PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851767

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851767

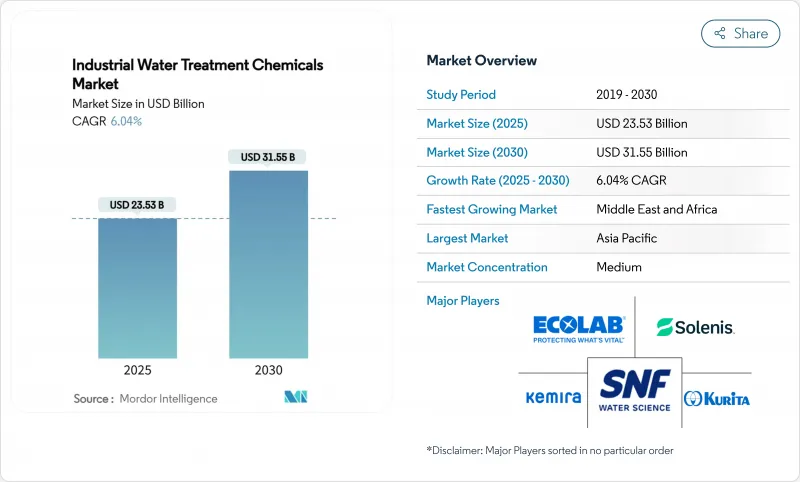

Industrial Water Treatment Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Industrial Water Treatment Chemicals Market size is estimated at USD 23.53 billion in 2025, and is expected to reach USD 31.55 billion by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

Growth draws strength from tightening PFAS removal mandates, expansion of shale gas operations that swell produced-water volumes, and rising industrial water-reuse targets in arid regions. Suppliers are pivoting from disposal-oriented solutions toward resource-recovery models that pair advanced chemistries with AI-enabled dosing platforms. The power sector continues to anchor demand, while biocides and disinfectants outpace the broader industrial water treatment chemicals market as industrial microbiological control becomes mission-critical. Competitive dynamics are intensifying as full-service models-combining digital monitoring, specialty chemicals, and equipment-replace commodity chemical contracts.

Global Industrial Water Treatment Chemicals Market Trends and Insights

Rising shale gas produced-water volumes

Shale operations in the Permian Basin now generate millions of barrels of produced water each day, requiring sophisticated oxidants, biocides, and high-temperature coagulants for safe recycling or disposal. The resulting chemical demand is compounded by operator targets to recycle up to 90% of flowback water, as this lowers freshwater intake and disposal fees. Suppliers that formulate corrosion-resistant blends capable of handling 140 °C temperatures and total dissolved solids beyond 150,000 mg/L secure premium pricing. Increasingly, field deployments layer AI dosing platforms onto treatment skids, cutting overdosing and trimming chemical spend by 15-25% while maintaining performance. These gains establish an economic incentive that locks in higher volumes for the industrial water treatment chemicals market.

Tightening discharge norms for heavy metals and COD

The European Union's Industrial Emissions Directive and the United States NPDES permits impose lower thresholds for cadmium, mercury, and chemical oxygen demand, forcing factories to upgrade treatment trains. Advanced organic binders paired with ferric-based coagulants capture fine particulates and dissolved metals more effectively than legacy alum solutions. When paired with real-time turbidity sensors, plants report a 35% reduction in sludge generation and a 20% drop in coagulant consumption without compromising compliance. The regulatory stick, coupled with measurable opex savings, accelerates adoption across textiles, metal finishing, and electronics segments.

Substitution by membrane and UV systems

Ultrafiltration modules, paired with UV-LED disinfection, now achieve 93% turbidity removal with 22% less coagulant demand than conventional setups. Municipal utilities in China already operate 6.7 million m3/day of membrane-based capacity, shrinking alum and polymer volumes. Chemical suppliers respond by shifting portfolios toward anti-fouling cleaners and membrane preservatives. While overall reagent tons may drop, revenue potential remains if suppliers pivot to these higher-margin adjuncts.

Other drivers and restraints analyzed in the detailed report include:

- Industrial water-reuse mandates in water-scarce regions

- PFAS removal requirements in industrial effluents

- Volatile specialty-chemical raw-material prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrosion inhibitors captured 24.16% of the industrial water treatment chemicals market share in 2024, underscoring their central role in protecting high-pressure boilers, condensers, and pipelines. Demand is sticky because plant operators view USD 0.10 per cubic-meter treatment costs as cheap insurance against multi-million-dollar outage events. Organophosphate blends now integrate film-forming amino acids that tolerate temperature spikes above 150 °C without depositing on heat-exchange surfaces, lengthening inspection cycles. Biocides and disinfectants, though smaller today, are advancing at a 6.83% CAGR, the highest within the industrial water treatment chemicals market. Microbiologically influenced corrosion costs the oil, gas, and power sectors billions each year, pushing uptake of fast-acting oxidizing biocides such as DBNPA and glutaraldehyde that meet tightening toxicity caps. AI dosing tools fine-tune ppm levels, cutting waste and helping plants stay below discharge limits for residual oxidants.

Scale inhibitors, coagulants, and flocculants continue to support large base-load volumes. Bio-derived tannin coagulants achieve PFAS capture efficiencies comparable to alum, but higher purchase prices restrict them to sustainability-driven customers. Oxidants, antifoams, oxygen scavengers, and sludge conditioners serve niche applications, yet they deliver stable gross margins because performance specs differ by site and carry high switching costs. As compliance thresholds and reuse rates rise, specialty blends rather than single-function reagents are set to propel the industrial water treatment chemicals market size over the forecast window.

The Industrial Water Treatment Chemicals Market Report is Segmented by Product Type (Scale Inhibitors, Corrosion Inhibitors, Biocides and Disinfectants, Coagulants and Flocculants, and More), End-User Industry (Oil and Gas, Power, Paper, Metals and Mining, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the industrial water treatment chemicals market with 37.58% revenue share in 2024, driven by rapid industrialization and expanding municipal infrastructure. China operates more than 580 membrane-based wastewater plants treating 6.7 million m3 each day, which lifts demand for anti-scalants, biocides, and cleaning chemicals that maintain permeate flux. India's water initiatives, including the Jal Jeevan Mission, sustain annual growth of 9.7% through 2025 and open new municipal bidding rounds that specify both conventional and advanced chemistries.

North America remains a technology bellwether. EPA PFAS limits require sweeping plant retrofits, pushing utilities to procure surfactant-enhanced coagulants, granular activated carbon replacement chemicals, and oxidative cleaners at scale. Shale basins add high-volume demand for specialty oxidants, biocides, and corrosion inhibitors formulated for brines exceeding 150,000 mg/L TDS. Europe holds a mature but innovation-driven user base that favors bio-based polymers and low-phosphorus blends aligned with Green Deal goals.

The Middle East & Africa region is projected to record a 7.12% CAGR, the fastest globally. USD 80 billion earmarked for water projects in Saudi Arabia and wider Gulf desalination expansion underpin adoption of anti-scalants and membrane cleaners designed for high-salinity RO plants. Industrial clusters in the United Arab Emirates and Egypt pursue zero-liquid-discharge systems, bolstering uptake of evaporation-control antiscalants and multi-cycle corrosion inhibitors. Latin America posts steady growth, led by mining hot-spots in Chile and Peru that need reagents for tailings water recycling and arsenic removal.

- 3M

- Accepta Water Treatment

- BASF

- Buckman

- Chemifloc

- Clariant

- DuPont

- Ecolab Inc.

- Feralco AB

- Italmatch AWS

- IXOM

- Kemira

- Kurita Water Industries Ltd

- Lenntech B.V.

- SNF Group

- Solenis LLC

- Thermax Limited

- Veolia Water Technololgies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising shale gas generated produced-water volumes (US)

- 4.2.2 Growth in chemical & pulp-and-paper wastewater generation

- 4.2.3 Tightening discharge norms for heavy metals & COD

- 4.2.4 Industrial water-re-use mandates in water-scarce regions

- 4.2.5 PFAS removal requirements in industrial effluents

- 4.3 Market Restraints

- 4.3.1 Substitution by membrane & UV systems

- 4.3.2 Volatile specialty-chemical raw-material prices

- 4.3.3 Net-zero roadmaps favouring chemical-free treatments

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Scale Inhibitors

- 5.1.2 Corrosion Inhibitors

- 5.1.3 Biocides and Disinfectants

- 5.1.4 Coagulants and Flocculants

- 5.1.5 pH Conditioners

- 5.1.6 Antifoams

- 5.1.7 Oxygen Scavengers

- 5.1.8 Sludge Conditioners

- 5.1.9 Oxidants

- 5.1.10 Others

- 5.2 By End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Power

- 5.2.3 Paper

- 5.2.4 Metals and Mining

- 5.2.5 Chemicals

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Accepta Water Treatment

- 6.4.3 BASF

- 6.4.4 Buckman

- 6.4.5 Chemifloc

- 6.4.6 Clariant

- 6.4.7 DuPont

- 6.4.8 Ecolab Inc.

- 6.4.9 Feralco AB

- 6.4.10 Italmatch AWS

- 6.4.11 IXOM

- 6.4.12 Kemira

- 6.4.13 Kurita Water Industries Ltd

- 6.4.14 Lenntech B.V.

- 6.4.15 SNF Group

- 6.4.16 Solenis LLC

- 6.4.17 Thermax Limited

- 6.4.18 Veolia Water Technololgies, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment