PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689783

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689783

Rooftop Solar Photovoltaic Installation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

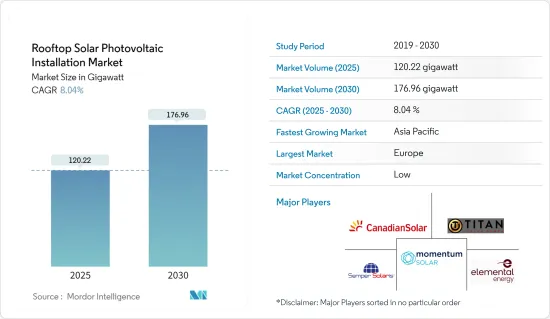

The Rooftop Solar Photovoltaic Installation Market size is estimated at 120.22 gigawatt in 2025, and is expected to reach 176.96 gigawatt by 2030, at a CAGR of 8.04% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Over the long term, supportive government policies in the form of incentives and tax benefits for solar panel installation, declining PV installation costs, and rising panel efficiencies are expected to drive the market during the forecast period.

On the other hand, high initial capital investment are expected to hinder the growth of the market during the forecasted period.

Nevertheless, new technological advancements and the development of perovskite solar cells are expected to create several opportunities for the rooftop solar PV installation market in the future.

Asia-Pacific was the largest market for rooftop solar PV installation in 2022. The region is also likely to be the fastest-growing market during the forecast period due to the presence of several developing economies, such as China and India.

Rooftop Solar Photovoltaic Installation Market Trends

Residential Rooftop Installation Expected to Dominate the Market

- The residential segment includes individual houses and residential building complexes. Residential rooftop-mounted systems are small compared to commercial and industrial rooftop systems. The residential rooftop solar PV system typically has a capacity range of up to 50 kW.

- The deployment of residential rooftop solar PV systems has increased significantly in recent years worldwide, owing to the declining costs and the government's supportive policies. Residential rooftop solar PV installations can be arranged in smaller configurations for mini-grids or personal use. There is a rise in demand for residential rooftop systems from various countries where residents need accessible, affordable, and reliable electricity options. In many countries, the electricity generated from solar PV is more economically attractive than buying electricity from the grid.

- For instance, in the past couple of years, the United States experienced rapid growth in residential rooftop solar installed capacity; according to the Solar Energy Industries Association, the residential rooftop solar PV installed capacity grew by around 40% between 2021 and 2022. In 2022, the annual installed capacity was 5.9 GW compared to 4.2 GW in 2021.

- Further, In 2022, the average cost of residential solar systems in the United States stood at USD 3.21 per watt. Although the price of residential solar has slightly increased in the last three years, it is still less than half the average cost registered in 2010. The decrease in the cost of residential solar systems has contributed to the significant increase in the solar capacity installed in United States households across the country.

- The European Union is actively promoting the domestic production of solar panels, exemplified by initiatives such as Enel Green Power's collaboration with the European Union to expand a solar panel Gigafactory located in Italy. Supported by European Union funding, Enel Green Power aims to increase its production capacity by a significant factor, specifically fifteen-fold, from the existing 200 MW to a substantial 3 GW. Anticipated to be operational by July 2024, this production facility represents a considerable investment totaling approximately USD 630 million, with an expected contribution from the European Union of around USD 124 million. This concerted effort is poised to drive down the cost of rooftop solar panels in the near term and to stimulate heightened demand for residential rooftop solar systems throughout Europe. The need for residential rooftops has increased in countries such as China, India, and Australia in the past couple of years due to government initiatives to promote solar energy projects in the residential sector and reduce installation costs.

- For instance, the Government of India initiated phase II of the Ministry of New and Renewable Energy's (MNRE) grid-connected rooftop solar program. Under this program, in April 2022, the Tamil Nandu Energy Development Agency issued a tender to install 12 MW of grid-connected residential rooftop solar systems in Tamil Nandu. Similarly, Telangana state's Renewable Energy Department Corporation invited bids to appoint suppliers to build 50 MW of grid-connected residential rooftop solar projects.

- Therefore, owing to the above points, the residential rooftop solar PV installation market is expected to dominate during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Rapid urbanization, population growth, and industrialization across Asia-Pacific countries have fueled a substantial rise in electricity consumption. In response, governments and businesses are increasingly turning to rooftop solar PV installations as a viable means to augment energy supply while addressing environmental concerns.

- Moreover, the Asia-Pacific region offers an abundance of sunlight, making it exceptionally conducive to solar energy generation. The favorable climatic conditions and technological advancements in solar panel efficiency ensure optimal energy yield from rooftop installations. This natural advantage bolsters the region's attractiveness and viability of solar PV installations.

- China is home to nearly all the largest solar photovoltaic (PV) manufacturing companies and facilities globally, with almost 70% of the global solar PV manufacturing capacity in China. These companies also dominate other businesses, such as polysilicon, ingot, and wafer-making, which are integral to the solar panel supply chain. This extraordinary control of the global solar PV supply chain puts Chinese manufacturers at a more significant advantage when compared to solar equipment manufacturers from other countries.

- Furthermore, proactive government policies and incentives play a pivotal role in propelling Asia-Pacific to the forefront of the rooftop solar PV market. Governments across the region have implemented robust support mechanisms, including feed-in tariffs, tax credits, and regulatory frameworks that encourage the adoption of rooftop solar PV systems. These incentives reduce the financial burden on consumers and businesses, stimulating rapid market growth.

- In June 2022, the Australian government released new rooftop solar PV regulations. The government committed USD 19.2 million in the 2021-22 budget to reform the SRES (Small-scale Renewable Energy Scheme). The amendment regulations aim to protect consumers better and improve integrity in the rooftop solar sector. The amendments are as follows:

- Streamline reporting requirements for installers, solar retailers, and manufacturers. Allow the Regulator to take a more direct role in setting the conditions for solar PV components eligible for small-scale technology certificates. Such mandates are expected to see a massive rise in rooftop solar PV adoption during the forecast period.

- Therefore, owing to the above points, Asia-Pacific is expected to dominate the rooftop solar PV installation market during the forecast period.

Rooftop Solar Photovoltaic Installation Industry Overview

The rooftop solar installations market is consolidated in nature. Some of the key players in the market (in no particular order) include Titan Solar Power NV Inc, Momentum Solar, Canadian Solar Inc., Elemental Energy Inc., and Semper Solaris Construction Inc, and among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Rooftop Solar Photovoltaic (PV) Installed Market in GW, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Solar Panel Costs

- 4.6.1.2 Supportive Government Policies

- 4.6.2 Restraints

- 4.6.2.1 High Upfront Cost

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Residential

- 5.1.2 Commercial and Industrial

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Asia-Pacific

- 5.2.2.1 China

- 5.2.2.2 India

- 5.2.2.3 Australia

- 5.2.2.4 Japan

- 5.2.2.5 Malaysia

- 5.2.2.6 Thailand

- 5.2.2.7 Indonesia

- 5.2.2.8 Vietnam

- 5.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Spain

- 5.2.3.4 Italy

- 5.2.3.5 France

- 5.2.3.6 Nordic Countries

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 South Africa

- 5.2.5.5 Egypt

- 5.2.5.6 Nigeria

- 5.2.5.7 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Titan Solar Power NV Inc.

- 6.3.2 Momentum Solar

- 6.3.3 Canadian Solar Inc.

- 6.3.4 Elemental Energy Inc.

- 6.3.5 Semper Solaris Construction Inc.

- 6.3.6 Pink Energy

- 6.3.7 ReVision Energy LLC

- 6.3.8 ADT Solar

- 6.3.9 Baker Electric Home Energy

- 6.3.10 Infinity Energy Inc.

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technological Advancements and the Development of Perovskite Solar Cells