Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693451

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693451

Tomato Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 465 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

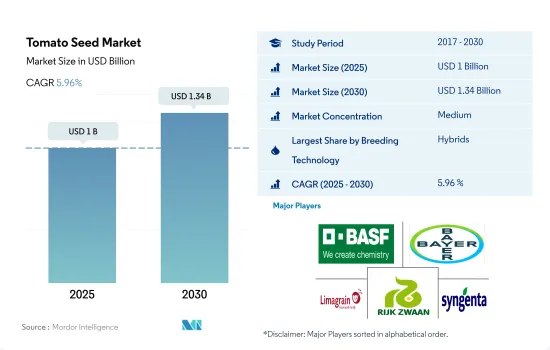

The Tomato Seed Market size is estimated at 1 billion USD in 2025, and is expected to reach 1.34 billion USD by 2030, growing at a CAGR of 5.96% during the forecast period (2025-2030).

Hybrids dominated the market due to the higher yield and disease resistance traits

- Tomato is one of the major vegetable crops cultivated globally. It accounted for 12.4% of the global vegetable seed market in 2022 as a result of the demand for tomatoes in processing and fresh consumption.

- In 2022, open pollinated varieties and hybrid derivatives accounted for 27.2% of the global tomato seed market. This is expected to increase due to the increase in organic cultivation and preference for native varieties.

- Asia-Pacific was the largest region for the cultivation of tomatoes by using open pollinated varieties and hybrid derivatives, accounting for 58.3% in 2022. This is a result of an increase in the usage of open pollinated varieties in developing countries and the preference for their taste and quality over hybrids.

- The hybrid segment accounted for 72.8% of the global tomato seed market, and it is growing at a faster rate compared to OPVs due to the increase in consumption and demand from processing industries. The usage of hybrids, which have higher adaptability, is also increasing in the protected structures.

- Asia-Pacific had the largest share of the global hybrid tomato seed market, and it accounted for about 43% in 2022 because of the new advanced technologies available in the region. China is a global leader in protected cultivation, and only hybrid seeds can be used for protected cultivation.

- Major companies, such as Syngenta, Bayer AG, and Rijk Zawann, are developing new hybrids with disease-resistant traits, increasing shelf life, wider adaptability, high yield, strong stem, crack resistance, and high vigor. The increase in organic cultivation and fresh segment consumption is also expected to drive the open pollinated varieties tomato seed market during the forecast period.

Asia-Pacific is the major market for tomato seeds due to high area under cultivation and the adoption of protected cultivation

- Tomato is the most popular vegetable globally, with an overall production of around 189.1 million metric ton in 2021. It represented around 16.4% of the global vegetable production. In 2022, the tomato seeds market accounted for 12.4% of the global vegetable seed market, which is considered to be one of the largest vegetable seed markets in the world. This is associated with tomatoes being the most consumed vegetable in various preparations.

- In 2022, Asia-Pacific was the largest tomato seed market, accounting for 47.3% of the global tomato seed market. It is expected to grow further due to the increase in consumption and market value in the domestic and international markets. In the region, China was the largest country in the tomato seed market, accounting for 23.5% of the global tomato seed market in 2022. With the increase in hybrid availability, most of the tomatoes are grown in greenhouses, which accounted for more than 50% of China's total tomato production in 2022.

- North America is the second-largest region in the tomato seed market, accounting for 21.4% of the global tomato seed market in 2022. The United States is the largest consumer of tomatoes globally.

- With the increased usage of hybrids in the production of tomatoes worldwide, the demand for hybrid tomato seeds increased. In 2022, hybrid seeds accounted for 72.7% of the global tomato seed market.

- An increase in protected cultivation acreage in major producing countries and an increase in the demand from processing industries and for consumption are anticipated to drive the global tomato seed market, registering a CAGR of 6.1% during the forecast period.

Global Tomato Seed Market Trends

The increase in demand for tomatoes from various industries and the growing consumption are driving the tomato cultivation area

- Tomato is one of the major vegetable crops cultivated and consumed globally. The overall area under cultivation of tomatoes increased by 8.0% between 2017 and 2022. This increase is mainly attributed to the growing demand from the various food processing industries and increasing consumption worldwide.

- Asia-Pacific holds the largest area under tomato cultivation with 2.6 million ha, accounting for about 47.1% of the global tomato acreage in 2022. China and India were the top countries with major tomato-cultivated areas in the region, with 1.1 million and 0.8 million ha, respectively, in 2022. China and India are the world's top countries in tomato production, and they have huge domestic and export demand. Africa is the second-largest region, accounting for 28.7% area of the world's tomato acreage in 2022. In Africa, the cultivated area increased by 14.5% between 2017 and 2022. Nigeria accounted for 54.8% of the total tomato acreage in the region in 2022 due to higher demand in the country.

- In 2022, Europe held 10.6% of the global tomato acreage. Turkey is the largest country, with 28.2% of the total European tomato acreage in the same year. Turkey is one of the largest producers of tomatoes in the world. Moreover, North America accounted for 4.1% of the world's tomato acreage in 2022. The United States is the major country, which held about 49.4% of the region's tomato area in the same year. South America accounted for 2.2% of the world's tomato acreage in 2022. Brazil alone held more than 42% of the total tomato acreage in the region during the same year. The increase in demand for tomatoes from various industries is anticipated to drive tomato acreage globally during the forecast period.

The expanding tomato seed market is driven by the increasing demand for disease-resistant and widely adaptable seed varieties

- Tomato is one of the largest segments of vegetables because of the high-value crop and high demand by processing industries for tomato puree, ketchup, and others. Major companies, such as Syngenta, Rijk Zwaan, and Enza Zaden, have more than 40% tomato seed varieties available globally that are resistant to viral diseases such as the leaf curl virus.

- Traits with resistance to viral diseases such as tomato mosaic virus, tomato yellow leaf curl virus, blossom end rot, powdery mildew, wilt diseases, and nematodes are popularly used for cultivation. Asia-Pacific is one of the largest tomato-producing regions, and major companies such as Rijk Zwaan, East-West Seed, and Namdhari Seeds have tomato seed varieties in the region that are resistant to viral diseases such as leaf curl virus. For instance, in 2022, Rijk Zwaan launched new tomato seed varieties resistant to the Tomato Brown Rugose Fruit Virus (ToBRFV). Moreover, in 2022, HM. Clause, a business unit of Limagrain, introduced a tomato variety that is resistant to the highly transmissible ToBRFV.

- Tomato varieties with extended shelf life, uniformity, cracking tolerance, and wider adaptability to different soils and climatic conditions are in high demand. Companies such as Bayer, Syngenta, and Rijk Zwaan offer seed varieties such as Kierano, Aurea, Angelle, Tontolle, and Cheramy RZ F1 to produce high-quality tomatoes in different agro conditions.

- The introduction of new hybrid seed varieties by companies with higher resistance to viruses, adaptability to different weather conditions, and high demand by processing industries are the factors expected to help in the growth of the tomato seed market during the forecast period.

Tomato Seed Industry Overview

The Tomato Seed Market is moderately consolidated, with the top five companies occupying 57.41%. The major players in this market are BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92513

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Breeding Technology

- 5.3.1.2 By Cultivation Mechanism

- 5.3.1.3 By Country

- 5.3.1.3.1 Egypt

- 5.3.1.3.2 Ethiopia

- 5.3.1.3.3 Ghana

- 5.3.1.3.4 Kenya

- 5.3.1.3.5 Nigeria

- 5.3.1.3.6 South Africa

- 5.3.1.3.7 Tanzania

- 5.3.1.3.8 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Breeding Technology

- 5.3.2.2 By Cultivation Mechanism

- 5.3.2.3 By Country

- 5.3.2.3.1 Australia

- 5.3.2.3.2 Bangladesh

- 5.3.2.3.3 China

- 5.3.2.3.4 India

- 5.3.2.3.5 Indonesia

- 5.3.2.3.6 Japan

- 5.3.2.3.7 Myanmar

- 5.3.2.3.8 Pakistan

- 5.3.2.3.9 Philippines

- 5.3.2.3.10 Thailand

- 5.3.2.3.11 Vietnam

- 5.3.2.3.12 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Breeding Technology

- 5.3.3.2 By Cultivation Mechanism

- 5.3.3.3 By Country

- 5.3.3.3.1 France

- 5.3.3.3.2 Germany

- 5.3.3.3.3 Italy

- 5.3.3.3.4 Netherlands

- 5.3.3.3.5 Poland

- 5.3.3.3.6 Romania

- 5.3.3.3.7 Russia

- 5.3.3.3.8 Spain

- 5.3.3.3.9 Turkey

- 5.3.3.3.10 Ukraine

- 5.3.3.3.11 United Kingdom

- 5.3.3.3.12 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Breeding Technology

- 5.3.4.2 By Cultivation Mechanism

- 5.3.4.3 By Country

- 5.3.4.3.1 Iran

- 5.3.4.3.2 Saudi Arabia

- 5.3.4.3.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Breeding Technology

- 5.3.5.2 By Cultivation Mechanism

- 5.3.5.3 By Country

- 5.3.5.3.1 Canada

- 5.3.5.3.2 Mexico

- 5.3.5.3.3 United States

- 5.3.5.3.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Breeding Technology

- 5.3.6.2 By Cultivation Mechanism

- 5.3.6.3 By Country

- 5.3.6.3.1 Argentina

- 5.3.6.3.2 Brazil

- 5.3.6.3.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Bejo Zaden BV

- 6.4.5 East-West Seed

- 6.4.6 Groupe Limagrain

- 6.4.7 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.8 Sakata Seeds Corporation

- 6.4.9 Syngenta Group

- 6.4.10 Yuan Longping High-Tech Agriculture Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.