PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071355

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071355

Systemic Lupus Erythematosus Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

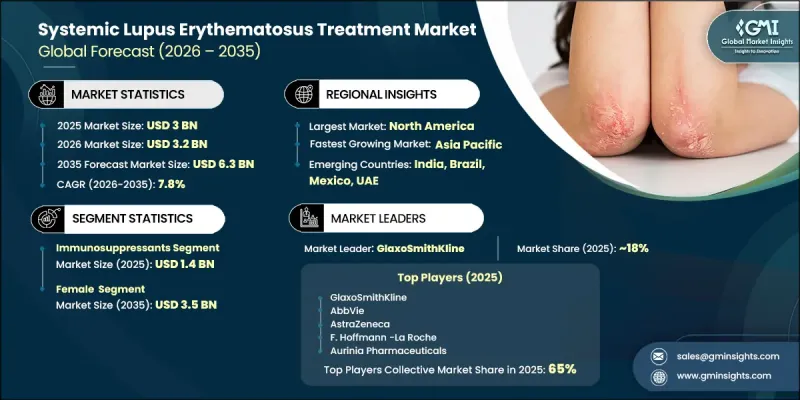

The Global Systemic Lupus Erythematosus Treatment Market was valued at USD 3 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 6.3 billion by 2035.

Growth is driven by increasing awareness of early disease detection, improved diagnostic accuracy, and broader availability of advanced treatment options. The higher incidence of systemic lupus erythematosus, particularly among women in reproductive age groups, is sustaining long-term demand for effective disease management therapies. Expanding healthcare expenditure, supportive initiatives for chronic and rare disease treatment, and continuous innovation in immunology are further reinforcing market expansion. The increasing use of precision medicine and biomarker-based approaches is reshaping treatment paradigms by enabling more individualized and outcome-focused care strategies. Growing access to specialist healthcare providers and improved patient monitoring systems is also supporting better disease control and reduced flare frequency across patient populations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 7.8% |

Systemic lupus erythematosus treatment refers to a range of therapeutic approaches used to manage a chronic autoimmune condition that affects multiple organ systems, including the skin, joints, kidneys, cardiovascular system, and nervous system. The primary treatment goal is to reduce inflammation, control immune system activity, prevent organ damage, and improve long-term quality of life. Therapeutic options include corticosteroids, nonsteroidal anti-inflammatory drugs, antimalarial agents, immunosuppressants, biologics, and newer targeted therapies designed to address specific immune pathways. Increasing adoption of personalized medicine approaches is enhancing treatment precision and improving patient outcomes.

The immunosuppressants segment generated USD 1.4 billion in 2025. This dominance is attributed to the essential role these therapies play in controlling immune overactivity and preventing disease progression. Widely used agents support the management of moderate to severe disease conditions, particularly in cases involving kidney complications and multi-organ involvement.

The hospital pharmacies segment accounted for a 52.6% share in 2025, reflecting their central role in the delivery of complex lupus treatment regimens. These facilities ensure timely access to advanced therapies that require close clinical supervision, particularly during disease flare-ups or treatment initiation phases. Their integration with multidisciplinary care teams supports optimized treatment selection, safety monitoring, and adverse event management, reinforcing their importance in patient care pathways.

North America Systemic Lupus Erythematosus Treatment Market held a 38.4% share in 2025, supported by a highly advanced healthcare infrastructure and strong adoption of innovative therapies. The region benefits from early diagnosis practices, high disease awareness, and broad access to specialized care services. Strong participation from pharmaceutical and biotechnology companies, combined with an active clinical research environment, continues to drive innovation and commercialization of new treatment options.

Major players operating in the global systemic lupus erythematosus treatment industry include AstraZeneca, AbbVie, F. Hoffmann-La Roche, GlaxoSmithKline, Teva Pharmaceutical, Sandoz, Sun Pharmaceutical, Cipla, Lupin, Aurinia Pharmaceuticals, and ImmuPharma. Companies in the systemic lupus erythematosus treatment market are strengthening their market position by investing in biologics and next-generation immunotherapies that target specific immune pathways involved in disease progression. They are expanding clinical trial programs to accelerate approval timelines for novel therapies and improve treatment efficacy. Strategic collaborations between pharmaceutical companies and research institutions are supporting faster drug development and broader clinical validation. Firms are also focusing on biomarker-driven precision medicine approaches to improve patient stratification and treatment outcomes. Expansion into emerging markets with rising autoimmune disease prevalence is further supporting growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Gender trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of SLE

- 3.2.1.2 Advancements in treatment options

- 3.2.1.3 Increased government funding and support for research on autoimmune diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Limited awareness and diagnosis

- 3.2.3 Market opportunities

- 3.2.3.1 Development of organ-specific lupus therapies

- 3.2.3.2 Expansion of personalized and precision medicine approaches

- 3.2.3.3 Rising demand for steroid-sparing targeted therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis (Driven by Primary Research)

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Technology and innovation trends

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Immunosuppressants

- 5.3 Corticosteroids

- 5.4 Biologics

- 5.5 Antimalarials

- 5.6 NSAIDs

Chapter 6 Market Estimates and Forecast, By Gender, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Female

- 6.3 Male

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Intravenous

- 7.4 Subcutaneous

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 AstraZeneca

- 10.3 Aurinia Pharmaceuticals

- 10.4 Cipla

- 10.5 F. Hoffmann-La Roche

- 10.6 GlaxoSmithKline

- 10.7 ImmuPharma

- 10.8 Lupin

- 10.9 Sandoz

- 10.10 Sun Pharmaceutical

- 10.11 Teva Pharmaceutical