor costs that can extend project ROI timelines.

Asia-Pacific is the growth pacesetter with a 9.18% CAGR, propelled by urban megaprojects in China and India, where curtain-wall facades dominate skylines. Beijing's dual-carbon target has birthed provincial incentives that cover 15% of intelligent facade costs, driving adoption among Grade-A office developers. India's Smart Cities Mission added daylight-responsive shades to its 2025 tender specifications, fortifying municipal demand. Japan registers high penetration in elder-care retrofits, and Southeast Asia's hospitality boom, especially in Singapore and Bangkok, pulls large lots of motorized drapery into four- and five-star hotels.

Europe enjoys steady replacement demand anchored in renovation waves funded by the EU's "Fit for 55" program. Germany leads with KfW low-interest loans that reward energy-efficient retrofits, while France's RE2020 building regulation tightens solar-heat-gain coefficients, nudging developers toward advanced shading. Nordic countries champion motorized blackout fabrics that mitigate extremes of midnight sun and polar night, whereas Mediterranean states emphasize reflective blinds to block peak-season insolation. Post-Brexit United Kingdom must juggle divergence from EU codes and alignment with net-zero commitments, yet premium consumer tastes keep average selling prices high.

- Hunter Douglas N.V.

- Automated Shading & Lighting Control Inc.

- Springs Window Fashions LLC

- Yoolax

- Somfy Systems S.A.

- SmartWings

- Lutron Electronics Co., Inc.

- Legrand S.A.

- Dooya Tubular Motor

- Griesser AG

- Behrens Group (Bali)

- Warema Renkhoff SE

- Mechoshade Systems LLC

- Coulisse B.V. (MotionBlinds)

- Draper Inc.

- Ching Feng Home Fashions Co. Ltd.

- Acmeda Pty Ltd

- Lafayette Venetian Blind Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart-Home Penetration Surge

- 4.2.2 Energy-Efficiency Regulations On Glazing & Facades

- 4.2.3 Cost Decline Of IoT Motors & Batteries

- 4.2.4 Aging-In-Place Retrofits Demanding Touch-Free Shading

- 4.2.5 Day-Light-Harvesting Mandates In Green-Building Codes

- 4.2.6 Hospitality Push For Contact-Free Guest Rooms Post-COVID

- 4.3 Market Restraints

- 4.3.1 High Upfront Installation Cost

- 4.3.2 Inter-Brand Interoperability Gaps

- 4.3.3 Cyber-Security & Data-Privacy Concerns

- 4.3.4 Motor & Chip Supply-Chain Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Suppliers

- 4.5.3 Bargaining Power Of Buyers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights Into The Latest Trends And Innovations In The Market

- 4.7 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.)

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Blinds

- 5.1.1.1 Venetian

- 5.1.1.2 Vertical

- 5.1.1.3 Roller

- 5.1.1.4 Others

- 5.1.2 Shades

- 5.1.2.1 Cellular

- 5.1.2.2 Roman

- 5.1.2.3 Pleated

- 5.1.2.4 Others

- 5.1.1 Blinds

- 5.2 By Control Type

- 5.2.1 Motorized

- 5.2.2 Smart

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality

- 5.3.2.2 Offices

- 5.3.2.3 Healthcare

- 5.3.2.4 Other Commercial End-Users

- 5.4 By Distribution Channel

- 5.4.1 B2C / Retail Channels

- 5.4.1.1 Multi-Brand Stores

- 5.4.1.2 Specialty Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B / Directly From Manufacturers

- 5.4.1 B2C / Retail Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest Of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, And Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, And Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, And Philippines)

- 5.5.4.7 Rest Of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest Of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share For Key Companies, Products & Services, And Recent Developments)

- 6.4.1 Hunter Douglas N.V.

- 6.4.2 Automated Shading & Lighting Control Inc.

- 6.4.3 Springs Window Fashions LLC

- 6.4.4 Yoolax

- 6.4.5 Somfy Systems S.A.

- 6.4.6 SmartWings

- 6.4.7 Lutron Electronics Co., Inc.

- 6.4.8 Legrand S.A.

- 6.4.9 Dooya Tubular Motor

- 6.4.10 Griesser AG

- 6.4.11 Behrens Group (Bali)

- 6.4.12 Warema Renkhoff SE

- 6.4.13 Mechoshade Systems LLC

- 6.4.14 Coulisse B.V. (MotionBlinds)

- 6.4.15 Draper Inc.

- 6.4.16 Ching Feng Home Fashions Co. Ltd.

- 6.4.17 Acmeda Pty Ltd

- 6.4.18 Lafayette Venetian Blind Inc.

7 Market Opportunities & Future Outlook

- 7.1 Growing Demand for Smart Home Integration