PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640686

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640686

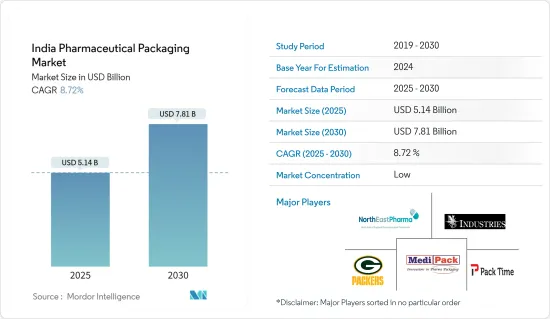

India Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The India Pharmaceutical Packaging Market size is estimated at USD 5.14 billion in 2025, and is expected to reach USD 7.81 billion by 2030, at a CAGR of 8.72% during the forecast period (2025-2030).

Pharmaceutical packaging uses materials designed to transfer and store pharmaceutical drugs safely. These materials are selected based on the drugs' characteristics, aiming to safeguard, identify, and maintain the integrity of the enclosed product. The packaging process ensures that the drugs are protected from external factors such as contamination, physical damage, and environmental conditions, which could potentially compromise their efficacy and safety. Pharmaceutical packaging is crucial in providing essential information about the drug, including dosage instructions and regulatory compliance details.

Key Highlights

- Pharmaceutical drugs face various hazards, spanning mechanical, chemical, biological, and climatic risks. They are packaged using multiple materials, including plastics, paper, glass, and metal, and tailored to different delivery methods, such as oral, pulmonary, injectable, transdermal, topical, interventional, nasal, and ocular.

- The Indian government has implemented extensive and ongoing reforms to bolster the pharmaceutical industry, unveiling policies to foster foreign direct investments (FDI). As part of the Aatmanirbhar Bharat Abhiyaan initiative, the government has introduced a range of short- and long-term measures to fortify the health system. These include implementing Production-linked Incentive (PLI) schemes specifically designed to enhance domestic pharmaceutical and medical device manufacturing. Moreover, India is actively positioning itself as a destination for spiritual and wellness tourism, leveraging its strengths in Ayurveda and yoga practices. These strategic moves are poised to impact the market studied significantly.

- The pharmaceutical packaging market in India is under increasing scrutiny for its impact on ecosystems and human health, given the escalating environmental concerns. The push for sustainability in the pharmaceutical industry is not just about reducing its carbon footprint but also about safeguarding ecosystems and public health for the long haul, especially in a country like India. The demand for eco-friendly and sustainable pharmaceutical packaging solutions is growing rapidly, driven by the need to address these environmental challenges effectively.

- Moreover, supplier bargaining power directly impacts pricing and quality, thereby dictating the value chain and, ultimately, the products and services delivered to consumers. As a supplier's power grows, so do the costs of raw materials, subsequently elevating the final product's price tag.

- The Indian pharmaceutical industry was already a major global player known for its generic drug manufacturing. The increasing demand for pharmaceutical products both domestically and internationally drove the need for diverse and advanced packaging solutions. The development and distribution of COVID-19 vaccines required specialized packaging solutions, including vials, syringes, and cold chain packaging, to ensure safe and effective delivery. According to the Ministry of Health and Family Welfare (India), the Indian state of Utter Pradesh reported the highest number of administered doses of the vaccine against the coronavirus as of November 13, 2023.

India Pharmaceutical Packaging Market Trends

Plastic Segment to Witness Major Market Growth

- The healthcare industry in India is witnessing a notable surge in the demand for flexible single-use plastic packaging, driven by a heightened emphasis on hygiene, safety, and convenience. While many industries are moving away from single-use plastics due to environmental concerns, healthcare is an exception, primarily due to safety and hygiene. This signifies the industry's reliance on single-use plastic packaging and drives the demand for plastic packaging. Plastic is a highly versatile material, including HDPE, PET, and PP, and is used in the pharmaceutical industry due to its flexibility, mechanical strength, and stability characteristics.

- The Indian government has implemented extensive and ongoing reforms to bolster the pharmaceutical industry. According to the India Brand Equity Foundation (IBEF), the Indian government spent 2.6% of the country's GDP on healthcare in the financial year 2023. Government healthcare spending is anticipated to be 2.5% of the GDP in the financial year 2025.

- Among product types, the bottle segment is anticipated to contribute significantly to the market's growth in line with the growth of HDPE and PET bottle production in the country and the emergence of HDPE (high-density polyethylene) bottles as the industry standard in the pharmaceutical industry due to their strength, resilience, and chemical resistance. These qualities make them perfect for safeguarding and storing a variety of medical supplies, supporting the growth of plastic bottle usage in the market.

- The material's intrinsic properties can be further improved through additives, improving performance and properties to act against oxygen, moisture, and UV radiation to the finished product, making plastic packaging a highly preferable type of packaging in the Indian pharmaceutical industry.

Bottles to be the Fastest-growing Product Segment in the Indian Market

- The demand for bottles for liquid pharmaceutical product packaging fuels the demand for glass, plastic, and other material-based bottle packaging. These bottles can be used for more than liquid medicines, solid pills, and gel tablets. They come in various sizes tailored to the specific dosage or product. Available in both glass and plastic, they maintain quality even after opening, provided they are stored as directed.

- The push for accessible, high-quality healthcare, especially for chronic diseases, at affordable rates is fueling the need for sustainable bottle pharmaceutical packaging solutions in India. According to the United Nations Economic and Social Commission for Asia and the Pacific (ESCAP), individuals aged between 15 and 64 constituted 68.9% of India's population in 2023. This demographic is projected to account for a share of 67.0% by 2050.

- The production and availability of HDPE-based bottles can support the growth of the bottles segment in the market because bottles ensure that medications remain safe and effective throughout their shelf life, shielding them from contamination and degradation. The demand for safe pharmaceutical packaging continues to grow in India. HDPE bottles are increasingly recognized for their ability to meet the rigorous standards required for storing and protecting medicinal products.

- PET plastic bottles have become the favored choice for pharmaceutical packaging owing to their applications and advantages in offering product protection, visibility, and customization. PET bottles can be environmentally sustainable due to their recyclability, reduced carbon footprint, and resource conservation. These factors are expected to support their increasing usage for packaging in the Indian pharmaceutical industry during the forecast period.

India Pharmaceutical Packaging Industry Overview

The Indian pharmaceutical packaging market is fragmented and dominated by significant players like Medipack Innovations Private Limited, Packtime Innovations Private Limited, North East Pharma Pack, NS Industries, and AS Packers. These companies leverage strategic collaborative initiatives to increase their market share and profitability. However, with technological advancements and product innovations, mid-size to smaller companies are growing their market presence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Awareness of Environmental Issues and Adoption of New Regulatory Standards

- 5.1.2 Surging Number of Chronic Disease Cases in India

- 5.2 Market Restraints

- 5.2.1 Fluctuations in Raw Material Costs Due to Suppliers' Bargaining Power

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Plastic

- 6.1.2 Glass

- 6.1.3 Other Material Types

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Vials and Ampoules

- 6.2.3 Syringes

- 6.2.4 Tubes

- 6.2.5 Caps and Closures

- 6.2.6 Pouches and Bags

- 6.2.7 Labels

- 6.2.8 Other Product Types

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Medipack Innovations Private Limited

- 7.1.2 Packtime Innovations Private Limited

- 7.1.3 North East Pharma Pack

- 7.1.4 N S Industries

- 7.1.5 A S Packers

- 7.1.6 JK Print Packs

- 7.1.7 West Pharmaceutical Packaging India Pvt. Ltd (West Pharmaceutical Services Inc.)

- 7.1.8 Huhtamaki India Ltd (Huhtamaki Oyj)

- 7.1.9 SGD Pharma India Ltd (SGD Pharma)

- 7.1.10 Uflex Limited

- 7.1.11 Amcor Flexibles India Pvt. Ltd (Amcor PLC)

- 7.1.12 Essel Propack Ltd

- 7.1.13 Parekhplast India Limited

- 7.1.14 Regent Plast Pvt. Ltd

- 7.1.15 Graham Blow Pack Pvt. Limited

- 7.1.16 Hoffmann Neopac AG

- 7.2 Vendor Market Share Analysis

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET