Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690702

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690702

Liquid Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

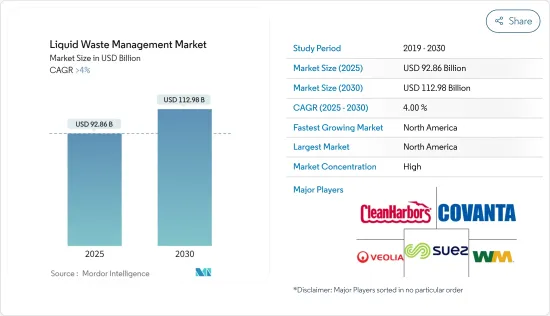

The Liquid Waste Management Market size is estimated at USD 92.86 billion in 2025, and is expected to reach USD 112.98 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic negatively impacted the market as petroleum refinery units cut their production throughput, and the demand for fuel decreased by about 30% to 40% globally during the lockdown. However, the demand for various pharmaceutical products increased during the pandemic, thereby enhancing the production of liquid wastes. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The increasing manufacturing activities that generate toxic chemicals are anticipated to enhance liquid effluent management activities. Also, the growth in the pharmaceutical and healthcare industry is expected to drive the market's growth.

- On the flip side, increasing technological challenges and stringent waste processing regulations are expected to hinder the market's growth.

- Further, the increasing focus on treating emerging contaminates is likely to provide opportunities to the market studied.

- The North American region represents the largest market, and it is also expected to be the fastest-growing market over the forecast period due to the enactment of stringent norms pertaining to the management of liquid waste and the presence of activities related to oil and gas production.

Liquid Waste Management Market Trends

Oil and Gas Segment to Dominate the Market

- The oil and gas industry is among the most profitable industries. It meets all the energy demands across various industries, households, transportation, and other sectors. The oil and gas industry is facing environmental concerns, mainly with wastewater.

- In refineries, the water consumption rate is very high for distilling crude into various fractions, such as gasoline, diesel, jet fuel, and kerosene. Several wastewater streams are coming out of refineries, which typically include desalter water generated from washing raw crude before topping, sour water from steam stripping, and fractionating that comes in contact with crude, process water generated from product washing, regenerating catalyst, and dehydrogenation reactions.

- Further, the oil and gas industry has a high water consumption rate, as it generates a large amount of wastewater in various operations, such as in hydrostatic testing water, which is consumed in the hydrostatic testing of pipelines to ensure pipeline safety and find any possible leaks. The process also includes the usage of chemical additives. Hence, hydro-test water should be treated before disposal into the sea or surface water.

- Furthermore, in the oil and gas industry, water is employed in technologies like hydraulic fracturing. In this process, high-pressure water is used to open up the cracks or fractures into the tight formations of rocks, permitting petroleum gas and unrefined petroleum to stream to a well for recovery. The water used in the process often gets contaminated, and it needs to be treated for either disposing of or reuse.

- According to the BP Statistical Review of World Energy 2022, global oil production amounted to 93.9 million barrels per day in 2022, representing an increase of 4% compared to the previous year.

- Further, China is increasing crude oil processing activities, which will be supported by following various upcoming refineries in the country. For instance, in March 2023, Saudi Aramco and its Chinese partners plan to start a full 10 USD billion refinery and petrochemical project in northeast China in 2026 to meet the country's growing demand for fuel and petrochemicals.

- Therefore, the factors above are expected to show a significant impact on the market in the coming years.

North America to Dominate the Market

- North America represents the largest market, and it is also expected to be the fastest-growing market over the period due to the enactment of stringent norms and the presence of activities related to oil and gas production.

- According to the US Energy Information Administration (EIA), crude oil production in the United States reached 12,462 thousand barrels in January 2023, compared to 12,115 thousand barrels annually in December 2022.

- Further, EIA forecasted that crude oil production in the United States will average 12.4 million barrels per day (b/d) in 2023 and 12.8 million b/d in 2024. The United States is one of the leading countries globally in terms of exploration of unconventional crude oil reserves, indicating a huge opportunity for the studied market in the country.

- Some of the liquid waste produced by the automotive industry includes used motor oil and used brake oil fluid. According to OICA, in 2022, around 10,060,339 vehicles were produced in the United States, witnessing an increasing growth rate of about 10% compared to the previous year.

- Moreover, the liquid waste management market is very well regulated by agencies like the Environmental Protection Agency (EPA) and the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH). Several laws, including the Environmental Protection Act of 1993, mentioned guidelines to be carried out by companies, including undertaking Environmental Impact Assessment (EIA) and preparing Environmental Impact Statement (EIS).

- Therefore, the aforementioned factors are expected to impact the market in the coming years significantly.

Liquid Waste Management Industry Overview

The liquid waste management market is consolidated in nature. The major players in the studied market (not in any particular order) include SUEZ, Veolia, CLEAN HARBORS, INC., Covanta Holding Corporation, and WM Intellectual Property Holdings, L.L.C., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 71005

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in the Pharmaceutical and Healthcare Industry

- 4.1.2 Increased Manufacturing Activities Containing Toxic Chemicals Leading to Growing Liquid Effluent Management

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Technological Challenges

- 4.2.2 Stringent Waste Processing Regulations

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Source

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial

- 5.2 Service

- 5.2.1 Collection

- 5.2.2 Transportation/Hauling

- 5.2.3 Disposal/Recycling

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Iron and Steel

- 5.3.3 Oil and Gas

- 5.3.4 Pharmaceutical

- 5.3.5 Textile

- 5.3.6 Other End-user Industries (Pulp and Paper, Food and Beverages, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 CLEAN HARBORS, INC.

- 6.4.2 Cleanaway

- 6.4.3 Covanta Holding Corporation

- 6.4.4 Enva

- 6.4.5 GFL Environmental Inc.

- 6.4.6 Hulsey (a Blue Flow Company)

- 6.4.7 Ovivo

- 6.4.8 REMONDIS SE & Co. KG

- 6.4.9 SUEZ

- 6.4.10 Veolia

- 6.4.11 WM Intellectual Property Holdings, L.L.C.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Rising Water Crisis Globally is Creating New Opportunities for Liquid Waste Management

- 7.2 Increasing Focus on Treating Emerging Contaminates

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.