Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687155

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687155

Geothermal Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

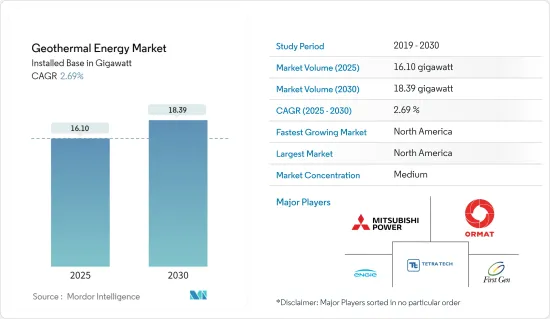

The Geothermal Energy Market size in terms of installed base is expected to grow from 16.10 gigawatt in 2025 to 18.39 gigawatt by 2030, at a CAGR of 2.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing electricity security concerns due to clean and eco-friendly resources and increasing demand for heating and cooling systems, including ground source heat pumps and district heating, are driving the growth of the geothermal energy market.

- On the other hand, the lucrative market for alternative clean energy sources like solar and wind is likely to hinder the market growth during the forecast period.

- Nevertheless, government-undertaken initiatives such as financial benefits and tax refunds to promote sustainable energy production are estimated to generate numerous growth opportunities for the geothermal energy market during the forecast period.

- North America is expected to be the largest market during the forecast period, with most of the demand coming from countries like the United States, Canada and Mexico, etc.

Geothermal Energy Market Trends

The Binary Cycle Power Plants Segment is Expected to Witness Significant Growth

- The binary cycle geothermal power plants incorporate low-temperature fluids below 182 degrees Celsius (or 360 degrees Fahrenheit) that are made to pass through a heat exchanger consisting of a secondary fluid. This secondary or binary fluid vaporizes the geothermal liquid and propels the turbine to produce electricity.

- In a binary-cycle geothermal power plant, the geothermal fluid does not directly come into contact with turbines, which makes it function differently from the other two geothermal technologies.

- The advantage of binary cycle power plants is that as the geothermal fluid of moderate temperature has greater availability than high-temperature geothermal resources, binary cycle power plants might become more prevalent to take advantage of this attribute in electricity generation, as per the US Department of Energy.

- The components of a binary cycle power plant include a heat exchanger, expander, condenser, generator, production well, reinjection well, and turbine. The average rated capacity of these power plants is around 6 MW. Conversely, large rated capacities co-exist with binary design cycles such as dual pressure, dual-fluid, and Kalinabinary cycles.

- The advantage of binary cycle power plants is that as the geothermal fluid of moderate temperature has greater availability than high-temperature geothermal resources, binary cycle power plants might become more prevalent to take advantage of this attribute in electricity generation, as per the US Department of Energy.

- Many new installations have been announced in recent years, which may support the growth of the geothermal energy market during the forecast period. As of September 2023, MTN Energy in Turkey re-initiated the process to conduct an Environmental Impact Assessment (EIA) method for the 2nd unit of the Babadere geothermal power plant. The examination is done to expand 11.8 MW of binary cycle plant to fulfill the electricity requirement of the region.

- As of 2023, the government of Italy consented to develop the proposed 10 MW binary cycle geothermal plant in Tuscany. Italy's first-ever binary cycle plant is expected to become active in 2027. It holds the potential to fulfill the power requirement of nearly 32,000 households and curtail carbon emissions of up to 40,000 tonnes. Hence, the onset of such projects could likely help in utilizing binary cycle plants in the forecast period

- Moreover, in 2023, the total geothermal energy installed capacity globally was around 14,846 MW, increasing from 14,653 MW in 2022. The capacity is increasing significantly across the world.

- Therefore, based on the abovementioned factors and recent developments, the binary cycle power plants segment is expected to grow significantly during the forecast period.

North America is Expected to Dominate the Market

- North America is one of the leading markets for geothermal energy worldwide, with the United States leading the regional and global markets regarding installed capacity. In 2023, approximately 16.5 terawatt hours of geothermal electricity were generated in the United States. This was an increase of roughly 0.5 terawatt hours from the 2022.

- Most of the geothermal power plants in the country are in the western states and the island state of Hawaii, where geothermal energy resources are close to the Earth's surface. California generates the most of the electricity from geothermal energy, whereas Northern California's Geysers dry steam reservoir is the world's largest known dry steam field.

- Moreover, California is home to the greatest number of geothermal power plants in the country. As of 2023, there were 31 such plants operated by electric utilities in the state. Nevada followed, with 26 geothermal power plants. That year, geothermal electricity generation across the United States reached a peak of 16.46 billion kilowatt hours.

- According to the International Renewable Energy Agency 2024, the total geothermal installed capacity in United States was around 2,674 MW in 2023. Moreover, in May 2023, Contact Energy announced that the company had signed a 10-year Power Purchase Agreement with Microsoft. Under the contract, Contact Energy will supply all the renewable energy attributes generated by the company's 51.4 MW Te Huka Unit 3 geothermal power station, New Zealand. Contact Energy announced the Te Huka Unit 3 geothermal power station in August 2022 and will be built at a cost of USD 189 million. The plant is expected to commence operations by the end of 2023.

- In February 2024, the United States Department of Energy's Geothermal Technologies Office announced a funding opportunity of up to USD 31 million for projects that support geothermal systems wellbore tools as well as the use of low-temperature geothermal heat for industrial systems. Also, funding of up to USD 23.1 million will enhance projects to address downhole cement and casing evaluation tools.

- Furthermore, new projects are also planned in the region, which is expected to support the region's market growth. For example, in March 2023, Also, the government in Mexico announced a exploratory project under Federal Electricity Commission (CFE) through a tender called 'Acquisition of Geothermal Well Drilling Services.

- Therefore, based on the above factors, North America is expected to dominate the geothermal energy market during the forecast period.

Geothermal Energy Industry Overview

The geothermal energy market is semi-fragmented. Some of the major players in the market (in no particular order) include Mitsubishi Power Ltd, Ormat Technologies Inc., Engie SA, Tetra Tech Inc., and First Gen Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 55756

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Geothermal Energy Installed Capacity and Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Electricity Security Concerns Due to Clean and Eco-Friendly Resources

- 4.5.1.2 Increasing Demand for Heating and Cooling Systems, Including Ground Source Heat Pumps

- 4.5.2 Restraints

- 4.5.2.1 Lucrative Market Opportunities for Alternative Clean Energy Sources Like Solar and Wind

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Plant Type

- 5.1.1 Dry Steam Plants

- 5.1.2 Flash Steam Plants

- 5.1.3 Binary Cycle Power Plants

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Spain

- 5.2.2.5 NORDIC

- 5.2.2.6 Turkey

- 5.2.2.7 Russia

- 5.2.2.8 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Malaysia

- 5.2.3.6 Thailand

- 5.2.3.7 Indonesia

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Nigeria

- 5.2.5.5 Qatar

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Geothermal Power Plant Equipment Manufacturers

- 6.3.1.1 Toshiba Corporation

- 6.3.1.2 Ansaldo Energia SpA

- 6.3.1.3 Fuji Electric Co. Ltd.

- 6.3.1.4 Baker Hughes Company

- 6.3.1.5 Doosan Skoda Power

- 6.3.2 Geothermal Power Plant EPC Companies and Operators

- 6.3.2.1 Mitsubishi Power Ltd

- 6.3.2.2 Ormat Technologies Inc.

- 6.3.2.3 Kenya Electricity Generating Company (KenGen)

- 6.3.2.4 Sosian Energy Limited

- 6.3.2.5 Tetra Tech Inc.

- 6.3.2.6 Engie SA

- 6.3.2.7 First Gen Corporation

- 6.3.2.8 PT Pertamina Geothermal Energy

- 6.3.2.9 Enel SpA

- 6.3.2.10 Aboitiz Power Corporation

- 6.3.1 Geothermal Power Plant Equipment Manufacturers

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Government-Undertaken Initiatives such as Financial Benefits and Tax Refunds

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.