PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690129

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690129

Debt Collection Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

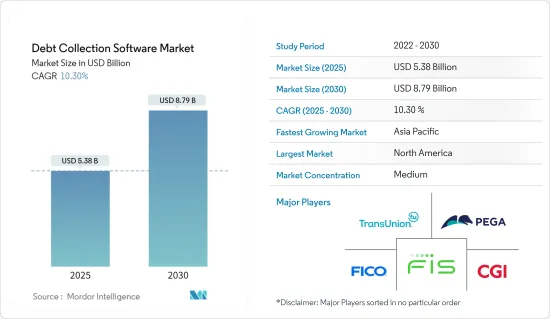

The Debt Collection Software Market size is estimated at USD 5.38 billion in 2025, and is expected to reach USD 8.79 billion by 2030, at a CAGR of 10.3% during the forecast period (2025-2030).

Key Highlights

- The growth of the market is majorly attributed to the increasing automation in the debt collection process, such as personalizing customer experience through the integration of AI and ML, Continuous innovations to meet consumer demand, predicting default probability through automation, and outsourcing debt recovery to specialized debt collection agencies.

- The most significant beneficiary of the technology-based banking method has been the digital lending market. Data-driven technology, machine learning, and other commitments are critical elements in the evolution of digital lending from traditional paperwork and formalities. Models such as P2P lending, SME financing, short-term loans, and credit cards generate a digital loan market.

- Companies can target their loans to customers due to the availability of large amounts of customer data, one of the most significant growth drivers in the digital lending sector. Further, compared to other business models in the field of fintechs, such as payments and finance services, digital lending offers greater margins.

- Digitization has become a necessity for banks in view of the growing demand for credit, increased awareness of financial matters, and an expectation that the process will go smoothly. The growth of digital lending is analyzed to create significant borrower data and other data that could be used efficiently in the debt collection software. A practical solution to automating the collection process is using debt collection software or collections CRM that allows lenders to track and follow up with debtors efficiently, predict and prioritize debt recovery, and enable faster collections. This is analyzed to boost the market's growth rate during the forecast period.

- The management of debt collection activities has been significantly hindered by legacy systems, which can be described by out-of-date technology, restricted functionality, and inflexible architecture. These limitations have driven the debt collection software market to witness a surge in demand for modern, agile, and adaptable solutions capable of addressing the evolving complexities of debt management.

- Debt collection software has transformed due to the COVID-19 pandemic because lenders must adapt to the latest risk procedures, including new risk technology and risk-evaluation indicators. The need to unify various risk solutions by using AI technologies and enhance overall implementation processes has enhanced market growth post-pandemic.

Debt Collection Software Market Trends

Financial Institutions (Banks and NBFC) to Witness Growth

- Implementing debt collection software across financial institutions to reduce the banks' risk for loan defaulters by digitizing the collection operation through advanced technology and analytics-based debt collection software is fueling the market's growth by supporting the development of lenders' overall revenue and profitability.

- Additionally, the trend of banking sector priorities in lowering the NPAs has led financial organizations to understand the repayment capacity of a borrower to locate areas for high and low delinquencies, driving the market of debt collection software due to their feature of delinquency management platforms to streamline and automate the collection process in the financial sector for better collection efficiencies.

- The deployment of cloud-based debt management software due to its scalability and compatibility in integrating BFSI sectors' on-premise and cloud-hosted data sheets for analyzing debt collection patterns drives the market's growth. The back-end applications in the collections function in financial institutions are increasingly using cloud technologies, advanced analytics, artificial intelligence (AI), machine learning (ML) techniques, and ready-to-consume application programming interfaces (APIs) for better reliability and accuracy in designing collection strategy for the loans, fueling the growth of the market.

- Market vendors, such as Pegasystems and Temenos AG, are introducing a comprehensive suite of debt resolution solutions, including digital collections, debt analytics, litigation management, and a collection mobile app powered by AI-driven intelligent automation and machine learning models to manage debt collections, which is fueling the adoption of the debt collection software in the BFSIs because, through complete collection solutions available in the market, users can easily implement those solutions for better recovery efficiencies.

- For instance, in June 2023, Secure Trust Bank partnered with EXUS Software to optimize the bank's collections operations through a data-driven, zero-customization approach. The bank has planned to use this single platform to reduce the complexity of business processes, streamline all communications with customers, and gain full visibility of the complete customer journey in collections processes, which is expected to fuel market growth in the BFSI sector.

- The World Bank report stated that the domestic credit to the private sector in low and medium-income countries had increased significantly and crossed their GDP in FY 2022, which showed the increase in the amount of debt in the market and raised the demand for an automated and software-based debt collection systems in the financial institutions.

Asia-Pacific is Expected to Register Significant Growth

- The debt collection landscape in China has undergone a remarkable transformation over the past few years due to new, technology-driven approaches that offer increased efficiency and compliance in debt collection. Additionally, the market's growth over the forecast period is analyzed in light of the rising bad debts and the increasing need to automate debt collection processes in end-user industries.

- The growth of the debt collection software market in China is largely driven by the increasing demand among end-user industries to minimize bad debt and automate debt collection through advanced technology-based software. As the country's financial market continues to grow and adapt, market vendors offering innovative debt collection solutions will continue to gain significant traction in ensuring efficient, compliant, and secure debt collection processes for end-user industries.

- In India, the debt collection software market has witnessed substantial growth in recent years. It is expected to continue growing due to the significant presence of global market vendors, the emergence of new debt collection software platforms, increasing bad loans, and technological advancements in debt collection practices. Challenges associated with the current economic landscape, especially in managing debt collection across various channels, lead to operational inefficiencies and rising expenses for banks and NBFCs, necessitating the adoption of debt collection software.

- The debt collection industry in India swiftly embraced technology post-pandemic, experiencing substantial momentum. The rising demand for credit, evolving consumer preferences, and the expectation of seamless experiences have compelled lenders to adopt digitization to automate debt collection practices. This expectedly boosts the adoption of debt collection software in lending organizations, aiding lenders in saving time, costs, resources, and reputation while simultaneously improving customer experience and retention rates.

- The Rest of Asia-Pacific, including Australia, Japan, South Korea, and New Zealand, is expected to register significant growth in the debt collection software market during the forecast period. This growth is attributed to increasing digitization and the need for automated debt collection in end-user industries such as banks, collection agencies, telecom, and governments. The growing imperative to minimize bad loans, coupled with the substantial presence of both regional and global market vendors, further fuels this growth.

Debt Collection Software Industry Overview

The debt collection software market exhibits a semi-consolidated landscape, with moderate penetration due to the considerable presence of suppliers in the region. These entities are progressively engaging with various digital technology startups to introduce advanced solutions. Among the notable players in this market are Fidelity National Information Services Inc. (FIS), CGI Inc., Fair, Isaac and Company (FICO) (Constellation Software Inc.), TransUnion LLC, and Pegasystems Inc.

- June 2024: Acquired.com, a forward-looking payments firm specializing in recurring commerce, and Flexys, a prominent UK collections technology provider, proudly unveiled their collaboration. Acquired.com's primary goal is equipping enterprises, such as Flexys, with cutting-edge payment tools to streamline and enhance their payment processes. Thanks to this collaboration, Flexys has seamlessly integrated a solution, elevating the payment experience for its customers.

- March 2024: Skit.ai, a prominent player in conversational AI solutions for accounts receivables, unveiled a cutting-edge suite of self-service offerings. These are designed to not only streamline debt collection but also to enrich consumer interactions. Skit.ai's latest offerings harness generative AI technology, spanning voice, chat, email, and text channels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Debt Collection Software Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Automation in the Debt Collection Process

- 5.1.2 Outsourcing Debt Recovery to Specialized Debt Collection Agencies

- 5.2 Market Restraints

- 5.2.1 Inadequacy of Legacy Systems

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 Cloud-based

- 6.1.2 On-premise

- 6.2 By Organization Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium-sized Enterprises

- 6.3 By End User

- 6.3.1 Financial Institutions (Banks and NBFC)

- 6.3.2 Collection Agencies

- 6.3.3 Healthcare

- 6.3.4 Government

- 6.3.5 Telecom and Utilities

- 6.3.6 Other End Users (Real Estate and Retail)

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Spain

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Colombia

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fidelity National Information Services Inc. (FIS)

- 7.1.2 CGI Inc.

- 7.1.3 Fair, Isaac and Company (FICO) (Constellation Software Inc.)

- 7.1.4 TransUnion LLC

- 7.1.5 Pegasystems Inc.

- 7.1.6 Temenos AG

- 7.1.7 Intellect Design Arena Limited

- 7.1.8 Nucleus Software Exports Limited

- 7.1.9 Chetu Inc.

- 7.1.10 AMEYO (Exotel Techcom Pvt. Ltd)

- 7.1.11 EXUS Ltd

- 7.1.12 KuhleKT Pty Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET