PUBLISHER: Zhar Research | PRODUCT CODE: 1880930

PUBLISHER: Zhar Research | PRODUCT CODE: 1880930

Long Duration Energy Storage for Datacenters, Microgrids, Houses: Technologies, Markets 2026-2036

Summary

Delayed electricity is needed for much more than grids. The new 451-page Zhar Research report, "Long Duration Energy Storage for Datacenters, Microgrids, Houses: Technologies, Markets 2026-2036" forecasts a $97 billion market for this in 2046, 36% of the total LDES market emerging. The requirements are very different in this world that includes off-grid and fringe-of-grid (only rare use of grid for backup). Expect 100 times the number needed for grids but smaller, space constrained units, variously safe even in buildings, stacked for small footprint and long-life, highly-reliable for remote locations. The authors even predict LDES in large numbers of solar houses before 2046, many off-grid. Unusually thorough, the report has 10 chapters, 17 SWOT appraisals, 24 forecast lines 2026-2046, examining over 100 companies and research advances through 2025.

The Executuve Summary and Conclusions (37 pages) is the quick read with the roadmap 2026-2046 in three lines - market, company, technology - 18 key conclusions, six of the SWOT appraisals and the 24 forecasts as tables and graphs with explanation. See many new infograms. Chapter 2. LDES Need and Design Principles (15 pages) is mostly graphics introducing stationary energy storage and LDES fundamentals, actual and proposed types of LDES, nine LDES technologies that can follow the market trend to longer duration with subsets compared. Learn how the off-grid solar house LDES is the toughest challenge but coming 2036-46, understand LDES metrics and LDES projects in 2025-6 with leading technology subsets for microgrid and similar applications. See scientific categories of LDES compared by 8 parameters, electrochemical LDES options compared but why most batteries will stay uncompetitive above 10-hour duration.

The report is balanced, realistic and independent so it has as Chapter 3. Microgrid LDES Escape Routes with 7 pages, mostly infograms and charts, covering the ways in which the demand for LDES in microgrids and similar applications down to houses will be reduced or avoided. That includes 2025 research advances including Home Energy Management Systems coping with intermittent supply.

Chapter 4. Advanced Pumped Hydro APHES (46 pages) combs through the many options avoiding pumping water up mountains. Here is pumping heavy, loaded water up mere hills, use of mines, the ocean and more. Many are suitable for the larger microgrid and similar applications but never solar buildings.

Chapter 5. Hydrogen H2ES and compressed air CAES for microgrid LDES (22 pages) examines these important options for grid LDES that are less impressive beyond but there are some microgrid projects appraised that use them. Learn the issues.

Chapter 6. Redox flow batteries RFB is 154 pages because this is currently the gold standard for microgrid and similar LDES, having the most installations, manufacturers and the strongest appropriate research pipeline, including for the more-compact hybrid RFBs. 45 manufacturers are appraised.

Chapter 7. Solid Gravity Energy Storage SGES has only 36 pages because it is a weaker contestant but five manufacturers examined and the various subsets have some prospects. Chapter 8. Advanced conventional construction batteries ACCB (48 pages) examines many emerging chemistries using conventional construction not flow battery principles. Much 2025 research is appraised. Many are fundamentally too expensive or too poor in certain performance parameters but there are possibilities too and successes to report.

Chapter 9. Liquefied Gas Energy Storage LGES: Liquid Air LAES or CO2 (43 pages) looks at this middle ground where extremely safe options using established technologies can provide LDES that has many competitive advantages for large microgrids and similar applications. LGES is more compact but pressurised carbon dioxide avoids the cryogenics. See appropriate projects, manufacturer intentions. The report then closes with Chapter 10. Thermal Energy Storage for Delayed Electricity ETES (22 pages). Delayed heat is a great success but there is less enthusiasm for thermally delayed electricity due to leakage, size and other issues. Nonetheless there is a project in Alaska and there are companies pursuing exotic forms such as thermophotovoltaics that are appraised. Learn the lessons of failures as well.

The Zhar Research report, "Long Duration Energy Storage for Datacenters, Microgrids, Houses: Technologies, Markets 2026-2036" is your essential reading for the latest research and balanced analysis of this large new opportunity. For these applications, it finds that redox flow batteries, liquid gas energy storage and some other options are the best compromises but different ones win at the extremes of AI datacenters and private houses 2026-2046.

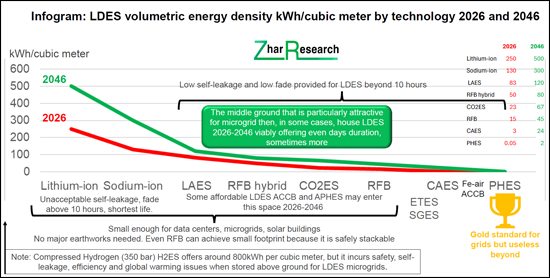

CAPTION: LDES volumetric energy density kWh/cubic meter by technology 2026 and 2046. Source: Zhar Research report, "Long Duration Energy Storage for Datacenters, Microgrids, Houses: Technologies, Markets 2026-2036".

Table of Contents

1. Executive summary and conclusions

- 1.1. Purpose and unique scope of this report

- 1.2. Methodology of this analysis

- 1.3. Examples of current beyond-grid LDES and similar

- 1.4. Technology basics

- 1.5. 18 key conclusions concerning electrification and LDES definitions, needs, candidates

- 1.6. Infogram: LDES volumetric energy density kWh/cubic meter by technology 2026 and 2046

- 1.7. Infogram: Escape routes from microgrid and similar LDES 2026-2046

- 1.8. Infogram: Off-grid solar house with LDES in 2036-46 - all-electric

- 1.9. Some customer types and potential energy services from LDES

- 1.10. Potential LDES performance by ten technologies in 19 columns

- 1.11. Three LDES sizes, with different technology winners 2026-2046 on current evidence

- 1.12. Acceptable sites: numbers by technology 2026-2046 showing microgrid opportunity

- 1.13. Calculations of LDES need by technology with implications

- 1.14. Current and emerging LDES duration vs power deliverable

- 1.14.1. Current LDES situation in green and trend in grid need in blue: simplified version

- 1.14.2. Duration hours vs power delivered by project and 12 technologies in 2026

- 1.15. Nine SWOT appraisals of potential broadly-defined microgrid LDES technologies for 2026-2046

- 1.16. Long Duration Energy Storage LDES roadmap 2026-2046

- 1.17. Market forecasts in 24 lines 2026-2046 with graphs and explanation

- 1.17.1. LDES total value market showing beyond-grid gaining share 2024-2046

- 1.17.2. LDES market in 9 technology categories $ billion 2026-2046 table, graphs, explanation

- 1.17.3. Total LDES value market % in three size categories 2026-2046 table, graph, explanation

- 1.17.4. Regional share of LDES value market % in four regions 2026-2046 table, graph, explanation

- 1.17.5. Number of LDES actual and putative manufacturers: RFB vs Other showing shakeout 2026-2046

- 1.17.6. Vanadium vs iron vs other RFB LDES market % value sales with technology strategies 2026-2046

- 1.17.7. RFB achievements and aspirations 2026-2046

2. LDES need and design principles

- 2.1. Energy fundamentals

- 2.2. Stationary energy storage and LDES fundamentals

- 2.2.1. General

- 2.2.2. Actual and proposed types of LDES

- 2.2.3. Nine LDES technologies that can follow the market trend to longer duration with subsets compared

- 2.2.4. Three sizes of grid and similar generator-user systems showing LDES potential

- 2.2.5. Off-grid solar house LDES is toughest challenge but coming 2036-46

- 2.2.6. LDES metrics

- 2.3. LDES projects in 2025-6 showing leading technology subsets

- 2.4. Scientific categories of LDES compared by 8 parameters

- 2.5. Electrochemical LDES options explained

- 2.6. Most batteries uncompetitive above 10-hour duration

- 2.7. Grand overview report on all LDES 2026-2046

3. Microgrid LDES escape routes

- 3.1. General situation

- 3.2. Infogram: 13 escape routes from LDES 2026-2046

- 3.3. Examples across the world: Denmark, Singapore, China, USA

- 3.4. Capacity factor of wind, solar and options that need little or no LDES

- 3.5. Extensive 2025 research on LDES escape routes

- 3.6. Research in 2025 on Home Energy Management Systems coping with intermittent supply

4. Advanced pumped hydro APHES

- 4.1. Overview

- 4.2. Using mining sites

- 4.2.1. Potential

- 4.2.2. Research advances in 2025

- 4.3. Pressurised underground: Quidnet Energy USA

- 4.4. Using heavier water up mere hills: RheEnergise UK

- 4.4.1. General

- 4.4.2. RheEnergise installation progress 2025-6

- 4.4.3. Power for mines and other targets with appraisal of prospects

- 4.5. Using seawater or other brine

- 4.5.1. General

- 4.5.2. Brine in salt caverns Cavern Energy USA

- 4.5.3. SWOT appraisal of seawater pumped hydro on land

- 4.6. Sizeable Energy Italy, StEnSea Germany, Ocean Grazer Netherlands

- 4.6.1. General

- 4.6.2. Sizable Energy Itay

- 4.6.3. StEnSea Germany

- 4.6.4. Ocean Grazer Netherlands

- 4.6.5. SWOT appraisal of underwater energy storage for LDES

- 4.7. Hybrid technologies: research advances in 2024 and 2025

- 4.8. Research advances in 2024 and 2025

- 4.9. SWOT appraisal of APHES

5. Hydrogen H2ES and compressed air CAES for microgrid LDES

- 5.1. Hydrogen H2ES

- 5.1.1. Overview

- 5.1.2. Calistoga Resiliency Centre USA 48-hour microgrid

- 5.1.3. Ulm University microgrid trial Germany 2025-2027

- 5.1.4. China plans 2025 and 2026

- 5.1.5. New hydrogen storage methods and LDES relevance

- 5.2. Compressed air CAES for microgrids

- 5.2.1. Overview

- 5.2.2. Augwind Energy Israel

- 5.2.3. Keep Energy Systems UK

- 5.2.4. LiGE Pty Ltd South Africa

6. Redox flow batteries RFB

- 6.1. Overview

- 6.2. RFB research pivoting to LDES

- 6.2.1. Overview of RFB and its potential for LDES

- 6.2.2. Infogram: RFB achievements and aspirations 2026-2046

- 6.2.3. 72 RFB research advances in 2025

- 6.2.4. 18 examples of RFB research advances in 2024

- 6.3. Winning LDES redox flow battery technologies 2026-2046

- 6.4. SWOT appraisal and parameter comparison of RFB for LDES

- 6.5. 45 RFB companies compared in 8 columns: name, brand, technology, tech. readiness, beyond grid focus, LDES focus, comment

- 6.6. RFB technologies with research advances through 2025

- 6.6.1. Regular or hybrid, their chemistries and the main ones being commercialised

- 6.6.2. SWOT appraisals of regular vs hybrid options

- 6.7. Specific designs by material: vanadium, iron and variants, other metal ligand, halogen-based, organic, manganese with 2025 research, three SWOT appraisals

- 6.7.1. Vanadium RFB design and SWOT appraisal

- 6.7.2. All-iron and variants RFB design and SWOT appraisal

- 6.8. RFB manufacturer profiles

- 6.9. Further research in 2025

7. Solid gravity energy storage SGES

- 7.1. Overview including research in 2025

- 7.1.1. General

- 7.1.2. Three stages of operation

- 7.1.3. Three geometries

- 7.1.4. Pumped hydro gravity storage compared to the three SGES options

- 7.1.5. Basics

- 7.1.6. SWOT appraisal of solid gravity storage SGES for LDES

- 7.1.7. Parameter appraisal of solid gravity energy storage SGES for LDES

- 7.1.8. CAPEX challenge

- 7.1.9. Challenge of ongoing expenses

- 7.1.10. Possibility of pumping sand

- 7.1.11. Hydraulic piston lift instead of cable: 2025 modelling

- 7.1.12. Appraisal of other SGES research through 2025 and 2024

- 7.2. ARES USA

- 7.3. Energy Vault Switzerland, USA and China, India licensees

- 7.4. Gravitricity

- 7.5. Green Gravity Australia

- 7.6. SinkFloatSolutions France

8. Advanced conventional construction batteries ACCB

- 8.1. Overview

- 8.2. Eight ACCB manufacturers compared: 8 columns: name, brand, technology, tech. readiness, beyond-grid focus, LDES focus, comment

- 8.3. Parameter appraisal and SWOT appraisal of ACCB for LDES

- 8.3.1. Parameter appraisal

- 8.3.2. SWOT appraisal of ACCB for LDES

- 8.3.3. Research appraisal published in 2025

- 8.4. Metal-air batteries

- 8.4.1. Iron-air with SWOT and 2025 research: Form Energy USA

- 8.4.2. Aluminium-air : Phinergy Israel

- 8.4.3. Zinc-air with SWOT: E-Zinc, AZA battery, Zinc8 (Abound)

- 8.5. High temperature batteries

- 8.5.1. Molten calcium antimony: Ambri USA out of business, SWOT

- 8.5.2. Sodium or lithium sulfur: NGK/ BASF Japan/ Germany, others, research in 2025, SWOT

- 8.6. Metal-ion batteries including Inlyte, Altris, HiNa, Tiamat, Natron, Faradion

- 8.6.1. Sodium-ion with SWOT

- 8.6.2. Zinc halide Eos Energy Enterprises USA with SWOT

- 8.6.3. Zinc-ion Enerpoly, Urban Electric Power USA, NextEra USA

- 8.7. Nickel hydrogen batteries: EnerVenue USA with SWOT

9. Liquefied gas energy storage LGES: Liquid air LAES or CO2

- 9.1. Overview

- 9.2. Liquid air LAES LDES

- 9.2.1. Technology and research advances through 2025

- 9.2.2. Parameter comparison of LAES for LDES

- 9.2.3. SWOT appraisal of LAES for LDES

- 9.2.4. Indicative LAES systems, footprints and operating parameters

- 9.2.5. Research advances in 2025 and 2024

- 9.2.6. CGDG, Zhongli Zhongke Energy Storage Technology Co China

- 9.2.7. Highview Energy UK and partners Sumitomo, Centrica, Rio Tinto and others

- 9.2.8. MIT study of LAES viability in USA

- 9.2.9. Phelas Germany

- 9.3. Liquid and compressed carbon dioxide LDES

- 9.3.1. Overview

- 9.3.2. Parameter comparison of CO2 for LDES

- 9.3.3. SWOT appraisal of liquid CO2 for LDES

- 9.3.4. Research advances in 2025

- 9.3.5. Energy Dome Italy

- 9.3.6. China and Kazakhstan

10. Thermal energy storage for delayed electricity ETES

- 10.1. Overview and research advances in 2025

- 10.2. Research advances in 2025 and 2024

- 10.3. Lessons of failure: Siemens Gamesa, Azelio, Steisdal, Lumenion

- 10.4. The heat engine approach proceeds: Echogen USA

- 10.5. Use of extreme temperatures and photovoltaic conversion

- 10.5.1. Antora USA

- 10.5.2. Fourth Power USA

- 10.6. Marketing delayed heat and electricity from one plant

- 10.6.1. Overview

- 10.6.2. MGA Thermal Australia

- 10.6.3. Malta Inc Germany