PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406275

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406275

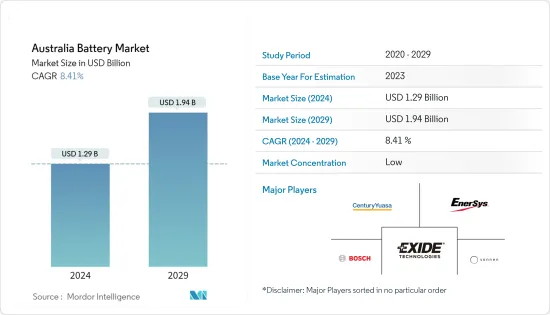

Australia Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Australia Battery Market size is estimated at USD 1.29 billion in 2024, and is expected to reach USD 1.94 billion by 2029, growing at a CAGR of 8.41% during the forecast period (2024-2029).

The Australia battery market is estimated to be at USD 1.19 billion by the end of this year and is projected to reach USD 1.79 billion in the next five years, registering a CAGR of over 8.41% during the forecast period.

Key Highlights

- Over the medium term, factors such as increasing demand from consumer electronics, electric vehicle applications, and supportive government policies are expected to drive market growth. Moreover, the increasing penetration of renewable energy is expected to increase the demand for energy storage systems, eventually driving the battery market during the forecast period.

- On the other hand, the need for more activities and development in various stages (except for mining) of the battery production supply chain, is expected to restrain the market potential during the forecast period.

- Nevertheless, new advancements in battery technologies are expected to create immense opportunities for the Australian battery market in the coming years.

Australia Battery Market Trends

SLI Battery Application to Dominate the Market

- SLI batteries are used for short power bursts, such as starting a car engine or running light electrical loads. Moreover, these batteries supply extra power when the vehicle's electrical load exceeds the supply from the charging system (alternator) and act as a voltage stabilizer in the electrical system that evens out voltage spikes, preventing them from damaging other components of the electrical system.

- SLI batteries are designed for automobiles and are always installed with the vehicle's charging system. This means a continuous cycle of charge and discharge in the battery whenever the vehicle is in use. The 12-volt batteries have been the most used for over 50 years. However, its normal voltage (while in use in the car and charged by the alternator) is close to 14 volts.

- The major factors attributing to the growth of the SLI battery market are the increasing demand for these batteries to power starter motors, lights, ignition systems, or other internal combustion engines with high performance, long life, and cost-efficiency. There are two main battery types for SLI - lead-acid and lithium-ion batteries.

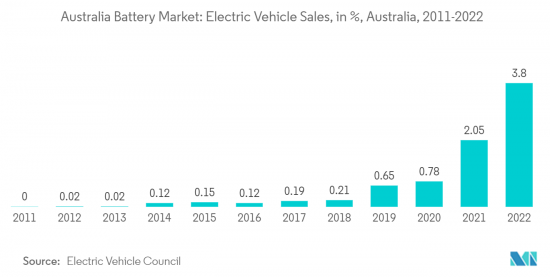

- According to Electric Vehicle Council statistics, in 2022, electric vehicle sales in Australia witnessed a significant growth of about 3.8% compared to the previous year. Such increasing EV sales are anticipated to drive the demand for SLI batteries.

- In Australia, the lead-acid battery is the technology of choice for all SLI applications in conventional combustion engine vehicles, such as cars and trucks. Lead-acid batteries are the most economically viable mass-market technology for SLI applications in traditional vehicles, including those with start-stop and basic micro-hybrid systems, owing to their excellent cold-cranking performance, reliability, and low cost. All automotive SLI batteries are lead-acid based and over 90% (by storage capacity) of industrial stationary and motive applications.

- According to the Federal Chamber of Automotive Industries (FCAI), 1,081,429 vehicles were delivered during 2022, up by 3%, compared to 2021, when 1,049,831 vehicles were sold. This was attributed to the entry of new automotive brands and models into the market. For instance, the fourth quarter of 2022 was headlined by a new product onslaught for Japanese rivals Toyota and Nissan, with updates to Australia's most popular vehicles - the Toyota HiLux, RAV4, Corolla, and Camry - and the all-new Nissan Qashqai, X-Trail, and Pathfinder SUVs, increasing demand for SLI batteries in Australia.

- Therefore, based on the abovementioned factors, the SLI battery application is expected to dominate the Australian battery market during the forecast period.

Large Domestic Reserves of Battery Metals Expected to Drive the Market

- Australia is naturally gifted with enormous mineral wealth. The country has one of the largest reserves of metals, such as lithium, nickel, and cobalt, which are critical for producing and manufacturing modern batteries. Australia has historically had a strong mining industry, and the proper extraction, enrichment, and utilization of these vast reserves of rare earth metals are expected to drive the Australia Battery market during the forecast period.

- According to the United States Geological Survey data, Australia has the 2nd largest cobalt reserves globally but accounts for only 4% of the global production of cobalt. However, most of the world's cobalt production comes from DR Congo, and most of the mines in Congo are owned by Chinese mining companies. Moreover, many ethical and environmental concerns exist, such as forced labor and child exploitation regarding mining in DR Congo. Due to this, many North American and European battery manufacturers are trying to diversify their supply chain by signing strategic agreements with Australian mining companies to secure their cobalt supply.

- In April 2023, Dreadnought Resources secured two Exploration Incentive Scheme (EIS) co-funded drilling grants for its Mangaroon Rare Earth Elements (REEs) and Tarraji-Yampi Copper-Silver-Gold-Cobalt (Cu-Ag-Au-Co) Projects in Western Australia. As part of the EIS grant awarded by the Western Australian government, each project will likely receive USD 220,000 to fund exploration.

- Australia is also the world's largest producer and exporter of lithium. Lithium is the most important component for manufacturing batteries for energy storage and electric vehicles. Most of the lithium is exported as spodumene concentrate, which requires further processing. Several Australian mining companies are starting to collaborate with foreign companies to commercially set up lithium extraction and enrichment plants to produce battery-grade lithium in Australia.

- In May 2023, Indian iron-ore merchant miner NMDC announced that it is planning to partner with Australian miners and prospecting agencies for lithium mining. It is also in talks with the Australian government to take up mines as and when they come up.

- In May 2023, Core Lithium received approval for early works at the BP33 underground mine at its Finniss lithium project in the Northern Territory. Early works funding of USD 40-50 million has been approved for BP33, along with the necessary mine authorization approvals.

- Therefore, these large-scale lithium refining projects are expected to strengthen Australia's domestic battery supply chain and drive the Australian battery market during the forecast period.

Australia Battery Industry Overview

The Australian battery market is fragmented. Some of the major players include Century Yuasa Batteries Pty Ltd, Enersys Australia Pty Ltd., Robert Bosch (Australia) Pty Ltd., Exide Technologies, and Sonnen Australia Pty Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand from EV Sector

- 4.5.1.2 Supportive Government Policies

- 4.5.2 Restraints

- 4.5.2.1 Lack of Development in Battery Production Supply Chain

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Li-Ion Battery

- 5.1.2 Lead-acid Battery

- 5.1.3 Other Technologies

- 5.2 Application

- 5.2.1 SLI Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.))

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Automotive Batteries (HEV, PHEV, EV)

- 5.2.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Century Yuasa Batteries Pty Ltd.

- 6.3.2 Enersys Australia Pty Ltd.

- 6.3.3 Robert Bosch (Australia) Pty Ltd.

- 6.3.4 Exide Technologies

- 6.3.5 VARTA AG

- 6.3.6 Sonnen Australia Pty Limited

- 6.3.7 Soluna Australia Pty Ltd.

- 6.3.8 Battery Energy Power Solutions Pty

- 6.3.9 R & J Batteries Pty Ltd.

- 6.3.10 PMB Defence

- 6.3.11 East Penn Manufacturing Company

- 6.3.12 Energy Renaissance Pty Ltd.

- 6.3.13 Crystal Solar Energy

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Advancements in Battery Technologies