PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687824

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687824

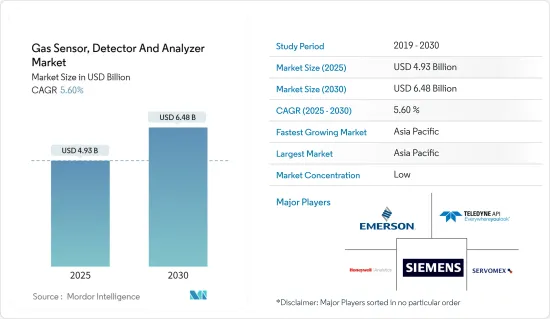

Gas Sensor, Detector And Analyzer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Gas Sensor, Detector And Analyzer Market size is estimated at USD 4.93 billion in 2025, and is expected to reach USD 6.48 billion by 2030, at a CAGR of 5.6% during the forecast period (2025-2030).

Gas sensors are chemical sensors that can measure the concentration of a constituent gas in its vicinity. These sensors embrace different techniques for quantifying a medium's exact amount of gas. A gas detector measures and indicates the concentration of certain gases in the air via other technologies. These are characterized by the type of gases they can detect in the environment. Gas analyzers find applications across safety instruments used in multiple end-user industries to maintain adequate safety in the workplace.

Key Highlights

- The global demand for gas analyzers has been boosted by an increase in shale gas and tight oil discoveries since these resources are utilized to stop corrosion in the infrastructure of natural gas pipelines. The use of gas analyzers has also been enforced in several industrial settings by government law and the enforcement of occupational health and safety rules. The growing public consciousness of the dangers of gas leaks and emissions contributed to the increased adoption of gas analyzers. Manufacturers are integrating gas analyzers with mobile phones and other wireless devices to offer real-time monitoring, remote control, and data backup.

- Gas leaks and other unintentional contamination can result in explosive consequences, physical harm, and fire risk. In confined spaces, numerous hazardous gases can even asphyxiate workers in the vicinity by displacing oxygen, which results in death. These outcomes jeopardize employee safety and the safety of equipment and property.

- Handheld gas detection tools keep personnel safe by monitoring a user's breathing zone while stationary and moving. These devices are critical in many situations where gas risks may exist. It is essential to monitor the air for oxygen, combustibles, and poisonous gases to ensure the safety of all people. Handheld gas detectors include built-in sirens that alert workers to potentially hazardous situations within an application, such as a confined space. When an alert is triggered, a large, easy-to-read LCD verifies the concentration of dangerous gas or gases.

- The production costs for gas sensors and detectors have steadily risen due to recent technological changes. While the market incumbents have been able to adapt to these changes, new entrants and mid-range manufacturers face considerable challenges.

- With the onset of COVID-19, multiple end-user industries in the market studied have been affected by reduced operations, temporary factory closures, etc. For instance, in the renewable energy industry, significant concerns revolve around global supply chains, which are considerably slowing down production, thus, aiming at reduced spending for new measurement systems and sensors. The detection and monitoring of hydrogen sulfide (H2S) and carbon dioxide (CO2) is pertinent in natural gas processing, creating significant demand for gas analyzers.

Gas Sensor, Detector, and Analyzer Market Trends

Oil and Gas Industry Segment is Expected to Hold Significant Market Share

- In the oil and gas industry, protecting a pressurized pipeline from corrosion and leaks and minimizing downtime are a few of the crucial responsibilities of the industry. As per a NACE (National Association of Corrosion Engineers) study, the total annual cost of corrosion in the oil and gas production industry is around USD 1.372 billion.

- The presence of oxygen in the gas sample determines a leak in the pressurized pipeline system. The continuous and undetected leak may worsen the situation while impacting on operational flow efficiency of the pipeline. Moreover, the presence of gases, such as hydrogen sulfide (H2S) and carbon dioxide (CO2), in the pipeline system reacting with oxygen can combine and form a corrosive and destructive mixture that can deteriorate the pipeline wall inside out.

- Mitigating such expensive costs is one of the drivers for adopting gas analyzers for preventive actions in the industry. Gas analyzer helps monitor leaks to extend the life of pipeline systems by effectively detecting the presence of such gases. The oil and gas industry is moving toward the TDL technique (tunable diode laser), which enables the reliability of detecting with precision because of its high-resolution TDL technique and avoids common interferences with traditional analyzers.

- As per the International Energy Agency's (IEA) June 2022, net global refining capacity is expected to expand by 1.0 million b/d in 2022 and by an additional 1.6 million b/d in 2023. With refinery gas analyzers commonly used to characterize gases produced during crude oil refining, such trends are expected to increase the market demand further.

- According to IEA, global natural gas supply increased by an estimated 4.1% globally in 2021, partly supported by the market recovery post the COVID-19 pandemic. The detection and monitoring of hydrogen sulfide (H2S) and carbon dioxide (CO2) is pertinent in natural gas processing, creating significant demand for gas analyzers.

- There are many ongoing and upcoming projects in the industry, with massive investments toward expanding production. For instance, the West Path Delivery 2023 project is expected to add about 40 km of new natural gas pipeline to the existing 25,000-km NGTL system, which ships gas across Canada and to the U.S. markets. Such projects are expected to continue during the forecast period, which will fuel the demand for gas analyzers.

Asia Pacific is Expected to Hold Significant Market Share

- Increased investments in new plants in oil and gas, steel, power, chemical, and petrochemicals and the rising adoption of international safety standards and practices are expected to influence market growth. Asia Pacific is the only region to register an oil and gas capacity growth in recent years. About four new refineries were added in the area, which has added nearly 750,000 barrels per day to global crude oil production.

- The development of industries in the region is driving the growth of gas analyzers, owing to their use in the oil and gas industry, such as monitoring processes, increased safety, enhanced efficiency, and quality. Hence, the refineries in the region are deploying gas analyzers in the plants.

- During the forecast period, Asia Pacific is anticipated to be one of the fastest-growing global gas sensors market regions. This is due to a rise in strict governmental regulations and ongoing environmental awareness campaigns. Further, according to IBEF, as per the National Infrastructure Pipeline 2019-25, energy sector projects accounted for the highest share (24%) out of the total expected capital expenditure of INR 111 lakh crore (USD 1.4 trillion).

- Also, the strict government regulations have recently shown significant growth in this region. Moreover, the surge in the government's investments in smart city projects creates a significant potential for smart sensor devices, likely to impel regional Gas Sensors Market growth.

- Rapid industrialization across the different countries in the Asia Pacific region is one of the primary factors driving the growth of the gas detectors market. Smoke, fumes, and toxic gas emissions occur due to highly polluting industries such as thermal power plants, coal mines, sponge iron, steel and ferroalloys, petroleum, and chemicals. Gas detectors are commonly used to detect combustible, flammable, and toxic gases and ensure safe industrial operations.

Gas Sensor, Detector, and Analyzer Industry Overview

The gas analyzer, sensor, and detector market is fragmented due to the presence of many players worldwide. Currently, some prominent companies are developing products with applications centering on the detector. The analyzer segment has applications across clinical assaying, environmental emission control, explosive detection, agricultural storage, shipping, and workplace hazard monitoring. Players in the market are adopting strategies such as partnerships, mergers, expansion, innovation, investment, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2022 - Servomex Group Limited (Spectris PLC) extended its offerings to the Asian market by opening a new service center in Korea. As the service center is officially unveiled at Yongin, customers from the semiconductor industry, as well as the industrial process and emissions for oil and gas, power generation, and steel industry, can access invaluable advice and assistance.

- August 2022 - Emerson has announced opening a gas analysis solutions center in Scotland to help plants meet sustainability goals. The center has access to more than ten different sensing technologies that can measure more than 60 other gas components.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Safety Awareness Regarding Occupational Hazards

- 5.1.2 Proliferation of Handheld Devices

- 5.2 Market Restraints

- 5.2.1 High Costs and Lack of Product Differentiation

6 MARKET SEGMENTATION

- 6.1 Gas Analyzers

- 6.1.1 Technology

- 6.1.1.1 Electrochemical

- 6.1.1.2 Paramagnetic

- 6.1.1.3 Zirconia

- 6.1.1.4 Non-disruptive IR

- 6.1.2 End-user Industry

- 6.1.2.1 Oil and Gas

- 6.1.2.2 Chemicals and Petrochemicals

- 6.1.2.3 Water and Wastewater

- 6.1.2.4 Pharmaceuticals

- 6.1.2.5 Other End-user Industries

- 6.1.3 Geography

- 6.1.3.1 North America

- 6.1.3.2 Europe

- 6.1.3.3 Asia-Pacific

- 6.1.3.4 Latin America

- 6.1.3.5 Middle-East and Africa

- 6.1.1 Technology

- 6.2 Gas Sensor

- 6.2.1 Type

- 6.2.1.1 Toxic

- 6.2.1.1.1 Electrochemical

- 6.2.1.1.2 Semiconductor

- 6.2.1.1.3 Photoionization

- 6.2.1.2 Combustible

- 6.2.1.2.1 Catalytic

- 6.2.1.2.2 Infrared

- 6.2.2 End-user Industry

- 6.2.2.1 Oil and Gas

- 6.2.2.2 Chemicals and Petrochemicals

- 6.2.2.3 Water and Wastewater

- 6.2.2.4 Metal and Mining

- 6.2.2.5 Utilities

- 6.2.2.6 Other End-user Industries

- 6.2.3 Geography

- 6.2.3.1 North America

- 6.2.3.2 Europe

- 6.2.3.3 Asia-Pacific

- 6.2.3.4 Latin America

- 6.2.3.5 Middle-East and Africa

- 6.2.1 Type

- 6.3 Gas Detectors

- 6.3.1 Communication Type

- 6.3.1.1 Wired

- 6.3.1.2 Wireless

- 6.3.2 Type of Detector

- 6.3.2.1 Fixed

- 6.3.2.2 Portable

- 6.3.3 End-user Industry

- 6.3.3.1 Oil and Gas

- 6.3.3.2 Chemicals and Petrochemicals

- 6.3.3.3 Water and Wastewater

- 6.3.3.4 Metal and Mining

- 6.3.3.5 Utilities

- 6.3.3.6 Other End-user Industries

- 6.3.4 Geography

- 6.3.4.1 North America

- 6.3.4.2 Europe

- 6.3.4.3 Asia-Pacific

- 6.3.4.4 Latin America

- 6.3.4.5 Middle-East and Africa

- 6.3.1 Communication Type

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Emerson Electric Company

- 7.1.2 Teledyne API

- 7.1.3 Siemens AG

- 7.1.4 Servomex Group Limited (Spectris PLC)

- 7.1.5 Honeywell Analytics Inc.

- 7.1.6 Draegerwerk AG & Co KGaA

- 7.1.7 Industrial Scientific Corporation

- 7.1.8 MSA Safety Incorporated

- 7.1.9 Crowncon Detection Instruments Limited

- 7.1.10 Yokogawa Electric Corporation

- 7.1.11 Control Instruments Corporation

- 7.1.12 Membrapor AG

- 7.1.13 Senseir AB

- 7.1.14 Eaton Corporation PLC

- 7.1.15 GfG Gas Detection UK Ltd

- 7.1.16 Figaro Engineering Inc.

- 7.1.17 Robert Bosch GmbH

- 7.1.18 Thermofisher Scientific Inc.

- 7.1.19 Detector Electronics Corporation

- 7.1.20 Alphasense Limited

- 7.1.21 California Analytical Instruments

- 7.1.22 Testo SE & Co. KGaA

- 7.1.23 Trolex Ltd

- 7.1.24 Bacharach Inc.

- 7.1.25 MKS Instruments Inc.

- 7.1.26 RKI Instruments Inc.

- 7.1.27 Horiba Ltd

- 7.1.28 SGX Sensortech Limited (Amphenol Limited)

- 7.1.29 Afriso-Euro-Index GmbH

- 7.1.30 General Electric Company

- 7.1.31 NGK Spark Plugs USA Inc.

- 7.1.32 Delphi Technologies (BorgWarner Inc.)

- 7.1.33 Denso Corporation

- 7.2 Vendor Market Share Analysis

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE GROWTH