PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740913

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740913

eVTOL Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

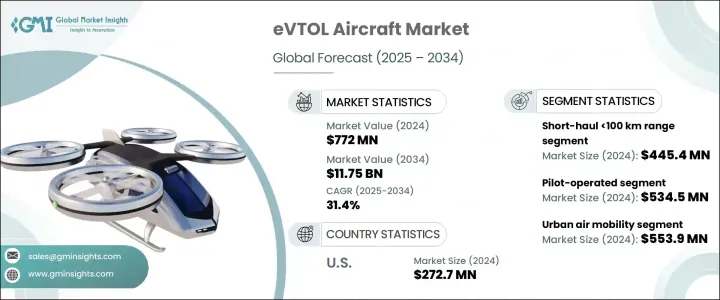

The Global eVTOL Aircraft Market was valued at USD 772 million in 2024 and is estimated to grow at a CAGR of 31.4% to reach USD 11.75 billion by 2034. The rapid pace of urbanization is driving up road congestion, making traditional transport modes less efficient. This shift is prompting significant interest in alternative mobility options, with eVTOLs emerging as a leading solution for short, efficient, point-to-point travel. Governments and city planners are actively encouraging these aircraft as part of modern infrastructure development, leveraging public-private partnerships to support implementation. There's also growing acknowledgment that an optimized urban transport system can contribute to overall economic performance. Meanwhile, the global push for sustainability is accelerating the transition toward electric-powered mobility, further boosting the relevance of eVTOL technology in today's eco-conscious markets.

However, certain challenges have tempered the market's growth trajectory. Tariffs imposed on key imported materials such as steel, aluminum, and aerospace components have driven up production costs, particularly impacting manufacturers relying on international supply chains. These increased costs have made it harder for companies to offer competitive pricing, especially in a market that is highly price sensitive. Higher production expenses are also being passed on to consumers, causing retail prices to climb. Additionally, supply chain interruptions have delayed final deliveries, creating uncertainty for buyers and slowing adoption rates. Despite these hurdles, local manufacturers have seen an advantage, as reduced foreign competition gives them more room to grow. Over the long term, the industry is expected to recalibrate, with more companies turning to domestic sourcing and reconfiguring supply chains to become less vulnerable to global disruptions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $772 Million |

| Forecast Value | $11.75 Billion |

| CAGR | 31.4% |

eVTOLs are increasingly being viewed as a practical answer to the inefficiencies of ground-based transportation. Their ability to bypass road traffic and enable swift, direct routes offers a compelling value proposition, especially for urban commuters. These aircraft are designed to land and take off vertically, making them ideal for city environments with limited space. Governments are also acknowledging their potential to transform urban mobility and are integrating them into long-term transportation planning. As clean transportation becomes a national and international priority, electric aviation is gaining support through both regulatory backing and private investment.

Innovation in battery technology and electric propulsion systems is playing a pivotal role in making eVTOLs more commercially viable. Advances in lithium-ion and emerging solid-state batteries are extending flight range, enhancing safety, and increasing payload capacity. At the same time, new materials and efficient propulsion designs are lowering overall operational costs. These improvements are attracting investments from major players in the aerospace and automotive sectors, who see long-term potential in urban air mobility. Developers are also using lightweight composites and exploring energy-efficient motor technologies to enhance aircraft performance while meeting sustainability goals.

By range, the short-haul (up to 100 km) segment accounted for USD 445.4 million in 2024. This category is gaining momentum as the most practical solution for intra-city and regional air travel, especially for use cases requiring quick, frequent flights. These aircraft are well-suited for applications like air taxis, medical transportation, and logistics. Battery improvements are helping extend flight times while increasing payload capacity. Governments and private firms are investing in supporting infrastructure like takeoff and landing zones, though challenges related to noise, regulation, and public trust still need to be addressed.

When broken down by autonomy, pilot-operated eVTOLs led the market in 2024 with a valuation of USD 534.5 million. These models are preferred during the initial stages of commercial deployment due to greater public trust and smoother regulatory approval. While the requirement for trained pilots increases operational costs, it also ensures safety and control, which is critical as the technology gains broader acceptance. Companies are prioritizing user-friendly interfaces and semi-automated cockpit systems to support operators and reduce workload. These aircraft serve as a stepping stone to full autonomy, helping to build credibility and operational data that will eventually support more advanced systems.

In terms of regional demand, the U.S. dominated the market with a valuation of USD 272.7 million in 2024. The country offers a strong ecosystem of legacy aerospace firms and agile startups, supported by a culture that embraces technological innovation. Research efforts focused on battery and automation technologies are pushing the market forward. While integration challenges like air traffic control and public sentiment remain, the country's commitment to commercializing eVTOL services is evident through partnerships with mobility companies and infrastructure investments.

Manufacturers are taking strategic steps to remain competitive by investing in energy-efficient designs, reducing aircraft noise, and integrating automation. Some are leveraging AI for air traffic management and predictive maintenance to streamline operations. Customization for niche sectors like cargo, medical transport, and premium air travel is becoming a key trend. At the same time, mergers, partnerships, and collaborations with regulatory authorities are helping firms scale operations and navigate certification processes. Emerging technologies like digital twins and robotics are also helping reduce costs and increase safety across production lines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Urban congestion and need for efficient mobility

- 3.3.1.2 Advancements in battery and electric propulsion technologies

- 3.3.1.3 Environmental sustainability and emission reduction goals

- 3.3.1.4 Rising investments and strategic partnerships

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development costs

- 3.3.2.2 Regulatory approval delays

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Range, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Short-Haul <100 km

- 5.3 Medium-Haul 100-300 km

- 5.4 Long-Haul >300 km

Chapter 6 Market Estimates & Forecast, By Autonomy Level, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Pilot-operated

- 6.3 Remote-piloted

- 6.4 Fully autonomous

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Urban air mobility

- 7.3 Air ambulance

- 7.4 Tourism & leisure

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Joby Aviation

- 9.2 Archer Aviation Inc.

- 9.3 EHang

- 9.4 Volocopter

- 9.5 Lilium

- 9.6 BETA Technologies

- 9.7 Vertical Aerospace

- 9.8 Wisk Aero

- 9.9 Supernal, LLC

- 9.10 Eve Air Mobility

- 9.11 Autoflight

- 9.12 Overair, Inc.

- 9.13 AeroMobil

- 9.14 SkyDrive Inc.

- 9.15 Jaunt Air Mobility LLC.

- 9.16 Urban Aeronautics

- 9.17 Bell Textron Inc.

- 9.18 DORONI AEROSPACE INC. ALL

- 9.19 Guangdong Huitian Aerospace Technology Co., Ltd.