PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433879

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433879

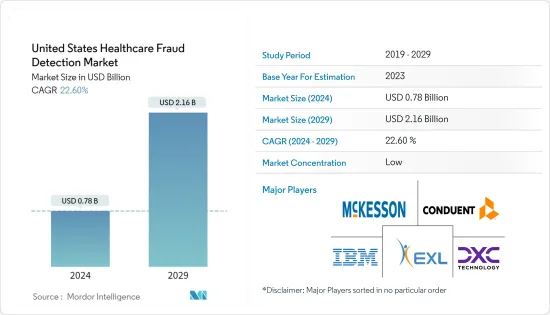

United States Healthcare Fraud Detection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The United States Healthcare Fraud Detection Market size is estimated at USD 0.78 billion in 2024, and is expected to reach USD 2.16 billion by 2029, growing at a CAGR of 22.60% during the forecast period (2024-2029).

The COVID-19 epidemic illustrates how public health crises affect emergency departments and hospital systems. The pandemic of COVID-19 had a tremendous impact on healthcare delivery. Urgent adjustments in billing codes, telehealth, and prescriptions enabled health care systems to successfully modify care delivery methods. These quick modifications, however, posed potential vulnerabilities for fraud and waste. According to the study published in May 2021, titled "The COVID-19 Epidemic As A Catalyst For Health Care Fraud" coronavirus aid, relief, and economic security (cares) acted would shortly provide funds to an estimated USD140 million United States households. This, combined with the heightened susceptibility to fraud that came with many people's dread, raises the possibility that covid-19 had been the newest consumer-facing fraud hot zone. Such spreads were common in the United States during the pandemic. In addition, in May 2021, the Department of Justice announced criminal charges against 14 defendants in seven federal districts across the United States, including 11 newly charged defendants and three charged in superseding indictments, for their alleged participation in various health care fraud schemes that exploited the COVID-19 pandemic and resulted in over USD 143 million in false billings. Hence, during a pandemic, healthcare fraud increased thereby growing the adoption of healthcare fraud detection systems and thus positively impacting the market.

The major factors attributing to the growth of the United States healthcare fraud detection market are increasing fraudulent activities in the United States healthcare, growing pressure to increase operational efficiency and reduce healthcare spending, and the prepayment review model. For instance, in September 2020, the Department of Health and Human Services Office charged 345 defendants in 51 judicial districts with participating in healthcare fraud schemes involving more than USD 6 billion in alleged losses to federal healthcare programs

According to the National Health Care Anti-Fraud Association, health insurance fraud in the United States cost around USD 80 billion per year to consumers. Criminals are looking forward to profiting from the people across the country. As most people in the country have health insurance, free medical treatments or complimentary consultation offers are being stolen. Additionally, in July 2022, the Department of Justice announced criminal charges against 36 individuals in 13 federal districts around the United States for alleged fraudulent telemedicine, cardiovascular and cancer genetic testing, and durable medical equipment (DME) scams totaling more than USD 1.2 billion. Thus, an increase in healthcare fraud in the country is expected to rise in demand for the healthcare fraud detection market.

Such cases of fraud in health insurance are causing damage to the medical history of people. A few years back, it was difficult for healthcare providers to identify the fraud, as criminals were using all types of patient identifications and insurance information. According to the National Health Care Anti-Fraud Association's (NHCAA) Consumer Information section, updated in 2021, the United States spends more than USD 2.27 trillion on health care annually. According to the NHCAA, USD 10 billion is lost each year due to health care fraud, and USD 54 billion is anticipated to be conned and stolen in the United States. These actions, as well as the loss of income as a result of fraud and illicit operations, make healthcare fraud the country's most serious problem. Over the projected period, this is expected to fuel demand for healthcare fraud detection systems. Due to such frauds, patients are compelled to pay higher premiums. Therefore, the United States healthcare department is currently more focused on the reduction of such cases by implementing fraud detection technology. Therefore, it is believed that due to the rising fraudulent activities in the United States healthcare department, the market studied may grow in the future. However, the lack of skilled healthcare IT labors in the country may restrain the market growth over the forecast period.

US Healthcare Fraud Detection Market Trends

Insurance Claims Segment is is Expected to Witness a Healthy Growth in Future.

The healthcare fraud detection solution plays a major role in the review of insurance claims, as most fraud cases occur while claiming insurance. As per the estimates of the National Health Care Anti-Fraud Association (NHCAA) in August 2022, healthcare fraud costs the United States around USD 68 billion, annually. Additionally, in August 2022 updates by Coalition Against Insurance Fraud (CAIF), insurance fraud can cost Unite States consumers USD 308.6 billion per year. This figure includes estimates of yearly fraud expenses in a variety of liability sectors, including life insurance (USD 74.7 billion). Health insurance fraud is a type of fraud, in which false or misleading information is provided to a health insurance company in an attempt to have them pay unauthorized benefits to the policyholder another party, or the entity providing services. The offense can be committed by the insured individual or the provider of health services.

Most health insurances include specific benefits and health insurance fraud practices, such as overbilling for the type of services received. A central objective of the recent United States healthcare policy reform has been to increase access to stable, affordable health insurance. Many strategic initiatives are being taken in the country too. For instance, in June 2021, Artivatic launched the ALFRED-AI HEALTH CLAIMS platform for automating end-to-end health claims, and its fraud and abuse detection capacity is 30% or more. The ALFRED-AI HEALTH CLAIMS platform also allows users to self-learn and evolve a system for better risk assessment, fraud detection, and decision-making.

Owing to the aforementioned factors, the review of the insurance claims segment is expected to grow exponentially in the United States healthcare fraud detection market.

US Healthcare Fraud Detection Industry Overview

The United States healthcare fraud detection market is moderately competitive and consists of several major players. In terms of market share, some of the major players currently dominate the market. With the rising adoption of healthcare IT and an increasing number of fraud cases, few other smaller players are expected to enter into the market in the coming years. Some of the major players in the market are Conduent Inc., DXC Technology Company, EXL (Scio Health Analytics), International Business Machines Corporation (IBM), and Mckesson, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Fraudulent Activities in the US Healthcare Sector

- 4.2.2 Growing Pressure to Increase the Operation Efficiency and Reduce Healthcare Spending

- 4.2.3 Prepayment Review Model

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Healthcare IT Labors in the Country

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Type

- 5.1.1 Descriptive Analytics

- 5.1.2 Predictive Analytics

- 5.1.3 Prescriptive Analytics

- 5.2 By Application

- 5.2.1 Review of Insurance Claims

- 5.2.2 Payment Integrity

- 5.3 By End User

- 5.3.1 Private Insurance Payers

- 5.3.2 Government Agencies

- 5.3.3 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Conduent Inc.

- 6.1.2 DXC Technology Company

- 6.1.3 EXL (Scio Health Analytics)

- 6.1.4 International Business Machines Corporation (IBM)

- 6.1.5 Mckesson

- 6.1.6 Northrop Grumman

- 6.1.7 OSP Labs

- 6.1.8 SAS Institute

- 6.1.9 Relx Group PLC (LexisNexis)

- 6.1.10 United Health Group Incorporated (Optum Inc.)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS