PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750532

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750532

Fuel Cell Stack Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

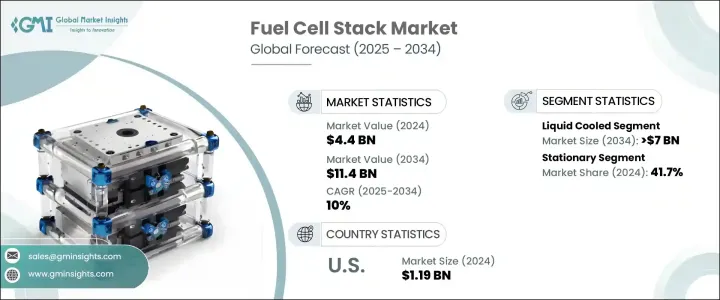

The Global Fuel Cell Stack Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 11.4 billion by 2034. This growth is largely fueled by the increasing enforcement of regulatory frameworks that support sustainable energy technologies, including fuel cells. As nations and industries intensify efforts to combat climate change and curb greenhouse gas emissions, fuel cell stacks are gaining significant traction across various applications. Governments around the world are actively promoting clean energy adoption through tax incentives, subsidies, and research initiatives, creating a favorable environment for market growth. Growing awareness of the environmental impact of conventional energy sources is prompting industries to shift toward zero-emission solutions, which is further bolstering the demand for fuel cell technology. Additionally, the expansion of hydrogen infrastructure and the integration of fuel cells into transportation-especially for high-performance and heavy-duty vehicles-are expected to create new avenues for market development. Technological advances aimed at improving performance, cost-efficiency, and scalability are also accelerating market momentum.

The demand for fuel cell stacks is heavily influenced by the continuous push for clean energy alternatives in the industrial, commercial, and residential sectors. As decarbonization becomes a strategic priority, the role of fuel cells in energy systems is expanding. Their ability to support hybrid setups, improve grid reliability, and provide efficient backup power makes them an attractive choice across sectors. Moreover, collaborations among stakeholders-including energy companies, research institutes, and manufacturers-are helping accelerate product innovation and deployment. Efforts to streamline manufacturing processes and reduce costs through improved materials and production techniques are expected to enhance affordability and accessibility, enabling broader adoption in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 10% |

In terms of product type, the market is segmented into air-cooled and liquid-cooled fuel cell stacks. The industry recorded USD 3.8 billion in 2022, USD 4.1 billion in 2023, and USD 4.4 billion in 2024. Among these, the liquid-cooled segment is projected to surpass USD 7 billion by 2034. This growth is being driven by the increasing use of fuel cells in high-power and intensive-duty applications, along with enhanced performance enabled by advanced thermal management. Liquid cooling systems support more stable operating conditions, better heat dissipation, and extended lifespan-making them ideal for sectors that demand consistent and reliable power output. The ongoing development of liquid-cooled systems is making them increasingly suitable for industrial and commercial backup systems where performance and durability are critical.

On the basis of application, the fuel cell stack market is categorized into automotive, stationary, power generation, and others. In 2024, the stationary segment held the largest share, accounting for 41.7% of the overall market. This dominance can be attributed to advancements in stationary fuel cell systems and the growing demand for sustainable and decentralized energy solutions. As industries seek to reduce their carbon footprints, stationary fuel cell systems are being adopted to power buildings, factories, and remote facilities with minimal emissions. Their compatibility with renewable energy sources also supports the creation of hybrid systems that ensure energy efficiency, reliability, and backup capabilities.

Regionally, North America held a 28.7% share of the global fuel cell stack market in 2024. The U.S. market alone was valued at USD 1.05 billion in 2022, USD 1.11 billion in 2023, and USD 1.19 billion in 2024. Growth in this region is supported by the development of hydrogen refueling infrastructure and increased deployment of fuel cell-powered vehicles. Continued public and private investment in building out hydrogen distribution networks is expected to strengthen the regional market further, positioning North America as a key player in the global fuel cell landscape.

The competitive landscape of the fuel cell stack market is marked by a combination of established companies and emerging innovators. The top five players- Plug Power, Ballard Power Systems, FuelCell Energy, Bloom Energy, and Doosan Fuel Cell-collectively contribute over 45% of the total market share. While dominant firms focus on scaling up production and reducing system costs, startups are targeting niche applications and exploring integration with renewable energy technologies. As companies strive to enhance manufacturing efficiency and adopt alternative materials, the race to provide cost-effective and scalable fuel cell solutions is intensifying. Strategic investments, government support, and alignment with clean energy goals continue to reshape market dynamics, encouraging innovation and competition throughout the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic initiatives

- 4.3 Company market share

- 4.4 Company benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 – 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Air Cooled

- 5.3 Liquid Cooled

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 <5 kW

- 6.3 5 kW – 100 kW

- 6.4 >100 kW – 200 kW

- 6.5 >200 kW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Stationary

- 7.4 Power generation

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Philippines

- 8.4.6 Vietnam

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Peru

Chapter 9 Company Profiles

- 9.1 Advent Technologies Holding

- 9.2 Ballard Power Systems

- 9.3 Commonwealth Automation Technologies

- 9.4 Dana Incorporated

- 9.5 ElringKlinger

- 9.6 FuelCell Energy Solutions

- 9.7 Freudenberg Group

- 9.8 Horizon Fuel Cell Technologies

- 9.9 Intelligent Energy Limited

- 9.10 Nedstack Fuel Cell Technology

- 9.11 Nuvera Fuel Cells

- 9.12 PowerCell Sweden

- 9.13 Plug Power

- 9.14 Robert Bosch

- 9.15 Schunk Bahn-und Industrietechnik

- 9.16 TW Horizon Fuel Cell Technologies