PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644371

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644371

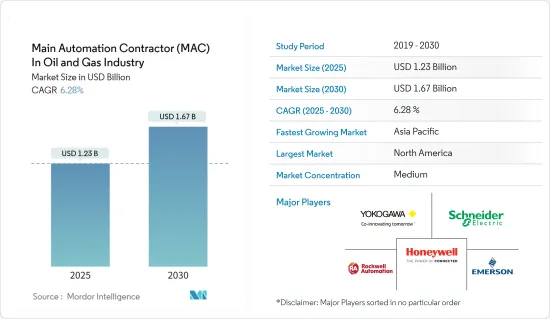

Main Automation Contractor (MAC) In Oil & Gas Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Main Automation Contractor In Oil & Gas Industry is expected to grow from USD 1.23 billion in 2025 to USD 1.67 billion by 2030, at a CAGR of 6.28% during the forecast period (2025-2030).

Key Highlights

- The growing demand for oil and gas across various end-user industries has significantly enhanced the rate of mechanization and the adoption of automation solutions, along with the demand for a higher process and operational efficiency, which positively influences the studied market's growth.

- With the increasing scope of automation in today's information-driven oil production environment, handling more information processing close to the production site is critical. Suitable production and operational data should flow smoothly between oil production and business systems. MAC's responsibility is to design, engineer, and deliver all automation-related equipment and procedures and ensure that these systems are integrated safely and securely and supported by necessary services.

- In the oil and gas industry, the penetration of automation solutions has been touching new heights in recent years, which is fueling the demand for MAC services. For instance, downstream, midstream, and upstream firms have integrated machine learning into their operations in many ways, which may continue to grow. Although, the industry needs to adopt new ways of operating. However, recent trends recognize the immense potential of technologies such as automation, artificial intelligence (AI), and machine learning (ML) can have on the industry.

- Considering such trends, vendors are increasingly entering into partnerships with oil & gas companies to offer MAC services. For instance, in June 2022, ABB partnered with Think Gas, a city gas distribution company, to automate operations across Think Gas' gas network, including many remote terminals spread across multiple locations. ABB created a system to monitor, integrate, and control operations across the company, automating workflows to support operators in improving safety.

- Furthermore, large oil and gas companies are focusing on leveraging MAC as a means of undertaking full project responsibility and delivering satisfactory results by facilitating proper management, automation/instrumentation, manufacture, selection of execution engineers, installation of equipment, commissioning equipment, and after-sales support as MAC implementation has demonstrated significant results in long-term, across various industries.

- However, the cost of implementation of the main automation contractor (MAC) continues to remain among the major challenging factors for the growth of the studied market. Furthermore, the lack of standardization of MAC and related solutions are also among the major restraining factors for the growth of the studied market.

- During the initial outbreak of COVID-19, companies were forced to coordinate their efforts due to the significant changes caused by the pandemic in the MAC supply chain and the growing movement to switch to cleaner, more dependable, and more sustainable energy sources. However, with automation solution proving their supremacy during the COVID period, a significant number of vendors operating in the oil & gas industry are anticipated to increase their investment in advanced automation solutions, creating opportunities in the studied market during the forecast period.

Oil & Gas Main Automation Contractor Market Trends

Upstream Segment to Witness Significant Growth

- The upstream sector of the oil and gas industry involves several drilling activities that must meet stringent government regulations and require intense planning to cut operational costs. Often, the industry deals with vast sets of spatial data to make several decisions. Several process automation tools and analytical engines are employed in the sector to harness the complete power of spatial data.

- Considerable exploration activity in the United Kingdom has led to crucial discoveries such as Glendronach, which is estimated to be the fifth-largest conventional natural gas reserve on the UK Continental Shelf in the millennium. Following Glendronach's success, companies such as Total Energies plan further exploration activities in the vicinity, which may be a significant source of demand for automation solutions from the upstream oil and gas sector.

- Furthermore, the growing demand for oil and gas also drives opportunities in the studied market as it significantly increases upstream activities. For instance, according to OPEC, the global crude oil demand is anticipated to reach 101.89 million barrels per day in 2023.

- The growing demand for oil & gas is also driving investments in the upstream segment of the oil and gas industry. For instance, according to the Canadian Association of Petroleum Producers (CAPP), oil and natural gas investment in upstream production is anticipated to reach CAD 40 billion (USD 29.4 billion) in 2023, surpassing the pre-pandemic levels.

- Similarly, under the National Outer Continental Shelf Oil and Gas Leasing Program for 2019-2024, the US Department of the Interior is planning to allow offshore exploratory drilling in about 90% of the Outer Continental Shelf acreage. The sector is expected to open up new opportunities to the market.

Middle-East and Africa to Register Considerable Growth

- Middle-East and Africa boast a robust oil and gas sector. In recent years, the industry has mirrored global trends and experienced changes and challenges. Investment across the Asia pacific region is becoming more diverse, and new avenues are being explored, such as more complex offshore and LNG projects.

- Several investments are being made for the region's oil and gas capacity expansions. For instance, in January 2023, the Petroleum Agency of Uganda launched its first oil drilling program to meet its target of first oil output in 2025. The Kingfisher field is part of a USD 10 billion scheme to develop the country's oil reserves under Lake Albert and build a vast pipeline to ship the crude internationally via an Indian Ocean port in Tanzania.

- Similarly, in September 2022, the United Arab Emirates announced that it is accelerating a plan to raise its oil production capacity as it attempts to leverage its crude reserves before the world transitions to cleaner energy. Abu Dhabi National Oil Co. (Adnoc), which pumps almost all the United Arab Emirates oil, wants to produce 5 million barrels daily by 2025. The United Arab Emirates also aims to sell more oil and natural gas while fossil fuel prices stay high.

- Saudi Arabia witnessed exponential growth in oil and gas construction projects in the last four decades. Major oil and gas development projects have been constructed in industrial cities, such as Jubail and Yanbu, including the construction of plants, oil and gas refineries, construction of pipelines, well oil setups for extraction, petrochemical manufacturing industries, and other utilities. Hence, the growing activities in the Middle East & African region are anticipated to drive opportunities in the main automation contractor (MAC) market during the forecast period.

Oil & Gas Main Automation Contractor Industry Overview

The automation contractor market in the oil and gas industry exhibits moderate competitiveness, owing to the presence of numerous players offering solutions both domestically and internationally. The market demonstrates a moderate level of concentration, with major industry leaders employing key strategies such as product innovation, mergers, acquisitions, and partnerships to enhance their solutions and expand their global presence. Prominent players in this market include Rockwell Automation Inc., Schneider Electric SE, Yokogawa Electric Corporation, and Honeywell International Inc.

In February 2023, Valmet and Naizak Global Engineering Systems inked a Value Added Reseller (VAR) Agreement pertaining to Valmet DNA Automation Systems. This agreement encompasses applications in various sectors, including oil, gas, power, water, wastewater, and other process industries in Saudi Arabia and Bahrain. Both companies have laid out plans to establish a dedicated Main Automation Contractor (MAC) team, with the objective of competing effectively with major distributed control system vendors.

In October 2022, Yokogawa Electric Corporation secured a significant contract as the main automation contractor (MAC) for the construction of Shell PLC's Holland Hydrogen I plant located in the Dutch port of Rotterdam. This plant is set to produce renewable hydrogen, utilizing electricity generated from an offshore wind farm. Upon its anticipated operational launch in 2025, the Holland Hydrogen I plant is poised to become the largest renewable hydrogen production facility in Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Traditional Approach vs. MAC Approach (Cost Savings Approach)

- 4.4 MAC Best Practices

- 4.5 Key Use Cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Preference of Oil and Gas Companies for a MAC Approach to Avoid Project Management and Integration Complexities

- 5.2 Market Challenges

- 5.2.1 Impact of COVID-19 on the Market and Planned Spending Cuts from Major Oil and Gas Companies

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Upstream (Offshore and Onshore)

- 6.1.2 Midstream

- 6.1.3 Downstream

- 6.2 By Project Size

- 6.2.1 Small and Medium (USD 5 million to USD 30 million)

- 6.2.2 Large (USD 31 million and Above)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Rockwell Automation Inc.

- 7.1.2 Schneider Electric SE

- 7.1.3 Yokogawa Electric Corporation

- 7.1.4 Honeywell International Inc.

- 7.1.5 Emerson Electric Co.

- 7.1.6 Siemens AG

- 7.1.7 ABB Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET