Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640404

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640404

Anti-Corrosion Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

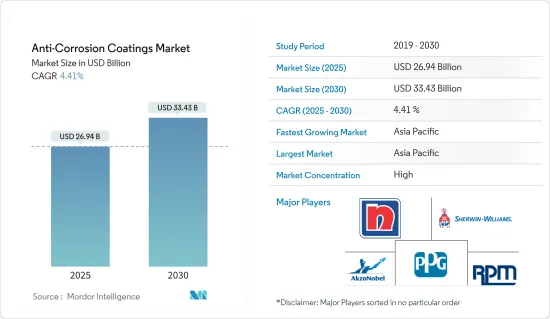

The Anti-Corrosion Coatings Market size is estimated at USD 26.94 billion in 2025, and is expected to reach USD 33.43 billion by 2030, at a CAGR of 4.41% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic had a negative impact on the anti-corrosion coatings sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business has been recovering since 2021 and is expected to rise significantly in the coming years.

- Major factors driving the market are significant growth in the infrastructure industry, an increase in demand from the marine industry, and expansion of oil and gas activities in Asia-Pacific and North America.

- Regulations related to volatile organic compounds (VOCs) and is expected to hinder the growth of the market studied.

- Significant investments in the infrastructure industry in emerging economies and increased adoption of water-borne coatings are expected to provide remarkable growth opportunities in the anti-corrosion coatings market in the future.

- Asia-Pacific region is expected to dominate the anti-corrosion coatings markets due to the increase in investments in various end-user industries in the region during the forecast period.

Anti-Corrosion Coatings Market Trends

Increasing Demand from the Infrastructure Industry

- The infrastructure segment accounts for the largest share of the market and is also estimated to be the fastest-growing segment. Rails, bridges, and roads contributed as the major segments of the infrastructure. The rapid increase in population and growth in infrastructure projects are expected to boost the demand for anti-corrosion coatings.

- There are various small-scale projects spread across Asia-Pacific and North America. Apart from being the most populous nation in the world, China also has the largest number of railroad passengers.

- Moreover, road projects in Asia-pacific are also expected to increase the consumption of anti-corrosion coatings. For instance, according to the Ministry of Road Transport and Highways, the ongoing Bharatmala Pariyojna is developing around 26,000 km length of Economic Corridors in order to carry most of the freight traffic on roads. The improvement of Economic Corridors, GQ, and NS-EW Corridoors has been done by building 8.000 km of Inter Corridors and 7,500 km of Feeder Routes.

- For infrastructure development, according to China Briefings, At the end of 2021, China's Ministry of Finance (MoF) pre-allocated USD 229.6 billion of the 2022 quota to be used in the first quarter in the hopes that the extra liquidity would spur investment at the beginning of the year, with higher quotas allocated to provinces and regions with higher capital needs.

- In April 2023, World Bank data stated that private participation in infrastructure (PPI) reached around USD 91.7 billion with around 263 projects, which accounts for 23% growth from 2021. It is observed in low and middle-income countries, the investment in infrastructure has rebounded in 2022.

- According to the US Department of Transportation (USDoT) and Federal Highway Administration (FHWA), in the years 2022 and 2030, around USD 120 billion has been allocated for highways and bridges, of which nearly 2,800 bridges have already been launched. USDOT invested USD 2.2 billion for 166 projects in Rebuilding American Infrastructure with Sustainability and Equity (RAISE) grants. It will facilitate the modernization of rail, ports, roads, bridges, and intermodal transportation to be more affordable, safer, and sustainable.

- The aforementioned factors are expected to increase the demand for anti-corrosion coatings in the forecast period.

Asia-Pacific Region to Dominate the Market

- In Asia-Pacific, though China, Japan, and South Korea lead the shipbuilding industry, new shipping hubs are appearing in Vietnam, India, and the Philippines.

- Australia and New Zealand are both island nations, and the geographical scale of Australia's coastline and waterways has resulted in a large number of recreational, commercial, and defense vessels.

- China is the leading importer and exporter of crude oil in the world. Thus, any changes affecting the expansion activities related to the oil and gas sector are likely to have a significant impact on the anti-corrosion coatings market in China.

- According to US Energy Information Administration, in 2022, China has prioritized low-carbon and carbon-neutral initiatives in order to meet the country's 2030 and 2060 climate targets of peak carbon emissions and carbon neutrality, respectively. The plan has set a goal for natural gas annual production to increase to 8.1 trillion cubic feet (Tcf) and installed generation capacity to increase to 3.0 terawatts (TW).

- Anti-corrosion coatings also play a significant role in infrastructure applications and global development, and an increase in investment in infrastructure is boosting the demand for anti-corrosion coatings. According to the Asian Development Bank (ADB), if Asia- Pacific has to maintain its growth momentum, respond to climate change, and remove poverty, then the region has to invest USD 1.7 trillion per year by 2030 in infrastructure development.

- Thus, the above-mentioned factors are expected to drive the anti-corrosion coatings market in the forecast period.

Anti-Corrosion Coatings Industry Overview

The anti-corrosion coatings market is consolidated and the major companies include PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., and the Sherwin-Williams Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 52574

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Significant Growth in the Infrastructure Industry

- 4.1.2 Increase in Demand from the Marine Industry

- 4.1.3 Expansion of Oil and Gas Activities in Asia-Pacific and North America

- 4.2 Restraints

- 4.2.1 Government Regulations Related to Volatile Organic Compounds (VOCs)

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Alkyds

- 5.1.3 Polyester

- 5.1.4 Polyurethane

- 5.1.5 Vinyl Ester

- 5.1.6 Other Resin Types

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder

- 5.2.4 UV-cured

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Marine

- 5.3.3 Power

- 5.3.4 Infrastructure

- 5.3.5 Industrial

- 5.3.6 Aerospace and Defense

- 5.3.7 Transportation

- 5.3.8 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East & Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems, LLC

- 6.4.3 BASF SE

- 6.4.4 H.B. Fuller Company

- 6.4.5 Hempel A/S

- 6.4.6 Jotun

- 6.4.7 Kansai Paint Co.,Ltd

- 6.4.8 Nippon Paint Holdings Co., Ltd.

- 6.4.9 PPG Industries, Inc.

- 6.4.10 RPM International Inc.

- 6.4.11 Sika AG

- 6.4.12 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Significant Investments in the Infrastructure Industry in the Emerging Economies

- 7.2 Increased Adoption of Water-borne Coatings

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.