PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1523311

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1523311

Indonesia Textiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

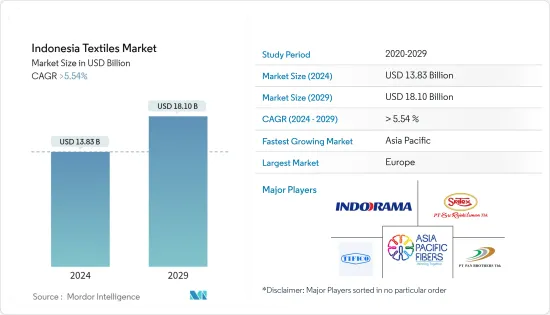

The Indonesia Textiles Market size is estimated at USD 13.83 billion in 2024, and is expected to reach USD 18.10 billion by 2029, growing at a CAGR of greater than 5.54% during the forecast period (2024-2029).

* The Indonesian textile industry is rapidly expanding. There are several reasons why Indonesia's textile and garment industry is now attractive to international investors and operators. Unlike many other Asian countries and the rest of the world, the Indonesian labor force is relatively young and growing at a fast pace. In 2023, there were about 5,000 active large and medium textiles and garment companies (SMEs) in the Indonesian market, while about 500,000 active small and micro businesses (SMEs).

* As one of the world's largest producers of cotton, Indonesia has access to a wide range of raw materials, including wool, silk, and a variety of natural and synthetic fibers, ensuring reliable supply chains.

* The Indonesian textile and garment industry has a long history, dating back to the pre-colonial era, where traditional fabrics such as batik, ikat, and other traditional textiles were prized for their unique designs and craftsmanship. In part, this is because successive governments have long supported the sector for its economic and cultural contribution to the nation.

* As production technology continues to improve, the government of Indonesia has set the goal of making Indonesia 4.0 as a goal for 2030, focusing on technological advancement in five key sectors, including the textile industry. As a result, some operations are transitioning to modern, higher-margin, high-tech fabrics for use in automotive, healthcare, sportswear, etc.

* Indonesia has a population of approximately 273 million people. This means that there is a large local apparel market. As the economy has been improving recently, disposable income has been increasing.

* The growth of e-commerce and the improvement of domestic logistics is also driving local demand. Indonesia's domestic apparel market was estimated to be worth USD 21.7 billion by 2023, with an annual growth rate of 3.5%. Every Indonesian is spending USD 78.14 on clothing this year.

* There has been a worldwide trend toward sustainable and ethical apparel production in recent years. People are becoming more conscious of the environmental and social effects of the clothes they buy. The Indonesian textile and garment industry is taking advantage of this trend by implementing sustainable practices. Investing in organic cotton, environmentally friendly dyeing, and promoting accepted ethical labor practices promote new market trends and attract conscious consumers.

Indonesia Textile Market Trends

Indonesian Cotton Imports Set to Rise in 2024

* 2023/24 Indonesian cotton imports are projected to grow by about 5.9% to around 1.8 million bales, compared to 2022/23. This is based on the assumption that spinners will consume more inventory on hand before making new purchases, while global demand slows and tight competition from low-priced, illegal imports of clothing on the domestic market has resulted in lower cotton utilization, resulting in an increase in end stocks to 379.000 bales in 2023 / 24.

* The Indonesian manufacturing industry increased by 5.20% in the third quarter of 2023 (compared to 4.94% in the same three-month period last year), according to the latest data from the BPS (Badan Pusat Statistics Agency).

* However, the global economic conditions have not improved, leading to a decrease in demand from Indonesia's textile and textile product export destination countries, a decrease in consumer buying power, and fierce competition from illegal, low-priced imports into the domestic market. Furthermore, the appreciation of the rupiah has weakened the Indonesian currency against the US dollar, which has further dampened cotton imports. These gloomy conditions are expected to persist into 2024.

* Australia remained the biggest supplier of cotton to Indonesia, with 52.1 percent market share and 268,000 bale volume between August and October 2023. Brazil and the United States followed at 21.1 percent and 86,000 bale, respectively. The United States market share continues to decrease due to lower prices and Australia's nearness.

Increasing sustainable practices in the market

Indonesia, renowned for its rich textile heritage and vibrant fashion scene, is witnessing a transformative shift toward sustainability. Building on its traditional textile artistry, especially the iconic batik, Indonesia's fashion industry is now embracing sustainability.

Designers increasingly turn to organic cotton, bamboo fabric, and recycled materials, seamlessly blending them with traditional techniques. This fusion results in unique, environmentally conscious fashion pieces.

Rising consumer awareness about fashion's environmental and social impact is fueling demand for ethically produced clothing. Indonesian designers and brands are responding by adopting fair trade practices, ensuring fair treatment of workers throughout the supply chain. This ethical shift also aligns with global sustainability standards.

Collaborations with local artisans are gaining momentum, empowering traditional craftsmen and women. These partnerships not only preserve cultural heritage but also foster sustainable livelihoods. The concept of circular fashion, emphasizing longevity and recycling, is gaining traction. This approach minimizes waste and contributes to a more sustainable industry.

Indonesia is also embracing technology, such as 3D printing and innovative fabric development, to further enhance sustainability in its fashion industry. These efforts are gaining global recognition, positioning Indonesia as a leading force in the green fashion movement.

In summary, Indonesia's fashion industry is undergoing a remarkable sustainability transformation. From embracing eco-friendly materials to championing fair trade, the nation's fashion landscape is evolving, proving that style and sustainability can indeed go hand in hand. As consumer demand for responsible choices rises, Indonesian fashion designers are spearheading a greener, more ethical future for the industry.

Indonesia Textiles Industry Overview

The Indonesian textile industry needs to be more cohesive, with many local and international players in the market. The key players in the polycarbonate market are PT. Sri Rejeki Isman Tbk, PT. Asia Pacific Fibers Tbk, Indorama Corporation (PT. Indo-Rama Synthetics Tbk), PT. Pan Brothers Tbk, and PT. Tifico Fiber Indonesia Tbk, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS & DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growing domestic market

- 4.2.1.2 Government support driving the market

- 4.2.2 Restraints

- 4.2.2.1 Competition from other countries

- 4.2.2.2 Infrastructure challenges

- 4.2.3 Opportunities

- 4.2.3.1 Rising demand for sustainable textiles

- 4.2.3.2 Technological advancements driving the market

- 4.2.1 Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technological Advancements in Textile industry

- 4.6 Pricing Analysis and Revenue Analysis of Textile Market

- 4.7 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Clothing

- 5.1.2 Industrial/Technical

- 5.1.3 Household

- 5.1.4 Other Applications

- 5.2 By Material

- 5.2.1 Cotton

- 5.2.2 Jute

- 5.2.3 Silk

- 5.2.4 Synthetics

- 5.2.5 Wool

- 5.2.6 Other Materials

- 5.3 By Process

- 5.3.1 Woven

- 5.3.2 Non-woven

6 COMPETITIVE LANDSCAPE

- 6.1 Overview

- 6.2 Company Profiles

- 6.2.1 PT. Ever Shine Tex Tbk

- 6.2.2 PT Trisula Textile Industries Tbk

- 6.2.3 PT Century Textile Industry Tbk (Toray Industries Inc.)

- 6.2.4 PT Pan Brothers Tbk

- 6.2.5 PT Polychem Indonesia Tbk

- 6.2.6 PT Sri Rejeki Isman Tbk

- 6.2.7 PT Indo Kordsa Tbk

- 6.2.8 PT Tifico Fiber Indonesia Tbk

- 6.2.9 PT Panasia Group

- 6.2.10 PT Asia Pacific Fibers Tbk

- 6.2.11 PT Tyfountex Indonesia

- 6.2.12 PT Eratex Djaja Tbk

- 6.2.13 PT Argo Pantes Tbk

- 6.2.14 Indorama Corporation (PT. Indo-Rama Synthetics Tbk)*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX