Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685934

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685934

France Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 296 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

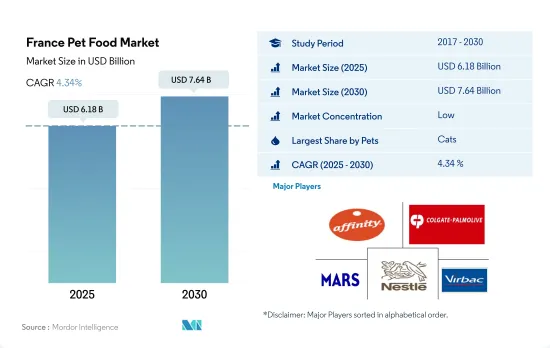

The France Pet Food Market size is estimated at 6.18 billion USD in 2025, and is expected to reach 7.64 billion USD by 2030, growing at a CAGR of 4.34% during the forecast period (2025-2030).

An increase in the pet population and growing demand for premium pet food products are driving the pet food market in France

- Cats held the largest market share in France's pet food market in 2022, valued at USD 2.7 billion. This can be attributed to the high population of cats in the country, which accounted for 40.7% (15.6 million) of the pet population.

- In 2022, dogs had the second-largest market share in France's pet food market, with a value of USD 1.8 billion. The trend of pet humanization has resulted in an increasing demand for premium pet food options, including grain-free and organic dog food. This trend is anticipated to drive the growth of the dog food market at a CAGR of 4.0% during the forecast period, making it one of the fastest-growing segments in the French pet food market.

- Other pets, such as birds, fish, reptiles, and rodents, account for 39.4% of the pet population in France. However, they accounted for 20% of the total pet food market value in 2022. This lower market share was attributed to the smaller size of these pets and their specific dietary requirements, resulting in lower food consumption than dogs and cats.

- The COVID-19 pandemic also contributed to increased pet ownership in France, leading to a higher demand for pet food. The growing awareness of the importance of pet health and nutrition has fueled the demand for specialized diets, organic pet foods, and treats. The French pet food market is anticipated to expand during the forecast period, driven by factors such as the rising number of pets (for instance, the pet population increased from 32.8 million in 2017 to 38.4 million in 2022), increased pet ownership, focus on pet health, and the introduction of new products that meet the changing needs of pet owners.

France Pet Food Market Trends

Cats can stay alone and require less maintenance, driving their adoption in the country

- In France, cats were the major pets adopted by pet parents, accounting for 40.6% of the pet population in 2022. The high adoption of cats is because cats are usually more adaptable to smaller living spaces than dogs and can be kept indoors without feeling cooped up. Additionally, cats are more highly regarded than dogs and are considered symbols of good luck or fortune.

- The higher number of cat parents is anticipated to help in the growth of the market for cat food in the country. The population of cats increased by 6.3% between 2019 and 2021. In 2021, there was a high adoption of cats by pet parents in the country; cat owners accounted for 31% of the population, whereas dog owners accounted for 25%. Furthermore, there was a rise in the pet population during the pandemic, and the cat population increased by 3.3% between 2020 and 2022. People adopted more cats during the pandemic to have a companion at home to avoid loneliness. Cats are quieter than dogs and easier to handle, which was helpful during lockdowns in home settings.

- There is less demand for services such as pet walking and pet boarding in the country than in the United States, as French pet parents usually work close to their homes to have lunch with their pets, including cats, and care for them on their own. The government also treats pets, including cats, as citizens because pet parents must have passports for their cats to travel with them.

- The increase in pet humanization, adaptability to smaller living spaces, and ability to be kept indoors are the factors anticipated to help in the growth of the cat population and the pet food market in the country.

The increasing usage of premium pet food has been enhancing the expenditure per pet in the country

- France is one of the major pet food markets in the European Union. There is an increasing trend in the overall pet expenditure in the country. The pet food expenditure increased by about 15.3% between 2019 and 2022. This surge in spending can be attributed to the growing trend of pet humanization and an expanding pet population nationwide. For instance, households owning cats increased from 8.5 million in 2016 to 8.9 million in 2020.

- Between 2019 and 2022, pet owners' annual spending on pet food for dogs increased by around 22.4%, while spending on cats increased by about 22.3%, and other pets saw an increase of about 9.0%. Sales of dog pet food recorded a CAGR of 1.5% from 2016 to 2020, while cat food sales recorded a CAGR of 2.5%. These findings may suggest an increasing trend in overall pet expenditure within the country.

- Pet owners in France are increasingly focused on the health and wellness of their pets. This has led to a rise in demand for natural and target-specific nutrition pet food products. This trend increased demand for premium pet brands such as "Royal Canine," which recorded increased retail sales from 188.5 million in 2016 to 305.6 million in 2022, registering a CAGR of 4.9%.

- The political conflict between Russia and Ukraine in 2022 has affected pet food prices in France. This conflict impacted the procurement of raw materials and subsequently affected pet expenditure in the country. However, the increasing preference for high-quality and premium pet food and the growing awareness of its benefits are anticipated to sustain the growth of pet expenditure during the forecast period.

France Pet Food Industry Overview

The France Pet Food Market is fragmented, with the top five companies occupying 31.42%. The major players in this market are Affinity Petcare SA, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated, Nestle (Purina) and Virbac (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 49552

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Alltech

- 6.4.4 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.5 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.6 General Mills Inc.

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.