PUBLISHER: SNS Research | PRODUCT CODE: 1994826

PUBLISHER: SNS Research | PRODUCT CODE: 1994826

Dermatological Drugs Market, 2025 - 2035: Opportunities, Challenges, Strategies & Forecasts

Synopsis:

The global dermatological drugs market is experiencing robust growth, driven by rising prevalence of skin disorders, persistent unmet medical needs, and increased demand for innovative therapies. Companies are strategically targeting diverse and previously underserved conditions, with breakthroughs across biologics, biosimilars, and novel therapeutic classes reshaping the competitive landscape. These innovations are delivering highly targeted, high-efficacy treatments across major therapeutic areas, including psoriasis, atopic dermatitis, alopecia areata, and skin cancer, and redefining standards of care.

Dermatological drugs remain the largest segment of spending within the broader dermatology market, projected to reach $52.8 billion globally by 2025. They continue to serve as the primary treatment option for both common conditions, such as acne, and complex diseases, including psoriasis. While patent expirations have introduced generic competition, the market outlook remains robust, supported by several late-stage and near-market drug candidates.

Biologics have emerged as a key growth driver, offering targeted treatment options for chronic conditions and providing targeted options for patients unresponsive to traditional therapies. Complementing this, innovations in drug delivery systems, particularly advanced topical platforms and microneedle technologies, are improving penetration, tolerability, and patient adherence, further supporting market expansion.

The "Dermatological Drugs Market: 2025 - 2035 - Opportunities, Challenges, Strategies & Forecasts" report presents an in-depth assessment of the dermatological drugs ecosystem including dermatological disorders, application areas, delivery technologies, key trends, market drivers, challenges, investment potential, leading therapies, drug development pipeline, opportunities, future roadmap, value chain, ecosystem player profiles and strategies.

The report covers market sizing & forecasts from 2025 - 2035 period which are segmented across seven therapeutic categories, three routes of administration, two drug types (OTC vs. Prescription), four distribution channels, three major drug classes (biologics, small molecules, gene & emerging therapies), and 26 leading countries across five regions.

Topics Covered:

The report covers the following topics:

- Dermatological drugs ecosystem

- Market drivers and barriers

- Dermatological disorders, application areas and key trends

- Analysis of key drug classes and leading dermatological drugs

- Future drug development pipeline

- Dermatological drug delivery technologies

- Industry roadmap and value chain

- Profiles and strategies of 83 leading ecosystem players, including dermatological drug developers

- Strategic recommendations for ecosystem players

- Market analysis and forecasts from 2025 till 2035

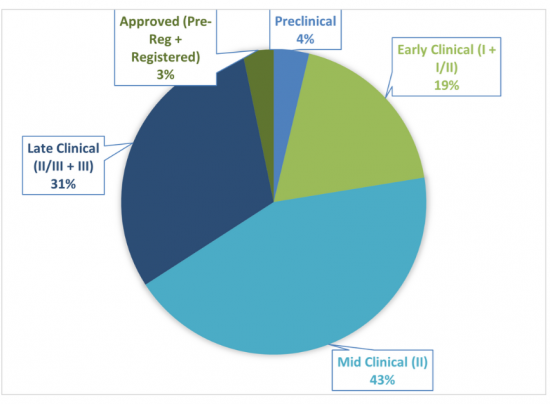

Sample Figure: Distribution of Dermatological Pipeline Candidates by Developmental Phase (%)

The report comes with an associated Excel datasheet suite covering quantitative data from all numeric forecasts presented in the report and 2025 clinical pipeline dataset, profiling 216 drug candidates.

Key Findings:

The report has the following key findings.

- Global dermatological drug spending is projected to reach approximately $52.8 billion in 2025, driven by sustained demand across inflammatory and chronic skin diseases.

- Advanced biologics remain the primary growth engine, supported by high-impact approvals and label expansions across atopic dermatitis, urticaria, prurigo nodularis, and psoriasis.

- IL-23 inhibitors (risankizumab, guselkumab) and dual-pathway IL-17 agents (bimekizumab) are setting the new standard for long-term, durable control of moderate-to-severe disease, reflecting the market's move toward deep, cytokine-specific immunology.

- TYK2 inhibitors, led by deucravacitinib, are reshaping competitive dynamics by offering targeted efficacy with the convenience of oral dosing, positioning them as credible alternatives to injectables.

- Innovation in topical agents such as JAK-based creams and PDE4 inhibitors continues to strengthen, improving localized therapeutic control and expanding treatment options for chronic inflammatory conditions.

- The 2025 commercial entry of multiple ustekinumab biosimilars marks a structural shift in pricing and access, prompting originators to deploy aggressive lifecycle and payer-defense strategies.

- Strategic acquisitions and alliances remain central to growth. Notable examples include J&J's acquisition of Proteologix, adding two bispecific antibodies for atopic dermatitis and reinforcing the industry-wide pivot toward precision immunology.

Key Questions Answered:

The report provides answers to the following key questions.

- How big is the dermatological drugs opportunity?

- What trends, challenges and barriers are influencing its growth?

- How is the ecosystem evolving by segment and region?

- What will the market size be in 2025 and at what rate will it grow?

- Which countries and submarkets will see the highest percentage of growth?

- What are the prospects of biosimilar drugs in dermatology?

- What are the key drug delivery technologies being used in dermatological treatments?

- How big is the market for psoriasis drugs?

- Who are the key market players and what are their strategies?

- How will patent expirations of innovator drugs impact the market?

- What strategies should dermatological drug manufacturers adopt to remain competitive?

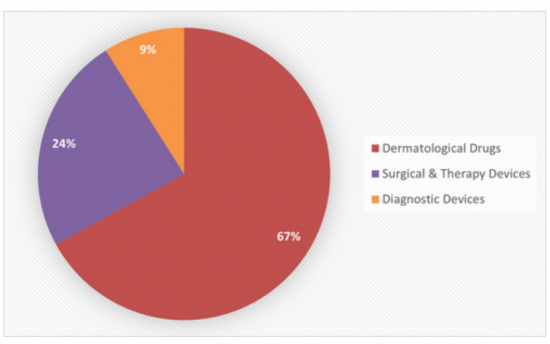

Sample Figure: Global Dermatology Product Spending by Submarket (%)

Forecast Segmentation:

The report provides detailed forecasts across multiple dimensions of the dermatological drugs market, including:

Therapeutic Category

- Acne & Rosacea

- Alopecia & Hair Disorders

- Dermatitis

- Psoriasis

- Skin Infections

- Skin Cancer

- Other Conditions

Drug Delivery Route

- Topical

- Oral

- Parenteral Formulations

Drug Type

- Over-the-Counter (OTC)

- Prescription

Distribution Channel

- Point-of-Care/Clinic

- Retail Pharmacies

- Digital Pharmacies

- Direct-to-Consumer (D2C)

-

Drug Class

Biologics

- IL-23

- IL-17

- IL-4/13

- TNF inhibitors

- IL-12/23 & Others

Small Molecules

- Corticosteroids

- Retinoids

- Calcineurin inhibitors

- PDE4 inhibitors

- JAK inhibitors

- Anti-infectives

- Vitamin D analogues

- Others

Gene & Emerging Therapies

Regional Markets

- Asia Pacific

- Europe

- Middle East & Africa

- North America

- Latin & Central America

Country Markets

- Australia

- Brazil

- Canada

- China

- Egypt

- France

- Germany

- Greece

- India

- Israel

- Italy

- Japan

- Mexico

- Netherlands

- Poland

- Portugal

- Russia

- Saudi Arabia

- South Africa

- South Korea

- Spain

- Switzerland

- Taiwan

- Turkey

- UK

- USA

List of Companies Mentioned:

The following companies and organizations have been reviewed, discussed or mentioned in the report.

- 3M

- Abbott Laboratories

- AbbVie

- Abeona Therapeutics

- AbGenomics Holding

- AboundBio

- Absci Corporation

- Aclaris Therapeutics

- Actelion Pharmaceuticals

- Adaptimmune

- AiCuris

- Akouos

- Akros Pharma

- Alfasigma

- Allergan

- Almirall

- AltruBio

- Amgen

- Amplyx Pharmaceuticals

- Amryt Pharma

- Anacor Pharmaceuticals

- AnaptysBio

- AndroScience Corporation

- AnnJi Pharmaceutical

- AOBiome

- ApoPharma

- Apotex

- Arcutis Biotherapeutics

- Arena Pharmaceuticals

- Array BioPharma

- Asana BioSciences

- Astellas Pharma

- AstraZeneca

- Astria Therapeutics

- Autotelic

- Bausch Health Companies

- Bayer Pharmaceuticals

- Bill and Melinda Gates Foundation

- Biocon Biologics

- Biocon Generics

- Biofrontera

- BioGen

- Biomedical Advanced Research and Development Authority (BARDA)

- BioMimetix

- BioOne Capital

- BioRay Pharmaceutical

- Biosintez

- Bio-Thera Solutions

- Boehringer Ingelheim

- Botanix Pharmaceuticals

- BPGbio

- Bristol-Myers Squibb

- Cadila Pharmaceuticals

- Can-Fite BioPharma

- Cantharidin Pharmaceuticals

- Capella BioScience

- Care Capital

- Castle Creek Biosciences

- Celgene

- CellPoint

- Celltrion

- Cerbios-Pharma

- Checkmate Pharmaceuticals

- Chiesi Farmaceutici

- Chugai Pharmaceutical

- Cipher Pharmaceuticals

- CKD Pharmaceuticals

- Clarion Medical Technologies

- Clinuvel Pharmaceuticals

- Coherus BioSciences

- Concert Pharmaceuticals

- CorMedix

- Cosette Pharmaceuticals

- Cosmo Pharmaceuticals

- CSL Behring

- Cumberland Pharmaceuticals

- Cutanea Life Sciences

- Daewoong Pharmaceutical

- Debiopharm

- Dermata Therapeutics

- Dermavant Sciences

- DermBiont

- Dermira

- DFB Soria

- DICE Therapeutics

- Dow Pharmaceutical

- Dr. Reddy's Laboratories

- Durata Therapeutics

- Dusa Pharmaceuticals

- Eirion Therapeutics

- Eli Lilly and Company

- Elorac

- Elsie Biotechnologies

- EMD Serono

- Encore Dermatology

- Escalier Biosciences

- Escient Pharmaceuticals

- European Medicines Agency (EMA)

- Evolus

- Ewopharma

- Exelixis

- Eywa Pharma

- F. Hoffmann-La Roche

- FAES Farma

- FDA

- Fibrocell Science

- G&E Herbal Biotechnology

- Galapagos

- Galderma

- Galectin Therapeutics

- Genentech

- Gilead Sciences

- Glenmark Pharmaceuticals

- GSK (GlaxoSmithKline)

- Gurnet Point

- Gurnet Point Capital

- Hallux

- Hapten Sciences

- Horizon Therapeutics

- Hospira

- Hoth Therapeutics

- Huya Bioscience

- Ichnos Glenmark Innovation

- Ichnos Sciences

- Immunocore

- Immutep

- Incyte Corporation

- Innovation Pharmaceuticals

- InSite Vision

- Iovance Biotherapeutics

- Ipsen

- Janssen Pharmaceutical

- Janssen Research & Development

- Japan Tobacco

- Jiangsu Hengrui Medicine

- Johnson & Johnson

- Journey Medical Corporation

- Kiniksa Pharmaceuticals

- Kintara Therapeutics

- Krystal Biotech

- Kyowa Kirin

- Ladrome

- LEO Pharma

- Libertas Bio

- Ligand Pharmaceuticals

- Lipidor

- Maruho

- Mayne Pharma

- MB Venture Partners

- Meda Pharma

- Melinta Therapeutics

- Merck & Co

- Merck KGaA

- Merz Pharma

- Microsoft

- Moderna

- MorphoSys

- Mycovia Pharmaceuticals

- Mylan

- Nanology

- Nestle Skin Health

- Neumedicines

- Nielsen BioSciences

- Novartis

- Novo Holdings

- Oncolys Biopharma

- Oncotelic

- Ono Pharmaceutical

- Optinose

- OriCiro Genomics

- Ortho Dermatologics

- Paratek Pharmaceuticals

- Pelthos Therapeutics

- Pfizer

- Philogen

- Phio Pharmaceuticals

- Photogen Technologies

- Pierre Fabre

- Pierre Fabre Laboratories

- Poli Group

- Polpharma Biologics

- PolyMedix

- Precigen

- Prevail Therapeutics

- Principia Biopharma

- Priovant Therapeutics

- Promius Pharma

- ProQR Therapeutics

- Proteologix

- Protomer Technologies

- Provectus Biopharmaceuticals

- Pyxis Oncology

- Qurient

- Ralexar Therapeutics

- Ranbaxy Laboratories

- Rani Therapeutics

- Regeneron Pharmaceuticals

- Roche

- Roivant Sciences

- Samsung

- Samsung Bioepis

- Sandoz AG

- Sanofi

- SBI Biotech

- Searchlight Pharma

- Seattle Genetics

- Sierra Oncology

- Sinclair Pharma

- Sol-Gel Technologies

- Soligenix

- Stiefel Laboratories

- Sun Pharmaceutical Industries

- Takeda

- Takeda Oncology

- Taro Pharmaceutical Industries

- Teva Pharmaceutical Industries

- The Proactiv Company

- Timber Pharmaceuticals

- Tioga Pharmaceuticals

- Torii Pharmaceutical

- Trillium Therapeutics

- UCB Biopharma

- UNION Therapeutics

- University of Pennsylvania

- Upjohn

- URL Pharma

- US WorldMeds

- Valeant Pharmaceuticals

- Vanda Pharmaceuticals

- Vectans Pharma

- Verrica Pharmaceuticals

- VidacPharma

- Villaris Therapeutics

- Vyne Therapeutics

- Zydus Group