PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044195

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044195

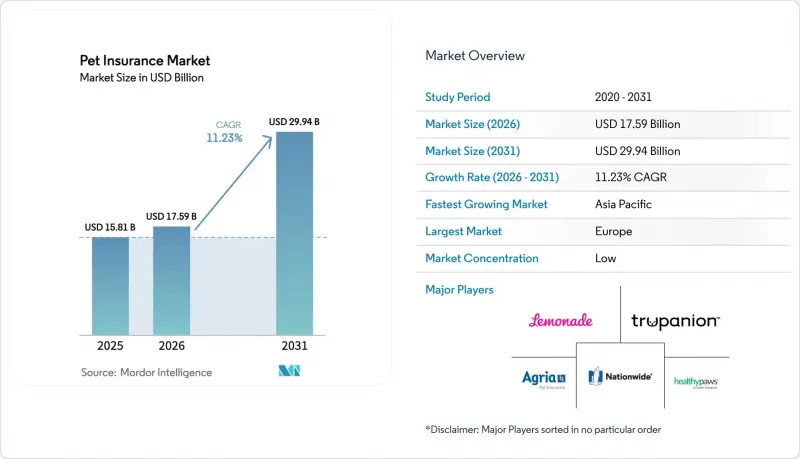

Pet Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Pet Insurance Market size is projected to expand from USD 15.81 billion in 2025 and USD 17.59 billion in 2026 to USD 29.94 billion by 2031, registering a CAGR of 11.23% between 2026 to 2031.

Penetration diverges widely across markets, with Sweden having near universal coverage among dogs, while the United States remains in the low single digits for companion animals, yet the gap in veterinary cost inflation versus general inflation keeps demand resilient as owners seek predictable budgeting for care. Pet owners spend a large share of their budgets on veterinary care, but cost sensitivity leads some to delay or skip visits. This creates opportunities for pet insurance, as many pets remain uninsured and owners seek ways to manage unexpected expenses. Veterinary services account for about 32% of household pet spending, and rising costs are influencing care utilization and preventive care engagement. Embedded distribution at the point of care and retail checkout reduces friction by presenting coverage offers at moments of high intent, while employer-sponsored voluntary benefits broaden access without adding cost to benefit budgets. Insurers and insurtechs deploy automation to compress underwriting and adjudication cycles, with large language models and straight-through processing lowering loss-adjustment expenses and improving customer experience at scale.

Global Pet Insurance Market Trends and Insights

Rising Pet Adoption and Pet Humanization Trend

United States pet ownership remains elevated and continues to expand in 2026, with approximately 94 million households owning at least one pet, as younger households add dogs and cats at a faster rate and sustain higher per-pet spending than older cohorts. The dog population reached about 87.3 million and the cat population about 76.3 million in 2025, reflecting both growth and the narrowing gap between species. Pet owners increasingly treat pets as family members, spending an average of USD 1,700 per household annually on pet-related expenses, with veterinary services accounting for about 32% of these expenditures . This mindset drives prioritization of premium foods, preventive care, and timely specialist interventions, supporting consistent veterinary utilization even when budgets tighten, which preserves demand for insurance coverage that caps exposure to surprise bills and smooths cash flows across a pet's lifespan. While insurance adoption in the United States still trails sentiment, steady gains in awareness and digital purchase journeys are narrowing the gap with more mature European markets. Insights from Japan further demonstrate that higher penetration and convenient direct-settlement options can accelerate uptake when owners perceive clear value at the point of care.

Escalating Veterinary Costs Outpacing CPI

Veterinary prices have risen faster than general inflation, putting pressure on household budgets and intensifying the need to manage the volatility of medical bills for pets. Practices face wage inflation and higher costs for advanced diagnostics, which raises fee schedules at large chains and independent clinics alike. The result is a measurable decline in routine wellness visits among some segments as owners defer care, coupled with a rise in emergency episodes that carry higher costs and create stress for uninsured households. Insurers absorb these pressures through pricing and product design, while households with constrained liquidity report rising anxiety around unexpected invoices and increasing difficulty meeting pet-related expenses. Select carriers have adjusted portfolios to address high-cost segments and rebalance risk exposure, which aligns underwriting with observed cost trends as veterinary services expand their share of total pet spending.

High Premium Inflation Versus Disposable Income

Premium adjustments respond to rising veterinary costs, and some consumers face affordability constraints that lead to policy lapses and delayed care decisions. Select carriers disclosed price increases to keep pace with claim severity, while monitoring retention and new business quality to avoid adverse selection that erodes risk pools. Demand elasticity emerges in lower-income segments as owners ration wellness visits, which in turn can increase emergency episodes and worsen health outcomes for uninsured pets. Households report higher financial stress tied to pet care, including balances carried for veterinary bills and constraints that limit the ability to pay premiums regularly. Carriers continue to refine product design and discounts to cushion the impact on price-sensitive segments while preserving coverage breadth in the pet insurance market.

Other drivers and restraints analyzed in the detailed report include:

- NAIC Model Act Rollout and Regulatory Advancements

- Embedded Insurance in Pet-Care Ecosystems

- Lack of Unified Global Veterinary Procedure Coding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accident & Illness led with 82.36% of the pet insurance market share in 2025, while Wellness and Preventive-Care add-ons are forecast to expand at a 15.39% CAGR through 2031. Accident & Illness coverage accounted for the largest policy-type share in 2025, reflecting owner preference for broad protection against injuries and diseases, and Wellness and Preventive-Care add-ons are projected to grow the fastest through 2031 as routine care gets bundled with catastrophic coverage. This pattern supports higher retention as reimbursement for exams, and vaccines sustain frequent touchpoints and normalize filing claims during the policy year. Clear separation between insurance and wellness plans under the United States model reforms improves disclosure and avoids confusion when customers compare products with similar names but different coverage scopes. The pet insurance market benefits when wellness riders lift perceived value for monthly premiums, especially for younger pets that file routine claims even if major incidents are rare in early years. As embedded retail and clinic channels expand, packaging wellness at checkout or intake increases conversion in the pet insurance market by aligning financial protection with immediate care needs.

Accident-only policies remain a niche for price-sensitive owners and older pets that no longer qualify for comprehensive underwriting, yet the momentum resides with combined Accident & Illness plus wellness bundles that meet both preventive and unexpected needs. Direct links with veterinary information systems shorten reimbursement cycles and improve customer satisfaction, which in turn raises renewal rates for plans that deliver visible value at each visit. Carriers also refine deductibles and annual limits to better match expected spend by age and breed, making core packages more competitive at the point of comparison. Embedded partnerships with major retailers and clinics provide marketing scale and trusted environments for upsell to wellness-enhanced options, where engagement is higher, and cancellations are lower. With these trends, the pet insurance industry continues to shift from standalone catastrophic policies toward integrated health and wellness propositions that strengthen lifetime value for both customers and carriers.

Dogs captured 74.82% of the pet insurance market share in 2025, and other pets recorded the fastest momentum with a 13.95% CAGR projected to 2031. Dogs represent the majority of insured pets and policy revenue in 2025 and remain the primary focus for product design given their higher clinical complexity and per-policy premiums relative to cats. Feline penetration is rising as cat ownership grows among younger urban households, though per-policy economics differ due to lower visit frequency and claim severity. Exotics and other pets are projected to expand from a smaller base as select carriers extend underwriting to avian and small-mammal species, which requires specialized clinical knowledge and tailored coverage language. The pet insurance market experiences steady growth in canine policies as breed-specific risks shape pricing ladders and as owners prioritize comprehensive protection for orthopedic and hereditary conditions. Over time, better data on feline chronic conditions and indoor-lifestyle risk will support more precise segmentation and messaging that raise take-up among cat owners.

Dog-heavy books of business tend to scale faster, and investments in claims automation and direct payment at clinics can remove friction and boost satisfaction metrics for canine and feline owners alike. Product education remains important for exotics since coverage features need to reflect species-specific conditions, and underwriting must account for different morbidity profiles. The pet insurance market responds to these dynamics by adjusting distribution, content, and plan builders to match the expectations and budgets of each owner segment. Partnerships with specialty clinics and associations in exotics can improve product credibility and accelerate adoption among enthusiasts who know their species' care requirements well. As data on cross-species outcomes improves, carriers can refine benefits and price points that align risk and value across dogs, cats, and other pets in the pet insurance market.

The Pet Insurance Market Report is Segmented by Policy Type (Accident & Illness, Accident-Only, and More), Animal Type (Dog, Cat, and More), Provider Type (Traditional, Insurtech/Digital Providers, and More), Sales Channel (Direct-To-Consumer, Intermediated, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe holds the largest regional position with 45.23% share in 2025, driven by a long-standing insurance-buying culture, high veterinary cost baselines, and consistent consumer familiarity with claims processes and benefits. The United Kingdom sustains elevated penetration as veterinary bills and standardized policy terms keep coverage relevant to households, while Sweden's historically high participation reflects a cultural norm around responsible ownership that includes financial protection. Product clarity has improved in major European markets alongside consumer protection initiatives, which helps owners compare reimbursement levels and exclusions when choosing plans. Embedded partnerships across retail and clinic networks strengthen attachment rates at checkout and in appointment flows and support ongoing migration from intermediated models. With higher awareness and stable regulatory frameworks, Europe remains the anchor of the pet insurance market while new channels expand reach into underpenetrated segments.

North America ranks second by revenue and continues to grow as awareness rises and product experiences become faster and simpler through digital claims and direct payment with select providers. Written premiums expanded in 2025 on the back of higher enrollments and premium normalization to veterinary costs, though penetration varies sharply by state and urban density. The model law adoption across multiple states improves clarity on pre-existing conditions, waiting periods, and wellness programs, which reduces friction at renewal and supports retention. Employer channels add momentum by making payroll deduction available for voluntary coverage, while retail and clinic partners integrate quotes directly into point-of-sale and appointment workflows. The pet insurance market in North America benefits from operational advances like instant adjudication and hybrid AI-human claims models, which compress payout cycles and improve customer satisfaction.

Asia-Pacific is the fastest-growing region with a projected 14.89% CAGR through 2031, supported by urbanization, rising disposable incomes, and digital-first distribution that lowers barriers to enrollment. Japan's direct-settlement infrastructure and wellness innovation create a blueprint for convenience and preventive outcomes that other markets seek to emulate as penetration increases. Australia, China's tier-one cities, and select Southeast Asian markets are building on mobile-native behaviors and embedded digital ecosystems to introduce coverage at scale. As EHR adoption and standardized claims data improve, underwriting precision will increase and support more tailored offerings by breed and age across the region. Together, these shifts reinforce Asia-Pacific's role as the global growth engine for the pet insurance market while Europe anchors total revenue and North America gains on improving awareness and product experience.

- Trupanion Inc.

- Nationwide (VPI)

- Anicom Holdings Inc.

- Embrace Pet Insurance Agency LLC

- Figo Pet Insurance LLC

- Hartville Group (ASPCA)

- Healthy Paws Pet Insurance LLC

- Lemonade Inc.

- ManyPets Ltd.

- Agria Djurforsakring AB

- RSA Group (MORE THAN)

- Petplan (Fetch)

- Pets Best Insurance Services LLC

- MetLife Pet Insurance (PetFirst)

- Dotsure.co.za

- Oneplan (South Africa)

- PetSure (Australia)

- iPet Insurance (Japan)

- Chewy / Trupanion Pet-Partner Plans

- Pumpkin Pet Insurance (Zoetis)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising pet adoption & pet-humanization trend

- 4.2.2 Escalating veterinary costs outpacing CPI

- 4.2.3 NAIC Model Act rollout & regulatory advancements

- 4.2.4 Embedded insurance in pet-care ecosystems (retailers, wellness apps)

- 4.2.5 Employer-sponsored pet-benefit programs

- 4.2.6 AI-driven dynamic underwriting & real-time claims automation

- 4.3 Market Restraints

- 4.3.1 High premium inflation vs. disposable income

- 4.3.2 Lack of unified global veterinary procedure coding

- 4.3.3 Insurer policy adjustments triggered by adverse loss ratios in certain breeds

- 4.3.4 Low awareness & cultural barriers in emerging markets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Policy Type

- 5.1.1 Accident & Illness

- 5.1.2 Accident-Only

- 5.1.3 Wellness / Preventive-Care Add-ons

- 5.1.4 Others

- 5.2 By Animal Type

- 5.2.1 Dog

- 5.2.2 Cat

- 5.2.3 Other Pets (Birds, Exotics, Equine, etc.)

- 5.3 By Provider Type

- 5.3.1 Traditional (Private / Mutual / Cooperative Insurers)

- 5.3.2 Insurtech / Digital Providers

- 5.3.3 Niche (Government-linked / Public Schemes / Other)

- 5.4 By Sales Channel

- 5.4.1 Direct-to-Consumer

- 5.4.2 Intermediated

- 5.4.3 Embedded

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.3.7 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Trupanion Inc.

- 6.4.2 Nationwide (VPI)

- 6.4.3 Anicom Holdings Inc.

- 6.4.4 Embrace Pet Insurance Agency LLC

- 6.4.5 Figo Pet Insurance LLC

- 6.4.6 Hartville Group (ASPCA)

- 6.4.7 Healthy Paws Pet Insurance LLC

- 6.4.8 Lemonade Inc.

- 6.4.9 ManyPets Ltd.

- 6.4.10 Agria Djurforsakring AB

- 6.4.11 RSA Group (MORE THAN)

- 6.4.12 Petplan (Fetch)

- 6.4.13 Pets Best Insurance Services LLC

- 6.4.14 MetLife Pet Insurance (PetFirst)

- 6.4.15 Dotsure.co.za

- 6.4.16 Oneplan (South Africa)

- 6.4.17 PetSure (Australia)

- 6.4.18 iPet Insurance (Japan)

- 6.4.19 Chewy / Trupanion Pet-Partner Plans

- 6.4.20 Pumpkin Pet Insurance (Zoetis)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment