PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686650

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686650

India HVDC Transmission Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

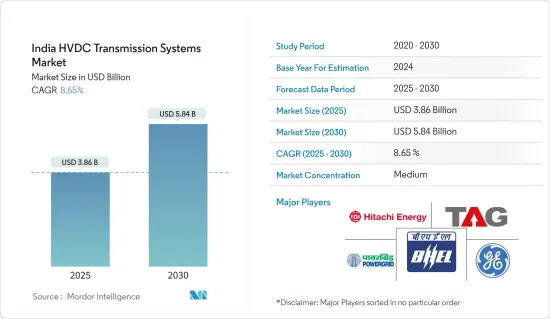

The India HVDC Transmission Systems Market size is estimated at USD 3.86 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 8.65% during the forecast period (2025-2030).

The COVID-19 pandemic did not alter the country's medium- to long-term plans for power transmission. Power transmission, which was categorized as an essential service by the Ministry of Power during the COVID-19 period, continued as an usual business in the country. Factors such as growing renewable energy sector, rapid urbanization, and increasing rural electrification, are expectde to drive the market during the forecast period. On the other hand, the growing distributed and remote power systems in the country is likely to hinder the market growth.

Key Highlights

- The HVDC overhead transmission system is likely to maintain its larger market share during the forecast period, thus making it a dominating segment in the India HVDC market.

- The country's pan to deploy 30 GW of offshore wind energy installations by 2030, is expected to create several opportunities for HVDC transmission systems, which are more efficient for offshore environments.

- The increasing expansion of transmission electrcity grid in India is expected to drive the country's HVDC transmission systems market during the forecast period.

India HVDC Transmission System Market Trends

HVDC Overhead Transmission Systems Expected to Dominate the Market

- HVDC overhead transmission systems have a simpler line tower construction requirement compared to HVAC transmission lines. Also, HVDC overhead transmission systems have lower per-unit costs, including cost per km of line and per MV of transmitted power.

- In major part of the world, high-voltage overhead transmission is a popular means of power transmission. DC decreases the total cost for long-distance power transmission with overhead lines cables.

- Moreover, the high-voltage overhead transmission is much less expensive to build and much quicker to repair than underground transmission. However, it has seen decreasing applications in densely-populated urban and commercial areas.

- The cost of HVDC transmission depends on the terminal station's cost and the cost of the transmission line. But in case of HVAC transmission network there are more conductors in comparison to HVDC, which increases the mechanical load. Due to the increased load the transmission line cost increases with the distance. The cost increase in HVAC is greater than the HVDC line per 100Km of a transmission line, thus making HVDC a more cost efficient option for long transmissions.

- Capacity additions in pe-existing HVDC networks are also driving the overhead transmission network in India. For instance, during 2019-2020, deployment of HVDC substations is witnessed in multiple projects, including Jharsuguda (Sundargarh) S/S with capacity addition of 3000 MVA, Aligarh (PG) 765 kV GIS, and others. In total, the nation increased the capacity of the pre-existing substation by the 12870 MVA, with the HVDC-based substations holding a significant share.

- India is currently witnessing large-scale COVID-19 vaccination, which is resulting in improving market conditions. Amid this, Power Grid's 320 kV 2000 MW Pugalur (Tamil Nadu) - Thrissur (Kerala) HVDC project was inaugurated on 19th February 2021. The project, with cost of INR 5070 crore, is part of the Raigarh-Pugalur-Thrissur 6000 MW HVDC system and enables the transfer of 2000 MW to Kerala through the HVDC station at Thrissur. Earlier in September 2020, Power Grid Corporation of India Ltd. commissioned Pole-1 of the Raigarh Pugalur HVDC Transmission system comprising Raigarh HVDC Terminal Station (Chhattisgarh) & Pugalur HVDC Terminal Station.

- Therefore, owing to the above points, HVDC overhead transmission systems are expected to dominate the market during the forecast period.

Increasing Expansion of Transmission Electrcity Grid expected to Drive the Market

- For HVDC transmission lines, the transmission losses are in inverse relation with the voltage ratings of electricity, i.e., the higher the voltage rating of electricity transmitted, the lower will be the transmission losses. Furthermore, the HVDC transmission lines can transmit higher voltage current than HVAC lines. In places with limited availability of land, HVDC transmission lines are preferred over HVAC, as they have higher power transmission capacity, and hence, can transmit more electricity per unit land usage.

- India has the second-highest population globally. With a high population, demand for electrical energy and transmission network is growing in India. However, the increasing size and complexity of a transmission network create problems related to load flow, power oscillation, and voltage quality. Thus, to eliminate the issues, HVDC transmission lines are prioritized by various central, state and private power transmission companies in India.

- As of 2020, more than 58% of the transmission lines in the country have voltage ratings of above 400 kV while 42% were 220 kV.

- The growth in HVDC transmission networks helped several states to meet the electricity demand, by importing electricity from states with surplus electricity or high installed capacity. Under the One Nation-One Grid plan, the five regional grids were interconnected to exchange surplus electricity among the regions. Moreover, as per the Ministry of power, in FY 2019, power transmission and distribution companies in India suffered a loss of INR 27,000 crore, primarily due to transmission and distribution losses.

- Further to enhance the interregional electricity exchange, a few HVDC projects are in expansion phases. Upgradation of Champa Pool- Kurukshetra HVDC Bipole from 1500 MW to 2000 MW by 2022 is one among the expansion projects. Additionally, in December 2020, Maharashtra unveiled USD one billion underground HVDC project from Aarey to Kudus in Palghar District. The project is under the proposed state and will help to solve an issue like a complete blackout in the Mumbai Metropolitan Region in October 2020.

- Therefore, based on the above-mentioned factors, increasing expansion of transmission electricity grid is expected to drive the India HVDC transmission systems market during the forecast period.

India HVDC Transmission System Industry Overview

The India HVDC transmission systems market is moderately consolidated. Some of the major companies include Hitachi Energy Ltd, General Electric Company, TAG Corporation, Power Grid Corporation of India Limited, and Bharat Heavy Electricals Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

5 MARKET SEGMENTATION

- 5.1 Transmission Type

- 5.1.1 HVDC Overhead Transmission System

- 5.1.2 HVDC Underground & Submarine Transmission System

- 5.2 Component

- 5.2.1 Converter Stations

- 5.2.2 Transmission Medium (Cables)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Hitachi Energy Ltd

- 6.3.2 Siemens AG

- 6.3.3 General Electric Company

- 6.3.4 Adani Transmission Ltd

- 6.3.5 TAG Corporation

- 6.3.6 Power Grid Corporation of India Limited

- 6.3.7 Bharat Heavy Electricals Limited

- 6.3.8 Tata Projects Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS