Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644400

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644400

India Coal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

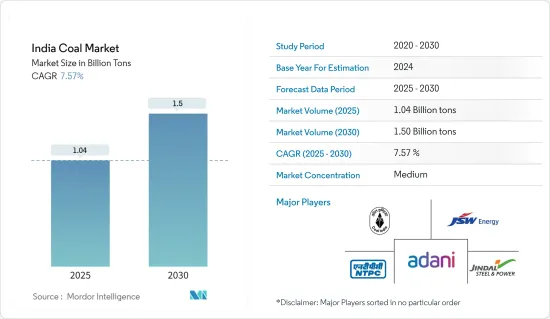

The India Coal Market size is estimated at 1.04 billion tons in 2025, and is expected to reach 1.50 billion tons by 2030, at a CAGR of 7.57% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing power generation capacity plans and increasing electricity demand and rapidly growing industrial and infrastructural development activities, are expected to be one of the most significant drivers for the India coal market during the forecast period.

- On the other hand, supportive government policies to increase renewable energy generation is expected to restrain the growth of the Indian coal market during the forecast period.

- Nevertheless, availability of lignite resources in three states: Tamil Nadu, which accounts for 79% of lignite resources, Rajasthan, and Gujarat. Most of the resources are untapped, and the mining of lignite sources is expected to create several opportunities for the market players.

India Coal Market Trends

Increasing Thermal Power Generation is Expected to Drive the Market

- Coal is extensively used in India to fire thermal power stations and, in turn, meet the demand for various sectors, such as industry, transport, residential, commercial, and public services. The power stations segment is expected to dominate the market, supported by India's plan to add additional coal-fired plants during the forecast period.

- Coal-fired power plants generate energy from the combustion of coal. The country is the second-largest coal producer globally and uses most coal to produce electricity. According to the India Ministry of Coal statistics, as of July 2023, the country imported 87.97 million tonnes of coal, moreover, the total coal imports registered 237.67 million tonnes in 2022-23.

- In April 2023, India's total coal installed generation capacity was 205 GW, which accounted for 49.3 % of the full installed power generation capacity. The increased consumption of coal exhibits the growing usage of coal in the country. Coal is abundant and economical for the country and is widely used by power-generating companies.

- The Ministry of Power in India is plplansommission Patratu Super Thermal Project by the end of 2022. The project is located in Jharkhand and can produce 4000 megawatts (MW) of coal-fired power. For India, coal has been a significant source of power generation in the past and still holds a considerable share in the country's power generation industry. This is expected to positively impact the thermal power plant market in the country.

- Moreover, the country plans to commission the Uppur Thermal Power Project located in Ramanathapuram, Tamilnadu, with a capacity of 1600 MW by 2023. The project is owned by Tamil Nadu Generation and Distribution Corporation Ltd (TANGEDCO) and has an investment cost of USD 1.7 billion.

- Hence, owing to the above points, increasing thermal-based power generation projects are expected to drive the Indian Coal Market during the forecast period.

Supportive Government Policies for Renewables is Expected to Restrain the Market

- The Indian government has introduced numerous supportive policies to increase the renewable energy installed capacity to 450 GW by 2030. Since the utilization of coal leads to air pollution linked with health disorders, the government is actively promoting renewables to reduce coal usage.

- According to International Renewable Energy Agency, the total renewable energy installed capacity raised to 162.96 GW in 2022, with an annual growth rate of 10.8% compared to the previous year.

- As part of the Paris Climate Agreement, India has committed to install 40% of its electricity generation capacity from non-fossil fuels by 2030. To achieve this goal, India has set an ambitious target of setting up 1,75,000 MW of renewable energy capacity, including 1,00,000 MW of solar power, by 2022. Further, a target of 4,50,000 MW installed RE capacity by 2030 has also been fixed, and this, in turn, culminates in the reduction in the usage of coal across the country

- Some other schemes implemented by the Ministry of New and Renewable Energy (MNRE) in the last three years are the Solar Park Scheme, the 300 MW defense Scheme, and the 500 MW of VGF (Viability Gap Funding) Scheme. In January 2020, India made an ambitious target of having 450 GW of renewable energy by 2030.

- Owing to the above factors increasing renewables with supportive government policies is expected to hamper the growth of the Indian Coal Market in the forecast period.

India Coal Industry Overview

The India coal market is semi-consolidated. Some of the major players in the market (in no particular order) include Adani Group, Coal India Limited, JSW Energy Ltd, NTPC Ltd, and Jindal Steel & Power Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 71557

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, until 2028

- 4.3 Energy Mix, 2022

- 4.4 Coal Prices, 2011-2022

- 4.5 Coal Porduction in India, in Tonnes, 2011-2022

- 4.6 Coal Imports, 2015-2022

- 4.7 Statewise Coal Production, India, 2022

- 4.8 Recent Trends and Developments

- 4.9 Government Policies and Regulations

- 4.10 Market Dynamics

- 4.10.1 Drivers

- 4.10.1.1 Increasing Power Generation Capacity Plans and Increasing Electricity Demand

- 4.10.1.2 Rapidly Growing Industrial and Infrastructural Development Activities

- 4.10.2 Restraints

- 4.10.2.1 Coal Substituted with Clean Energy Sources

- 4.10.1 Drivers

- 4.11 Supply Chain Analysis

- 4.12 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Power Generation (Thermal Coal)

- 5.1.2 Coking Feedstock (Coking Coal)

- 5.1.3 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 NLC India Ltd

- 6.3.2 JSW Energy Limited

- 6.3.3 Singareni Collieries Company Limited (SCCL)

- 6.3.4 NTPC Ltd

- 6.3.5 Jindal Steel & Power Ltd

- 6.3.6 Adani Power Ltd

- 6.3.7 Coal India Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Untapped Mining Lignite Sources

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.