PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687335

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687335

Satellite Communication In The Defense Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

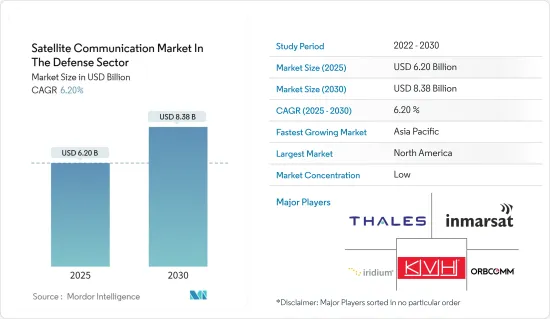

The Satellite Communication Market In The Defense is expected to grow from USD 6.20 billion in 2025 to USD 8.38 billion by 2030, at a CAGR of 6.2% during the forecast period (2025-2030).

Satellite communication is being used for many applications across the defense industry, including for extending broadband coverage, setting up 5G communications systems, integration and convergence of diverse wired and wireless technologies, earth observation, defense, security, and surveillance applications.

Key Highlights

- Defense personnel using a smartphone in the air can benefit from in-flight connectivity to access the internet. Ship personnel may benefit from crew connectivity with the latest maritime information, such as chart updates, engine monitoring, and weather routing broadcasts. The backpack terminals must be quickly and reliably deployed to support connectivity in harsh and emergent conditions.

- There have been accusations of linkages between cyberattacks and physical piracy, with pirates allegedly accessing the systems of shipping corporations to identify ships carrying valuable cargo with low onboard protection. As a result, the need to design a solid security system with features like a secret communication channel has arisen.

- The military and defense industry's main priority is the privacy and security of military communications. The need for enhanced data network security is driven by the increasing volume of IP-based data, including situational awareness video and remote sensor data provided across standard interfaces. Furthermore, as cyber resources on the ground, air, and space are subject to diverse threats, safeguarding military satellites from cyberattacks has become increasingly important. Security breaches could threaten citizen safety because military communication data and network infrastructure are vital.

- In February 2024, Thales announced to supply SurfSAT-L satellite communication solutions for F126 German frigates. This modernized system, previous versions of which have been in service with multiple navies worldwide, would ensure improved connectivity even under difficult operational conditions.

- However, cybersecurity has become a major concern in satellite communication, as launching a satellite to transmit data is highly sensitive. The challenge lies in the negative impact that cybersecurity threats can potentially have, as the vulnerabilities are mission-critical. The mission-critical vulnerabilities exposed to cybersecurity threats include the launch systems, communications, telemetry, tracking and command, and mission completion. The over-dependency of satellite communication on secure cyber capabilities across the satellite's lifespan makes it a serious concern, thus hindering its adoption.

Satellite Communication Market Trends

The Remote Sensing Segment is Expected to Hold a Significant Market Share

- Remote sensing aids the defense, military, and aerospace sectors by providing many data types. Navigating ships use remote sensing technology, such as wind-wave information, routing analysis, ship proximity, and GPS, to avoid hitting obstacles like icebergs and sinking. Many satellites orbit the Earth daily, collecting data useful for locating lost or destroyed aircraft. According to celestrak.org, there were around 26,673 orbit satellites globally in 2023.

- Remote sensing has been utilized as a surveillance method for many years. Remote sensors were used before the First World War by connecting them to hot air balloons and flying them over target cities. Remote sensing is carried out by specialized satellites with a wide range of capabilities. Optical satellites, radar imaging satellites, ultraviolet and infrared imagery satellites, and signal-intercepting communication satellites are a few examples.

- Remote sensing offers significant advantages over traditional forms of surveillance in that it can provide high-resolution imagery of light wavelengths other than visible light. This data can be utilized to track enemy movements, make strategic decisions, and assess tactical threats.

- There is now a need for better connection and higher-resolution imaging than before. This is beyond the ability of military-owned satellite technologies due to the fast growth of science and technology and the dependency of military activities on military-owned satellite technologies. Today, the US Military, the world's largest military, mainly relies on commercial satellite capabilities for military purposes. In October 2023, Airbus and US-headquartered defense company Northrop Grumman announced a Memorandum of Understanding (MoU) to develop and foster a strategic collaboration in military satellite communications for the United Kingdom's future wideband SKYNET military satellite communications program.

- A primary factor that could drive the satellite communication market's growth in the defense sector over the next few years is the application of AI in satellite communication for earth-based surveillance. The rising demand for remote sensing and monitoring applications and governments' plans to establish a network of spy satellites are also expected to drive market demand. The increased seaborne security risks, increased defense sector investments, and growing concerns about political instability in many parts of the world are driving the market.

Asia-Pacific is Expected to Hold a Significant Market Share

- The region is witnessing various innovations and investments in research and development to strengthen satellite communication in defense organizations. For instance, the Japanese government approved JPY 10.17 trillion (USD 66 billion) in defense spending in 2023. The funding will also be used to buy new defense equipment.

- In February 2024, the Indian armed forces allocated approximately INR 25,000 crore (USD 2,993.3 million) to fulfill its defense needs. These include establishing a surveillance satellite constellation and bolstering secure communication networks.

- Defense satellite services can assist military departments and boost operational effectiveness and mission success probabilities by offering dependable, secure broadband services that permit global interoperability on land, sea, and air.

- Moreover, military applications for satellite communication demand higher security standards than conventional uses. Military Satcom providers have, therefore, been driven to improve their solutions to meet the constantly rising demands of the military and defense industry. These demands include improving satellite communications capabilities, including bandwidth frequency, global broadcast, and personal communication service.

- In July 2024, Japan launched its upgraded Earth observation satellite, ALOS-4, aboard the new H3 rocket. The primary mission of the Advanced Land Observation Satellite (ALOS-4) is Earth observation, focusing on disaster response, mapmaking, and monitoring activities like volcanic eruptions, seismic shifts, and land movements. Additionally, it features an infrared sensor developed by the Defense Ministry, enabling it to monitor military actions, including missile launches.

Satellite Communication Industry Overview

The satellite communication market in the defense sector is fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Thales Group, Inmarsat Communications, Iridium Communications Inc., KVH Industries Inc., and Orbcomm Inc. Market players are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Seaborne Threats and Ambiguous Maritime Security Policies

- 5.1.2 Rise in Demand for Military and Defense Satellite Communication Solutions

- 5.2 Market Restraints

- 5.2.1 Cybersecurity Threats to Satellite Communication

- 5.2.2 Reliance on High-cost Satellite Equipment

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Ground Equipment

- 6.1.2 Services

- 6.2 By Application

- 6.2.1 Surveillance and Tracking

- 6.2.2 Remote Sensing

- 6.2.3 Disaster Recovery

- 6.2.4 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thales Group

- 7.1.2 Inmarsat Communications

- 7.1.3 Iridium Communications Inc.

- 7.1.4 KVH Industries Inc.

- 7.1.5 Orbcomm Inc.

- 7.1.6 Cobham PLC

- 7.1.7 Thuraya Telecommunications Company (Al Yah Satellite Communications Company P.J.S.C)

- 7.1.8 ViaSat Inc.

- 7.1.9 ST Engineering iDirect

- 7.1.10 L3Harris Technologies Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET