PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907241

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907241

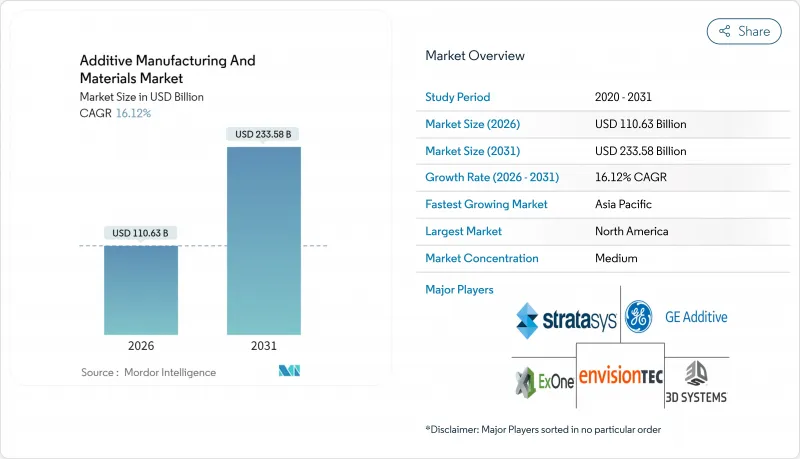

Additive Manufacturing And Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The additive manufacturing and materials market is expected to grow from USD 95.27 billion in 2025 to USD 110.63 billion in 2026 and is forecast to reach USD 233.58 billion by 2031 at 16.12% CAGR over 2026-2031.

Falling material prices, aerospace demand for lightweight parts, and rapid healthcare adoption shift the additive manufacturing and materials market away from prototyping and into volume production. Standardization programs at NIST and ASTM provide unified qualification pathways that lower certification costs, while government incentives in North America, Europe, and Asia Pacific accelerate factory-level deployment.Competitive intensity rises as vendors integrate software, printers, and qualified powders to deliver turnkey production lines that meet industrial uptime requirements. Simultaneously, circular-economy policies motivate producers to qualify recycled polymer and metal feedstocks, creating cost and sustainability advantages for regions with established waste-processing capacity. Space agencies validate in-orbit metal printing, opening a long-term frontier for on-site micro-production that removes costly launch mass.

Global Additive Manufacturing And Materials Market Trends and Insights

Demand for lightweight components in automotive and aerospace

Aerospace OEMs condense multi-part assemblies into single printed geometries to trim aircraft weight and maintenance. GE Aviation's printed fuel nozzle replaces twenty components and saves carriers USD 1.6 million in lifetime operating costs per aircraft.Boeing integrates titanium lattice brackets on the 787 that cut part cost by USD 2-3 million while meeting structural standards. Automotive firms replicate this consolidation in battery housings and brake systems to extend electric-vehicle range. Topology-optimization software unlocks organic shapes unattainable with machining, giving early adopters a performance edge. ASTM F2792 definitions standardize terminology and testing, helping certifiers approve flight-critical parts faster.

Rapid adoption of patient-specific healthcare implants

Powder-bed fusion enables porous titanium implants that match individual anatomy, improving osseointegration and cutting failure rates. Stryker has produced over 2 million such devices, proving the scalability of hospital-grade additive workflows.The U.S. FDA's point-of-care guidance lets certified hospitals print surgical guides onsite, reducing lead times and inventory costs. Distributed production shifts value from centralized factories to clinical settings, shrinking logistics footprints. Premium demand pushes cobalt-chrome and titanium powder suppliers to scale atomization capacity despite tight aerospace allocation.

High cost of high-performance metals and polymers

PEEK, PEKK, and aerospace-grade titanium powders trade at premiums that smaller job shops struggle to absorb. Limited atomizer capacity and energy-intensive plasma processes elevate raw-material costs just as buyers push for volume pricing. Suppliers face a squeeze between customers requesting discounts and investors demanding R&D spending, delaying next-generation material rollouts. Automotive and consumer sectors therefore confine purchases to prototypes or high-margin components until cost curves fall.

Other drivers and restraints analyzed in the detailed report include:

- Government funding and standards harmonization

- Supply-chain volatility in critical alloying elements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Directed Energy Deposition posts a 16.98% CAGR, underpinned by aerospace engine repair where meter-scale parts eclipse powder-bed build volumes. This segment benefits from wire feedstock that costs 30-50% less than powder and recoups material unused in other systems. Fused Deposition Modeling, however, retains 39.68% additive manufacturing and materials market share due to its ubiquity in education, design, and low-stress industrial fixtures. Hybrid CNC-additive platforms merge laser cladding with five-axis milling to meet tolerance and surface roughness targets in a single setup.

Powder Bed Fusion remains the benchmark for lattice-rich implants and rocket turbopump components requiring sub-80 µm layer heights. Binder Jetting evolves for steel pump housings and sand casting molds, offering throughput advantages when sintering bottlenecks are solved. Emerging microwave volumetric systems promise order-of-magnitude speed gains, foreshadowing a future where build time no longer dictates unit economics.

The Additive Manufacturing and Materials Market Report is Segmented by Technology (Polymer-Based, Metal-Based, Ceramic-Based, and More), Material Type (Polymers, Metals, Ceramics, Composite, and More), End User (Aerospace and Defense, Automotive, Healthcare, Industrial Machinery, Consumer Products, Construction, Education and Research, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commands 36.45% additive manufacturing and materials market size in 2025, supported by defense budgets, NASA deep-space initiatives, and a mature supplier ecosystem. Federal tax incentives and Section 174 R&D expensing rules reward capital investment in new production lines. FDA 510(k) guidance for 3D-printed implants accelerates time-to-market for device OEMs, reinforcing domestic powder consumption.

Asia Pacific is the fastest-growing region at a 16.55% CAGR as China funds domestic printer champions to lessen dependence on imported engine parts. Singapore's National Additive Manufacturing cluster certifies aerospace alloys and trains technicians, turning the island into a regional export hub.India's Production-Linked Incentive program subsidizes metal-printer purchases for automotive and energy verticals, while Australia's Cooperative Research Centre advances titanium powder atomization from local ore.

Europe focuses on sustainability; the EU's Fit-for-55 package spurs OEMs to print lightweight brackets that reduce vehicle emissions. The European Space Agency demonstrates the first stainless-steel part fabricated aboard the ISS, validating micro-gravity printing for lunar infrastructure. German carmakers co-develop aluminum-silicon alloys that weld seamlessly without hot-crack defects, setting a benchmark for crash-relevant applications.

- BASF 3D Printing Solutions GmbH

- Evonik Industries AG

- Arkema S.A.

- Sandvik AB

- Hoganas AB

- Stratasys Ltd.

- 3D Systems Corporation

- General Electric Company (GE Additive)

- EOS GmbH

- Materialise NV

- Desktop Metal Inc.

- Markforged Holding Corporation

- Carpenter Technology Corporation

- Heraeus Holding GmbH

- GKN Powder Metallurgy Holdings GmbH

- HP Inc.

- Prodways Group SA

- SLM Solutions Group AG

- Henkel AG and Co. KGaA

- DSM-Covestro Additive Manufacturing (Covestro AG)

- ExOne Company (Desktop Metal)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for lightweight components in automotive and aerospace

- 4.2.2 Rapid adoption of patient-specific healthcare implants

- 4.2.3 Falling polymer and metal powder prices

- 4.2.4 Government funding and standards harmonisation

- 4.2.5 Circular-economy push for recycled feedstocks

- 4.2.6 On-site micro-production for space and remote missions

- 4.3 Market Restraints

- 4.3.1 High cost of high-performance metals and polymers

- 4.3.2 Intellectual-property protection concerns

- 4.3.3 Stringent EHS rules for nano-powder handling

- 4.3.4 Supply-chain volatility in critical alloying elements

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Polymer-based Technologies

- 5.1.1.1 Fused Deposition Modeling (FDM)

- 5.1.1.2 Stereolithography (SLA)

- 5.1.1.3 Digital Light Processing (DLP)

- 5.1.1.4 Material Jetting (PolyJet)

- 5.1.1.5 Binder Jetting - Polymers

- 5.1.2 Metal-based Technologies

- 5.1.2.1 Powder Bed Fusion (SLM, EBM)

- 5.1.2.2 Directed Energy Deposition

- 5.1.3 Ceramic-based Technologies

- 5.1.3.1 Ceramic SLA

- 5.1.3.2 Ceramic Binder Jetting

- 5.1.4 Other Technologies

- 5.1.1 Polymer-based Technologies

- 5.2 By Material Type

- 5.2.1 Polymers

- 5.2.1.1 Commodity Thermoplastics (ABS, PLA)

- 5.2.1.2 Engineering Plastics (PA, PEEK)

- 5.2.1.3 Photopolymer Resins

- 5.2.1.4 High-performance Thermoplastics (ULTEM, PEKK)

- 5.2.2 Metals

- 5.2.2.1 Titanium Alloys

- 5.2.2.2 Aluminum Alloys

- 5.2.2.3 Stainless Steels

- 5.2.2.4 Nickel Super-alloys

- 5.2.2.5 Precious Metals

- 5.2.3 Ceramics

- 5.2.3.1 Alumina

- 5.2.3.2 Zirconia

- 5.2.3.3 Silicon Carbide

- 5.2.4 Composite and Other Emerging Material Feedstocks

- 5.2.1 Polymers

- 5.3 By End User

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Healthcare

- 5.3.3.1 Medical Devices

- 5.3.3.2 Dental

- 5.3.4 Industrial Machinery

- 5.3.5 Consumer Products

- 5.3.6 Construction

- 5.3.7 Education and Research

- 5.3.8 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Southeast Asia

- 5.4.4.7 Rest of Asia Pacific

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Egypt

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF 3D Printing Solutions GmbH

- 6.4.2 Evonik Industries AG

- 6.4.3 Arkema S.A.

- 6.4.4 Sandvik AB

- 6.4.5 Hoganas AB

- 6.4.6 Stratasys Ltd.

- 6.4.7 3D Systems Corporation

- 6.4.8 General Electric Company (GE Additive)

- 6.4.9 EOS GmbH

- 6.4.10 Materialise NV

- 6.4.11 Desktop Metal Inc.

- 6.4.12 Markforged Holding Corporation

- 6.4.13 Carpenter Technology Corporation

- 6.4.14 Heraeus Holding GmbH

- 6.4.15 GKN Powder Metallurgy Holdings GmbH

- 6.4.16 HP Inc.

- 6.4.17 Prodways Group SA

- 6.4.18 SLM Solutions Group AG

- 6.4.19 Henkel AG and Co. KGaA

- 6.4.20 DSM-Covestro Additive Manufacturing (Covestro AG)

- 6.4.21 ExOne Company (Desktop Metal)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment