PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766197

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766197

Automotive Radar-on-Chip Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

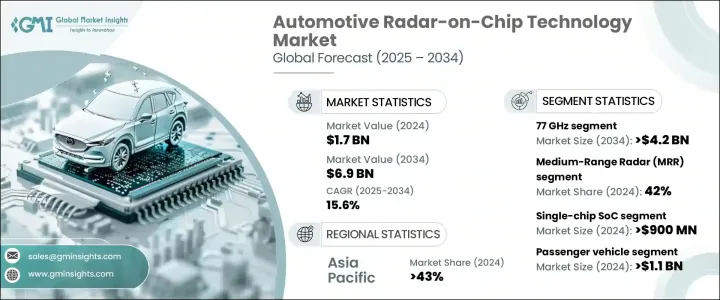

The Global Automotive Radar-on-Chip Technology Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 15.6% to reach USD 6.9 billion by 2034. As original equipment manufacturers (OEMs) push advancements from Level 2+ to Level 4 autonomy, the demand for sophisticated and scalable perception systems continues to rise. Radar-on-chip technology integrates antennas, transceivers, and signal processing components onto a single chip, significantly lowering overall system costs, minimizing size, and simplifying complexity compared to traditional radar modules. This integration is particularly beneficial for electric and compact vehicles, where saving space and power is critical. With fleet operators and the automotive industry ramping up their push for autonomous driving capabilities, radar sensors' importance grows across vehicle segments, elevating RoC to a strategic priority.

Advancements in microwave millimeter-wave (mmWave) CMOS and RF-CMOS technologies have accelerated the development of radar-on-chip systems. These improvements allow all radar components operating in the 76 to 81 GHz frequency range to be integrated into a single die, reducing size, power consumption, and costs. Economical mass production of RoC chips with high yields further supports adoption in automotive manufacturing. Moreover, modern RoC chips incorporate artificial intelligence (AI) and machine vision processors for enhanced object detection and classification, resulting in software-defined, updatable radar systems that improve adaptability and extend product life.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 15.6% |

Single-chip system-on-chip (SoC) solutions led the market, generating USD 900 million in 2024. These single-chip SoCs combine radar functions-including RF transceivers and signal processing-with logic circuitry on one chip, enhancing power efficiency, reducing manufacturing costs, and simplifying vehicle integration. This compact design becomes increasingly important as OEMs focus on fleet electrification and digitalization. For advanced computing needs or redundancy in customized advanced driver-assistance systems (ADAS), multi-chip modules remain preferred. Meanwhile, integrated radar arrays are gaining traction in high-definition radar applications.

The passenger vehicle segment dominated the market with USD 1.1 billion in 2024. SUVs are the fastest-growing subcategory within passenger vehicles, driven by consumer preference for larger models that incorporate ADAS features. Radar-on-chip solutions balance advanced and mid-level safety functionalities cost-effectively, especially for sedans and entry-level hatchbacks where risk mitigation is critical.

Asia Pacific Automotive Radar-on-Chip Technology Market captured a 43% share in 2024. Growth here is fueled by strong vehicle production, increasing penetration of ADAS, and robust government initiatives. High manufacturing volumes give regional OEMs advantages in adopting cost-efficient radar technologies. The push toward Level 3+ autonomous driving in countries like China has accelerated radar adoption in electric and intelligent vehicles. National programs support domestic radar-on-chip development through partnerships among industry leaders and tech firms. Japan and South Korea focus on reducing chip size and power consumption, and integrating multi-chip systems into single-chip solutions. Emerging urban air mobility radar SoCs and multi-modal ADAS sensors are being developed and integrated by regional automotive manufacturers.

Key players in the Global Automotive Radar-on-Chip Technology Market include Valeo, Texas Instruments, Robert Bosch, Infineon Technologies, Continental, Denso Corporation, NXP Semiconductors, ZF Friedrichshafen, and Arbe Robotics. To reinforce their market presence, companies in the automotive radar-on-chip space are prioritizing research and development focused on enhancing integration, power efficiency, and computational capabilities within smaller form factors. Collaboration with automotive OEMs and technology firms enables tailored solutions for evolving autonomous driving requirements. Strategic investments in AI-enabled radar systems and software-updatable platforms boost product adaptability and lifespan. Expanding manufacturing capabilities to improve chip yields and reduce costs remains a focus, as does compliance with global automotive standards. Firms are also leveraging partnerships and joint ventures to accelerate innovation and scale production while targeting emerging markets through localized production and distribution networks.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Region

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Frequency band

- 2.2.3 Range

- 2.2.4 Technology

- 2.2.5 Vehicle

- 2.2.6 Sales Channel

- 2.2.7 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Safety regulations and NCAP mandates

- 3.2.1.2 Rising ADAS and autonomous demand

- 3.2.1.3 Integration with AI and sensor fusion

- 3.2.1.4 Government-funded mobility programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex calibration and validation

- 3.2.2.2 High R&D and chip development costs

- 3.2.3 Market opportunities

- 3.2.3.1 Level 3+autonomy adoption

- 3.2.3.2 Emerging markets penetration

- 3.2.3.3 Next-gen radar with 4D imaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Consumer behavior analysis

- 3.11.1 OEM vs aftermarket preferences

- 3.11.2 Cost–performance decision factors

- 3.12 Analysis of aftermarket trends

- 3.12.1 Radar system maintenance & warranties

- 3.12.2 Chip replacement cycles

- 3.12.3 Cost vs benefit for Tier 1 vs OEM models

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Frequency Band, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 24 GHz

- 5.3 77 GHz

- 5.4 79 GHz

Chapter 6 Market Estimates & Forecast, By Range, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Short-Range Radar (SRR)

- 6.3 Medium-Range Radar (MRR)

- 6.4 Long-Range Radar (LRR)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Single-chip SoC

- 7.3 Multi-chip module

- 7.4 Integrated radar arrays

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Passenger vehicle

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicle

- 8.3.1 Light Commercial Vehicle (LCV)

- 8.3.2 Medium Commercial Vehicle (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 Adaptive Cruise Control (ACC)

- 10.3 Blind Spot Detection (BSD)

- 10.4 Forward Collision Warning (FCW)

- 10.5 Automatic Emergency Braking (AEB)

- 10.6 Advanced parking assist

- 10.7 Corner radar for autonomous vehicles

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Analog Devices

- 12.2 Aptiv

- 12.3 Arbe Robotics

- 12.4 Artsys360

- 12.5 Autoliv

- 12.6 Calterah Semiconductor Technology

- 12.7 Continental

- 12.8 Delphi Technologies

- 12.9 Denso

- 12.10 HELLA GmbH

- 12.11 Infineon Technologies

- 12.12 NXP Semiconductors

- 12.13 Renesas Electronics

- 12.14 Robert Bosch

- 12.15 Steradian Semiconductors

- 12.16 Texas Instruments

- 12.17 Uhnder

- 12.18 Valeo

- 12.19 Veoneer

- 12.20 ZF Friedrichshafen