PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686203

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686203

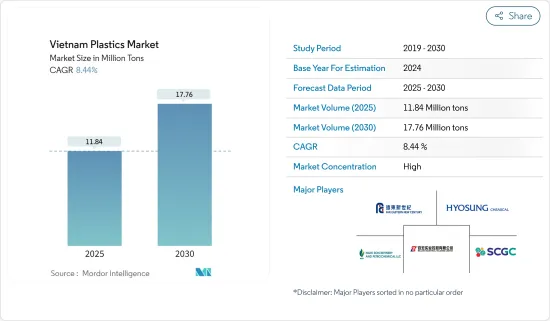

Vietnam Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Vietnam Plastics Market size is estimated at 11.84 million tons in 2025, and is expected to reach 17.76 million tons by 2030, at a CAGR of 8.44% during the forecast period (2025-2030).

The COVID-19 pandemic affected the Vietnamese market negatively. However, with the resumption of work in major end-user industries, the market is estimated to have reached pre-pandemic levels.

Key Highlights

- In the short term, the increasing demand from the construction industry is expected to drive market growth.

- Over-reliance on imports of raw materials and finished plastics is expected to hinder the growth of the market.

- An increase in foreign investments is expected to offer various opportunities for the growth of the market.

Vietnam Plastic Market Trends

Extrusion Technology to Dominate the Market

- In Vietnam, extrusion molding technology is used to make products such as PVC, PE pipe, aluminum and plastic pipe, fiber, PVC doors, frames, roofings, and wall coverings. An extrusion molding process involves lower production costs and faster setup time. However, it provides mediocre precision and is mostly suitable for uniform cross-section parts and not complex parts.

- This technology is used mainly in construction activities, and the main products include PVC, HDPE, PPR pipes, profile bars, plastic doors and windows, panels, and furniture.

- According to the plastic industry development plan of 2020, the plastics industry will be restructured toward reducing the proportion of packaging and consumer plastics and increasing the percentage of the construction and technical plastics segment.

- Vietnam's construction plastics segment accounts for around one-fourth of the total plastics industry. Developing the construction and real estate sector is boosting the demand for plastic construction products.

- In addition, the country's government aims to build a million affordable houses in more than 350 industrial zones. These infrastructural development projects and the increasing number of factories being installed are robustly increasing the demand for construction and technical plastics in the country.

- In April 2022, one of the top PET packaging businesses in Vietnam, Ngoc Nghia Industry - Service - Trading Joint Stock Company (NN), was acquired by Indorama Ventures Public Company Limited (IVL), a global sustainable chemical company. The acquisition will strengthen IVL's market position as it broadens its integrated PET product offering to significant multinational customers throughout the country.

- In September 2022, the US-based beverage company The Coca-Cola Company introduced fully recycled plastic bottles in Vietnam. The company claims to meet both Vietnamese regulations and international standards for food-grade rPET packaging.

- Based on the aforementioned aspects, extrusion technology is expected to dominate the market.

Packaging Segment to Dominate the Market

- Packaging accounts for the largest share of the Vietnamese plastics market. Factors like light weight and thermal, chemical, and corrosion resistance make plastics a viable choice for packaging purposes in the Vietnamese market.

- In the packaging industry, plastics are used for healthcare packaging, food and beverage packaging, consumer packaged goods, consumer and personal care packaging, and in the home and garden.

- Polyethylene terephthalate (PET) is one of the majorly used plastics for packaging purposes, mostly in the food and beverage industry. Portability, design flexibility, ease of cleaning, light weight, and protection against moisture are a few properties of PET that make them suitable for packaging purposes.

- In addition, low handling hazards, low toxicity, absence of Bisphenol A (BPA), and heavy metals favor the PET market for the food packaging industry.

- With a growth rate of 15% to 20% in the upcoming years, the packaging industry is one of Vietnam's fastest-growing sectors. Over 900 factories are currently in operation in the sector, with approximately 70% of them located in the Southern region, primarily in Ho Chi Minh City, Binh Duong, and Dong Nai.

- In March 2022, Tetra Pak, a well-known F&B company, with an additional USD 5.9 million investment into its USD 141.2 million packaging material factory in the province of Binh Duong, proved its confidence in Vietnam. To meet the growing demand for aseptic packages in Vietnam and other regional markets, the additional investment will increase the factory's annual output from the current 11.5 billion to 16.5 billion packages.

- Thus, based on the aforementioned aspects, the packaging segment is expected to dominate the market.

Vietnam Plastic Industry Overview

The Vietnamese plastics market is a consolidated market with a limited number of players engaged in the production of plastic resins. Some of the key players in the market include Far Eastern New Century, Nghi Son Refinery and Petrochemical (NSRP), Hyosung Chemicals, Billion Industrial Holdings Limited, and SCG Chemicals Public Company Limited (TPC VINA), among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Construction Sector

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Over-reliance on Imports of Raw Materials and Finished Plastics

- 4.2.2 Environmental Concerns of Plastics and the Availability of New Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene

- 5.1.1.2 Polypropylene

- 5.1.1.3 Polystyrene

- 5.1.1.4 Polyvinyl Chloride

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyurethanes

- 5.1.2.2 Fluoropolymers

- 5.1.2.3 Polyamides

- 5.1.2.4 Polycarbonates

- 5.1.2.5 Styrene Copolymers (ABS and SAN)

- 5.1.2.6 Thermoplastic Polyesters

- 5.1.2.7 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 Technology

- 5.2.1 Blow Molding

- 5.2.2 Extrusion

- 5.2.3 Injection Molding

- 5.2.4 Other Technologies

- 5.3 Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Housewares

- 5.3.6 Furniture and Bedding

- 5.3.7 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Agc Inc.

- 6.4.2 Billion Industrial Holdings Limited

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 Hyosung Chemical

- 6.4.5 Lyondellbasell Industries Holdings Bv

- 6.4.6 Nan Ya Plastics Corporation

- 6.4.7 Nsrp Llc

- 6.4.8 Scg Chemicals Public Company Limited

- 6.4.9 Toray Industries Inc.

- 6.4.10 Vietnam Oil And Gas Group

- 6.4.11 Vietnam Polystyrene Co. Ltd

- 6.4.12 Vinaplast

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Foreign Investments

- 7.2 Other Opportunities