Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689739

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689739

Southeast Asia Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

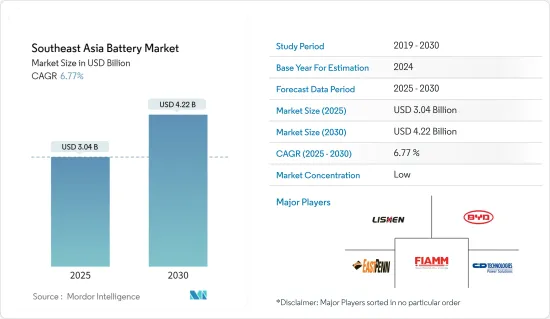

The Southeast Asia Battery Market size is estimated at USD 3.04 billion in 2025, and is expected to reach USD 4.22 billion by 2030, at a CAGR of 6.77% during the forecast period (2025-2030).

Though COVID-19 negatively impacted the market in 2020, it has reached pre-pandemic levels.

Key Highlights

- Over the medium term, factors such as growing demand from the automotive sector, declining lithium-ion battery prices, and plans to make Southeast Asia a data center hub are expected to drive the market during the forecast period.

- Despite the growing demand for batteries in the automotive, data centers, and telecommunications sectors, the battery energy storage segment is expected to witness stagnant growth, as most countries depend on other energy storage alternatives. This, in turn, is likely to restrain the growth of the battery market in the energy storage segment during the forecast period.

- Moreover, plans to integrate renewable energy with the national grids in respective countries are expected to create significant opportunities for lithium-ion battery manufacturers and suppliers during the forecast period.

- Thailand is expected to dominate the market during the forecast period due to the increasing demand from the automotive, data center, and other end-user sectors.

Southeast Asia Battery Market Trends

Automotive Sector is Expected to Dominate the Market

- Vehicles with internal combustion engines (ICE) were the only types used earlier. ICE vehicles have been using lead-acid batteries, which may continue with no significant replacement available.

- However, nowadays, technology has been shifting toward electric vehicles due to rising concerns about the environment. In EVs, mostly lithium-ion batteries are used, as they provide high energy density, have low self-discharge, and require little maintenance.

- Lithium-ion battery systems propel plug-in hybrid and electric vehicles. Due to their high energy density, fast recharge capability, and high discharge power, lithium-ion batteries are the only available technology that meets the OEM requirements for vehicles' driving range and charging time. Lead-based traction batteries are not competitive for use in full-hybrid electric cars or electric vehicles because of their lower specific energy and higher weight.

- Moreover, the exponential decline in lithium-ion batteries' prices reduced their value by 81.5% from USD 668/kWh in 2013 to USD 123/kWh in 2021. The trend is likely to continue in the future, making EVs affordable to a broader range of economic groups in the region.

- For hybrid vehicles, several battery technologies can provide these functions in different combinations, with nickel-metal hydride and lithium-ion batteries preferred at higher voltages due to their fast recharge capability, good discharge performance, and lifetime endurance.

- Several regional governments developed plans to reduce emissions, which are expected to increase the region's share of electric vehicles (EV) during the forecast period.

- Therefore, owing to the abovementioned factors, the automotive sector is expected to dominate the Southeast Asian battery market during the forecast period.

Thailand is Expected to Dominate the Market

- Thailand accounts for the majority share of the market. This trend is expected to continue during the forecast period, owing to the increasing demand from the automotive, data center, and telecom sectors.

- Thailand provides great investment potential for the automotive sector. The country has a leading automotive production base in the Association of Southeast Asian Nations. The country has developed from an assembler of auto components into a top automotive manufacturing and export hub in over 50 years.

- Moreover, the country is expected to witness high growth in the EV segment, particularly in plug-in hybrid electric vehicles (PHEVs) and hybrid electric vehicles (HEVs). In September 2022, BYD Co. announced plans to build its first overseas electric passenger car plant in Rayong, Bangkok.

- Under the National Electric Vehicle Policy Committee (NEVPC) roadmap, Thailand is expected to add between 100,000 and 300,000 vehicles by 2025 and finally between 400,000 and 750,000 vehicles by 2026.

- Further, in April 2022, the Thai government agreed to fund the manufacturing of zinc-ion batteries to power electric vehicles (EVs). Thailand will develop a local EV battery plant worth using zinc as a natural resource.

- Furthermore, Thailand has made great progress in growing its ICT sector, moving quickly from being a secondary player in the world of technology to one of the regional leaders. Over the past decade, the digital share in Thailand has been closing at an ever-increasing speed, with the country making significant gains in labor force education and skills building.

- The government planned its business module under Thailand's 4.0 Program. This program helps increase the use of new technologies such as cloud computing, interactive media, big data, and the internet of things. Hence, the country is expected to have a high demand for data centers, which is expected to increase the demand for batteries in its data centers during the forecast period.

- Therefore, owing to the abovementioned factors, Thailand is expected to dominate the Southeast Asian battery market during the forecast period.

Southeast Asia Battery Industry Overview

The Southeast Asian battery market is partially fragmented due to the presence of key players, including (in no particular order) Tianjin Lishen Battery Joint-Stock Co. Ltd., FIAMM Energy Technology SpA, BYD Co. Ltd., C&D Technologies Inc., and East Penn Manufacturing Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 67784

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery Type

- 5.1.1 Lead-acid Battery

- 5.1.2 Lithium-ion Battery

- 5.1.3 Other Battery Types

- 5.2 By End-User

- 5.2.1 Automotive

- 5.2.2 Data Centers

- 5.2.3 Telecommunication

- 5.2.4 Energy Storage

- 5.2.5 Other End-Users

- 5.3 By Geography

- 5.3.1 Indonesia

- 5.3.2 Malaysia

- 5.3.3 Philippines

- 5.3.4 Singapore

- 5.3.5 Thailand

- 5.3.6 Vietnam

- 5.3.7 Myanmar

- 5.3.8 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd.

- 6.3.2 C&D Technologies Inc.

- 6.3.3 East Penn Manufacturing Co. Inc.

- 6.3.4 Tianjin Lishen Battery Joint-Stock Co. Ltd.

- 6.3.5 Exide Industries Ltd.

- 6.3.6 FIAMM Energy Technology SpA

- 6.3.7 GS Yuasa Corporation

- 6.3.8 LG Chem Ltd.

- 6.3.9 Panasonic Corporation

- 6.3.10 Saft Groupe SA

- 6.3.11 Samsung SDI Co. Ltd.

- 6.3.12 Clarios

- 6.3.13 Tesla Inc.

- 6.3.14 Leoch International Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.